Disclaimer: This article is for educational and informational purposes only and does not constitute personalized financial or investment advice. Past performance of any investment does not guarantee future results.

Starting small doesn’t mean thinking small. If you’re wondering whether investing $50 a month in VOO is actually worth it, the short answer is: yes, and more than most people expect. By consistently putting just $50 into the Vanguard S&P 500 ETF every single month over 20 years, you could turn a modest habit into a meaningful wealth-building machine — powered almost entirely by the magic of compound growth.

In this guide, we’ll break down exactly what VOO is, how the math works over two decades, what taxes you need to plan for, and whether this strategy fits your life. Let’s get into it.

What Is VOO and Why Do Beginners Love It?

VOO is the ticker symbol for the Vanguard S&P 500 ETF, a fund that tracks the performance of the S&P 500 index — 500 of the largest publicly traded companies in the United States. When you buy one share of VOO, you instantly own a tiny slice of companies like Apple, Microsoft, Amazon, Nvidia, and nearly 500 others.

What makes VOO especially appealing for beginners and long-term investors is its rock-bottom cost. VOO carries an expense ratio of just 0.03% per year — meaning you pay only 30 cents annually for every $1,000 invested. That’s one of the lowest fees of any ETF on the market. Additionally, VOO currently pays a dividend yield of approximately 1.09%, with about $7.13 per share distributed annually in quarterly payments.

VOO’s Historical Performance: The Numbers Behind the Strategy

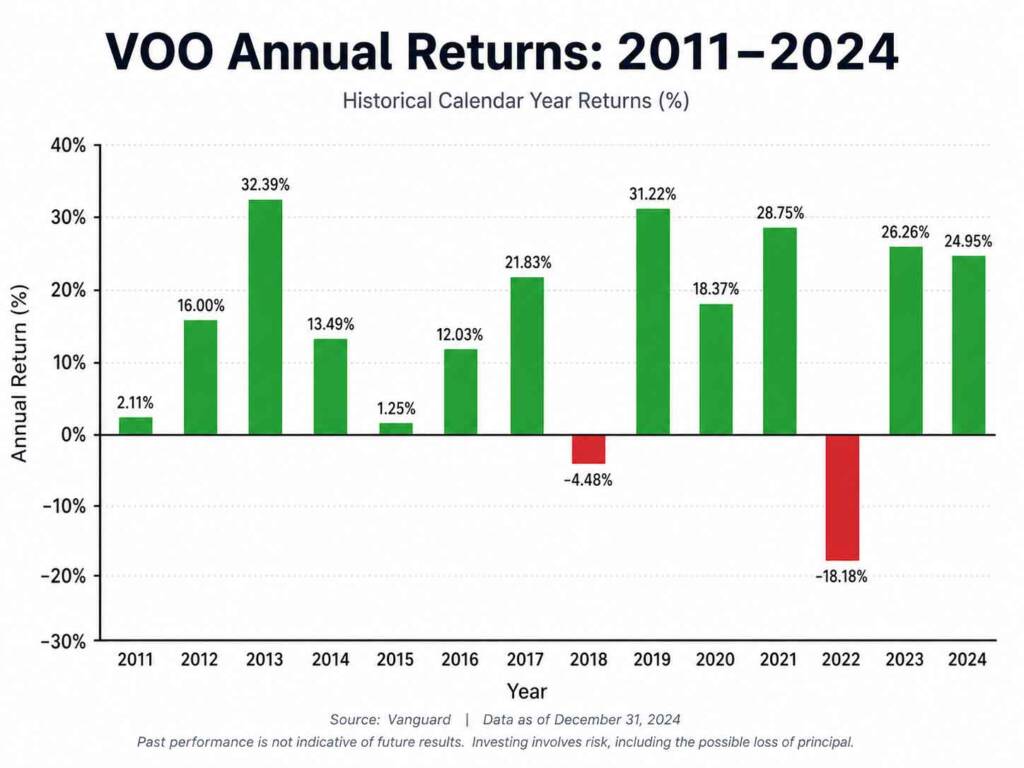

Before projecting the future, it helps to understand what VOO has done in the past. According to historical data, the S&P 500 has delivered an average annual return of approximately 10% since its inception, and the 30-year average from 1996 through 2025 came in at 10.4%.

VOO’s own track record since launching in 2010 is even more impressive. Including dividends reinvested, VOO has delivered a total return of approximately 762% from 2010 through April 2026, translating to roughly 13–14% annualized. Of course, not every year looks the same — VOO returned 26.32% in 2023, lost 18.17% in 2022, and gained 24.98% in 2024. That volatility is normal, and it’s exactly why a long time horizon matters.

Over the last 30 years, the S&P 500 achieved a compound annual return of 9.91%, even after periods like the 2000 dot-com crash and the 2008 financial crisis, with a maximum drawdown of -50.80% before fully recovering. This context should remind every investor that patience is part of the strategy.

The 20-Year Projection: What $50 a Month Can Realistically Become

The Power of Compound Growth

Compound growth means your earnings generate their own earnings. When you reinvest dividends — which VOO allows automatically through most brokerage platforms — your money snowballs over time. Even at just $50 per month, that snowball effect is powerful enough to significantly outpace what you put in.

Three Realistic Scenarios

Over 20 years, you will invest a total of $12,000 ($50 × 240 months). Here’s how that could grow depending on your average annual return:

| Scenario | Assumed Annual Return | Total Invested | Projected Final Value | Total Gain |

|---|---|---|---|---|

| Conservative | 7% | $12,000 | $26,046 | $14,046 |

| Moderate | 10% | $12,000 | $37,968 | $25,968 |

| Optimistic | 12% | $12,000 | $49,463 | $37,463 |

The moderate 10% scenario — which aligns closely with the S&P 500’s long-term historical average — shows your $12,000 growing to nearly $38,000, more than tripling your original investment. The conservative 7% case (accounting for inflation or a slower market decade) still more than doubles your money.

These figures assume monthly contributions, dividends reinvested, and no withdrawals. They do not account for taxes on dividends in a taxable brokerage account.

Why the Strategy Works: Dollar-Cost Averaging

The method behind this plan is called dollar-cost averaging (DCA) — investing a fixed dollar amount at regular intervals regardless of market conditions. When prices fall, your $50 buys more shares. When prices rise, you still keep building. According to investment research, this disciplined approach helps remove emotion from investing and reduces the risk of bad market timing. It makes VOO an accessible entry point for anyone with a modest budget and a long runway.

VOO vs. Comparable ETFs: Choosing the Right Core Holding

If you’re comparing VOO to similar options before committing, here’s a quick look at how some popular broad-market ETFs stack up:

| ETF | Tracks | Expense Ratio | Dividend Yield | AUM |

|---|---|---|---|---|

| VOO | S&P 500 | 0.03% | ~1.09% | ~$862B |

| IVV (iShares) | S&P 500 | 0.03% | ~1.3% | ~$600B |

| SPY (SPDR) | S&P 500 | 0.0945% | ~1.2% | ~$530B |

| VTI (Vanguard) | Total US Market | 0.03% | ~1.3% | ~$460B |

VOO and IVV are essentially identical in cost and coverage. SPY costs slightly more but offers higher liquidity, which matters more for traders than for long-term investors like you. VTI adds mid- and small-cap exposure, giving broader diversification. For most beginners running a $50/month DCA strategy, VOO is the most popular and trusted starting point.

Tax Considerations for VOO Investors

The way you’re taxed on VOO depends heavily on which account type you use.

In a taxable brokerage account, VOO’s dividends are generally classified as qualified dividends, taxed at preferential rates. For the 2025 tax year, qualified dividends are taxed at 0% for single filers earning up to $48,350, and at 15% for most middle-income earners above that threshold. You can verify the current rules directly on the IRS dividend tax topic page.

In a Roth IRA, the story gets much better. All growth and qualified withdrawals are completely tax-free. The 2025 Roth IRA contribution limit is $7,000 per year (or $8,000 if you’re 50 or older), which easily covers $50 per month. If your income qualifies — under $150,000 for single filers in 2025 — a Roth IRA is almost always the smarter home for a VOO DCA strategy. Your future self will thank you for it.

Risks to Know Before You Start

Investing $50 a month in VOO is one of the most sensible strategies available to everyday investors — but it’s not without risk. Here are the key ones to understand:

- Market volatility: VOO dropped 18.17% in 2022. If you need the money in 2–5 years, equities may not be right for you.

- Sequence of returns risk: A major crash early in your investing timeline can have an outsized negative effect if you plan to withdraw soon after.

- Inflation risk: At a 7% nominal return, real purchasing power growth (after ~3% inflation) may be closer to 4%. The moderate scenario adjusted for inflation still shows meaningful long-term growth.

- No guarantees: The S&P 500’s 10% average is an average — some decades deliver more, some deliver less. The 20-year return from 2004–2024 was 8.4% annualized.

- Concentration risk: VOO holds US large-cap stocks only. Some investors add international or bond ETFs for balance.

Is Investing $50 a Month in VOO Right for You?

This strategy works best if you check most of these boxes:

- You have a time horizon of 10 years or more

- You have an emergency fund already in place (3–6 months of expenses)

- You want a simple, low-maintenance investment approach

- You’re comfortable leaving money invested through downturns

- You’re investing in a Roth IRA or tax-advantaged account if possible

If you’re 25 and starting today, that $50/month habit — if maintained and scaled up as your income grows — could become the cornerstone of your retirement portfolio. Even if you’re 40, a 20-year horizon to age 60 still gives compounding enough time to work significantly in your favor.

Frequently Asked Questions

Can I really build wealth by investing just $50 a month in VOO?

Yes. As shown in the projections above, $50/month over 20 years at a 10% average annual return could grow to approximately $37,968 — more than triple your $12,000 invested. The key is consistency and time, not the size of your initial investment.

What is the best account to hold VOO in for long-term investing?

A Roth IRA is generally the best choice for long-term VOO investing because all growth and qualified withdrawals are tax-free. If you’ve maxed out your Roth IRA, a traditional brokerage account still works well, especially if your income keeps qualified dividends in the 0% tax bracket.

What happens if the stock market crashes right after I start investing?

A crash early in your timeline is actually an opportunity when you’re using dollar-cost averaging. Your $50 buys more shares at lower prices, reducing your average cost per share. Historically, the S&P 500 has always recovered from every major downturn.

Does VOO pay dividends, and how often?

Yes. VOO currently pays a dividend yield of approximately 1.09%, distributed quarterly. The last ex-dividend date was March 27, 2026. In a Roth IRA, reinvesting these dividends compounds your returns tax-free.

How does investing $50 a month in VOO compare to leaving money in a savings account?

A high-yield savings account today might offer 4–5% APY. While that’s attractive and risk-free, it won’t keep pace with stock market returns over 20 years. At 5% for 20 years, your $12,000 grows to roughly $20,551 — compared to $37,968 at 10% with VOO. The trade-off is accepting short-term volatility for significantly higher long-term returns.

Conclusion: Start Small, Think Big

Investing $50 a month in VOO is not a get-rich-quick scheme — it’s one of the most time-tested, evidence-backed wealth-building habits available to everyday Americans. You’re buying a piece of the largest, most innovative companies in the world, at a 0.03% fee, using a disciplined strategy that removes emotion from the equation.

The best time to start was yesterday. The second-best time is today. Open a Roth IRA, set up a $50 automatic monthly investment into VOO, and let compounding do the heavy lifting for the next two decades. Your future self will look back at this decision as one of the best financial moves you ever made.

Ready to get started? Open a brokerage or Roth IRA account with a provider like Vanguard, Fidelity, or Charles Schwab — all of which allow fractional or full VOO purchases with no trading commissions. Then automate your $50 and forget about it (mostly).