Have you ever stared at your brokerage account wondering whether to load up on high-flying growth stocks or just sit back and collect dividend checks every quarter? You’re not alone. The debate around growth vs dividend investing is one of the most common — and most important — questions every retail investor eventually has to answer.

Here’s the honest truth: there’s no universally “better” strategy. However, one approach will almost certainly fit your current situation better than the other. In this guide, we’ll break down how each strategy works, compare them side by side, and help you figure out which one (or what combination) actually makes sense for your financial goals.

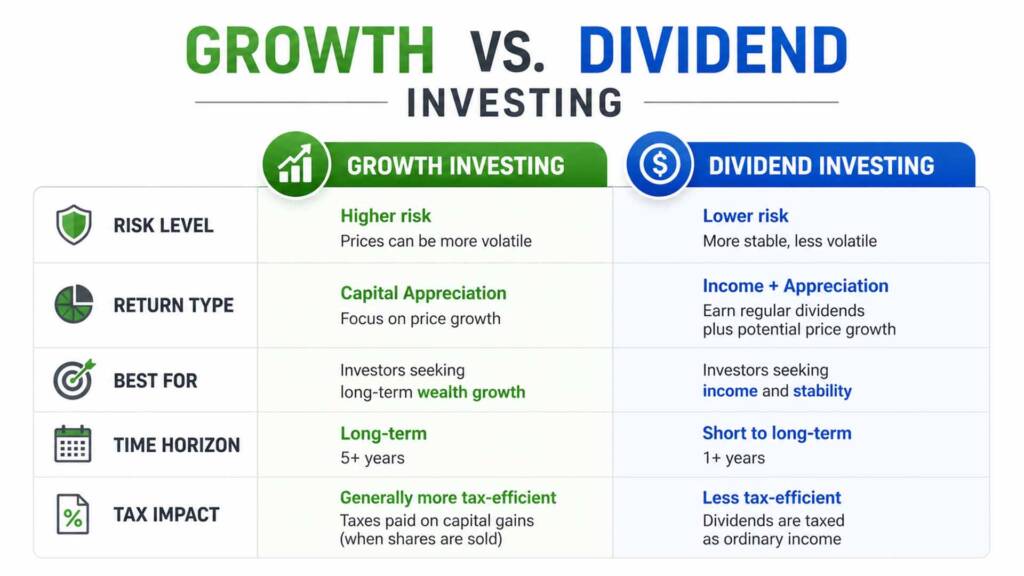

What Is Growth Investing?

Growth investing is all about buying companies — or funds — that are expected to increase in value significantly over time. Instead of paying dividends, these companies reinvest every dollar of profit back into the business to fuel expansion. Think of it like planting a tree: you don’t pick fruit today, but you expect a much bigger harvest down the road.

How Growth Stocks Generate Returns

The primary engine behind growth investing is capital appreciation — meaning the stock price goes up. When you invest in a company like Amazon or Nvidia during its high-growth phase, the returns come when you eventually sell your shares at a higher price than you paid.

A few things drive that price appreciation:

- Revenue and earnings growth — companies consistently beating analyst expectations

- Expanding market share — capturing customers from slower competitors

- Innovation and disruption — new products, platforms, or business models

- Investor sentiment — as growth prospects brighten, more buyers push prices up

The tradeoff? Growth stocks tend to be more volatile. During market downturns, they can drop sharply. For example, QQQ — a tech-heavy growth ETF — fell nearly 33% during 2022’s selloff before rebounding strongly. According to Investopedia, growth investors need a high risk tolerance and a long investment horizon to weather those swings.

Popular Growth ETFs to Know

If you’re not interested in picking individual stocks, ETFs make growth investing incredibly accessible. Two of the most popular growth-oriented ETFs are:

- VOO (Vanguard S&P 500 ETF) — Tracks the S&P 500, giving you exposure to 500 of America’s largest companies. It returned ~25% in 2024 and ~18% in 2025. It’s low-cost (0.03% expense ratio) and broadly diversified.

- QQQ (Invesco QQQ Trust) — Tracks the Nasdaq-100, heavily weighted toward technology giants like Apple, Microsoft, and Nvidia. More concentrated and more volatile than VOO, but delivered ~25% annually from 2022–2026.

To understand how ETFs work under the hood before diving deeper, check out our beginner’s guide to ETF investing.

What Is Dividend Investing?

Dividend investing focuses on owning companies or funds that regularly distribute a portion of their profits directly to shareholders. Instead of waiting to sell for a gain, you get paid — typically quarterly — just for holding the investment. For many investors, especially those approaching retirement, this steady income stream is extremely appealing.

How Dividend Stocks Create Passive Income

Here’s a simple way to think about it: if you own 100 shares of a stock paying a $2/year dividend, you receive $200 annually regardless of whether the stock price moves up or down. As noted by Fidelity’s investing resources, dividend-paying investments are a cornerstone strategy for building reliable passive income.

Additionally, dividend investors benefit from:

- Reinvestment compounding — reinvesting dividends to buy more shares accelerates growth over time

- Downside cushion — dividend stocks tend to fall less during market corrections

- Predictable cash flow — especially valuable in retirement or for supplementing income

In contrast to growth stocks, dividend stocks are typically more mature businesses in sectors like utilities, consumer staples, or financials — industries less prone to dramatic swings.

Popular Dividend ETFs to Know

- SCHD (Schwab U.S. Dividend Equity ETF) — One of the most beloved dividend ETFs, focused on high-quality U.S. companies with strong dividend histories. It delivered a total return of about 4.3%/year from 2022–2026, prioritizing income stability over rapid growth.

- JEPQ (JPMorgan Nasdaq Equity Premium Income ETF) — A covered-call strategy ETF that generates high monthly income (often 8–11% annual yield) while still tracking Nasdaq-linked companies. It returned ~11.3%/year from 2022–2026 and is increasingly popular for hybrid income strategies.

Growth vs. Dividend Investing: Key Differences

Understanding the contrast between these two strategies is essential before putting real money to work. Therefore, here’s a direct side-by-side comparison:

One important tax nuance: with growth investing, you control when you owe taxes — you only pay capital gains tax when you sell. With dividend investing, the IRS considers your distributions as income each year, even if you reinvest them immediately. Over decades, this difference can meaningfully affect your compounding power.

Which Strategy Fits Your Financial Goals?

The right choice depends almost entirely on where you are in life, what you need your money to do, and how much volatility you can stomach without panic-selling.

Choose Growth Investing If…

- You’re in your 20s, 30s, or early 40s with at least 10 years before you need the money

- You don’t need current income from your investments

- You’re comfortable watching your portfolio drop 30–40% in a bad year without selling

- Your primary goal is maximum long-term wealth accumulation

- You’re investing in a tax-advantaged account like a Roth IRA or 401(k), minimizing the tax drag

Choose Dividend Investing If…

- You want regular cash flow from your portfolio — monthly or quarterly

- You’re in or near retirement and prioritizing capital preservation plus income

- You prefer lower volatility and more defensive holdings

- You want a tangible “paycheck” to reinvest or cover living expenses

- You’re okay with potentially lower total returns in exchange for that predictability

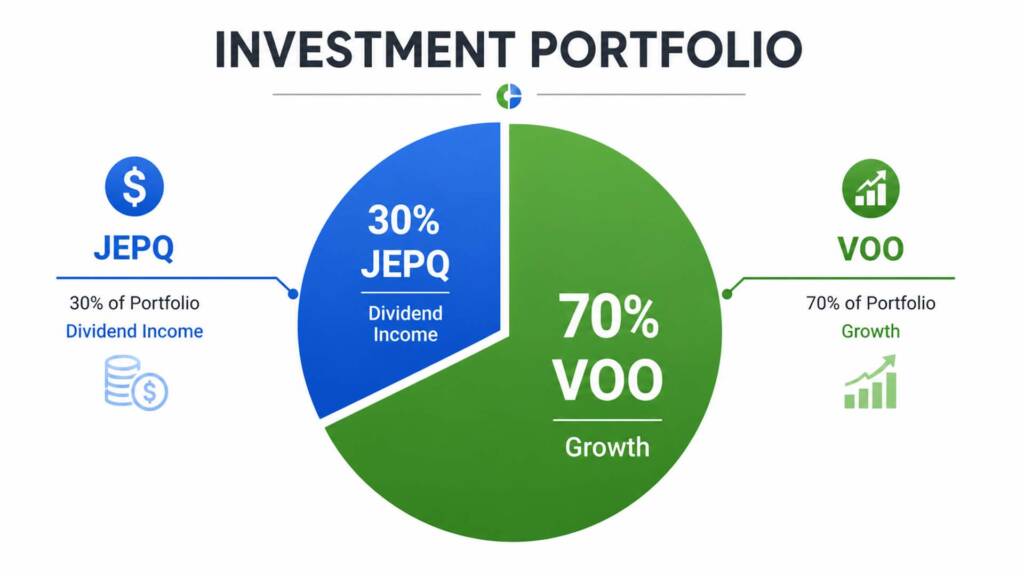

Can You Combine Both? (The Hybrid Approach)

Absolutely — and honestly, this is what most experienced investors end up doing. The hybrid approach lets you capture the best of both worlds: long-term growth and passive income. For example, a straightforward hybrid portfolio might look like this:

- 70% VOO — for broad market growth exposure

- 30% JEPQ — for monthly income via covered-call premiums

This blend means your portfolio keeps compounding through the S&P 500 while JEPQ hands you a regular income stream. As your life circumstances change — say, you get closer to retirement — you can gradually shift the allocation from growth-heavy to income-heavy. That’s the flexibility hybrid investing offers.

A Real Portfolio Example: Blending Growth and Dividends

Let’s make this concrete. Imagine you invest $10,000 with a 70/30 split between VOO and JEPQ:

- $7,000 in VOO — targeting capital growth aligned with the S&P 500’s historical ~10% annual return

- $3,000 in JEPQ — targeting roughly 9–11% annual yield through monthly distributions

In 2024, both ETFs performed remarkably well — VOO returned ~25% and JEPQ returned ~24.85%. In 2025, VOO returned ~17.8% and JEPQ ~15.2%. This kind of real-world data shows that hybrid portfolios don’t have to sacrifice much growth to gain the benefit of income.

Want a deeper dive into how this exact portfolio is structured and rebalanced? Read our VOO and JEPQ portfolio breakdown for a full walkthrough of the allocation logic.

How to Start Investing With as Little as $50/Month

One of the biggest myths in investing is that you need thousands of dollars to get started. In reality, both growth and dividend strategies are fully accessible with small, consistent monthly contributions — especially with fractional shares now widely available.

Dollar-cost averaging (DCA) is the practice of investing a fixed amount on a regular schedule, regardless of where the market is. It removes the guesswork of timing the market and builds discipline into your financial habits. Additionally, it means you automatically buy more shares when prices are low and fewer when they’re high — a naturally smart strategy.

Consider this: if you invested just $50/month into VOO starting in 2022, your portfolio today would reflect the power of consistent contributions compounding through both market dips and rallies. Curious what those exact numbers look like? Check out how investing $50/month in VOO works in practice — the results might surprise you.

As NerdWallet explains, DCA is one of the most beginner-friendly strategies available, and it works for both growth and dividend ETFs alike.

Frequently Asked Questions

Q: Is dividend investing better than growth investing for beginners?

Neither approach is universally “better” for beginners — it really comes down to your goals. However, many beginners find dividend investing psychologically easier because seeing regular deposits hit your account feels rewarding and keeps motivation high. On the other hand, growth investing with ETFs like VOO is extremely simple to execute: buy shares regularly and let time do the heavy lifting. If you’re just starting out and don’t need income yet, a broad growth ETF like VOO is typically the cleaner starting point.

Q: Can I lose money with dividend stocks or ETFs?

Yes — dividend stocks are still stocks, and they can and do lose value. In fact, if a company cuts its dividend during hard times, the stock price often drops too, hitting you twice. That said, diversified dividend ETFs like SCHD spread this risk across dozens of high-quality companies, significantly reducing exposure to any single stock’s failure. The key is to treat your dividend ETF as a long-term hold, not a short-term trade.

Q: How are dividends taxed compared to capital gains?

Dividends are generally taxed in the year you receive them. Qualified dividends — from most U.S. stocks and ETFs held for the required period — are taxed at long-term capital gains rates: 0%, 15%, or 20% depending on your income. Non-qualified dividends are taxed as ordinary income, which can be as high as 37%. In contrast, growth investing lets you defer taxes until you sell your shares. Therefore, if you’re investing in a taxable account, growth strategies often have a tax efficiency advantage over high-yield dividend strategies.

Conclusion

Both growth and dividend investing are legitimate, proven paths to building wealth — they just serve different purposes at different life stages. Growth investing maximizes long-term compounding, while dividend investing prioritizes steady, recurring income. For many investors, the smartest move is a thoughtful blend of both. Start by clarifying what you actually need your money to do right now, then let that guide your allocation.

Ready to take the next step? Explore our VOO and JEPQ portfolio breakdown to see exactly how a real hybrid portfolio is built and maintained — from initial allocation to rebalancing strategy.