Most beginner investors don’t lose money because of bad luck. They lose it because of beginner investor mistakes that are entirely avoidable — mistakes that even smart, educated people fall into when they first start investing.

The good news? Every one of these mistakes has a straightforward fix. Let’s break them down so you can stop leaving money on the table.

Why Beginner Investor Mistakes Are So Costly

According to Morningstar’s 2025 Mind the Gap report, the average dollar invested in U.S. mutual funds and ETFs earned 1.2% less per year than what those funds actually returned over the 10-year period ending December 2024. That gap represents roughly 15% of total potential returns lost — not because of bad funds, but because of bad investor behavior.

DALBAR’s research tells an even starker story: over the past decade, the average equity fund investor earned around 9.8% annually, compared to the S&P 500’s annualized return of roughly 13%. The difference isn’t the market. It’s the investor.

Think of investing like planting a fruit tree. You don’t dig it up every month to check if the roots are growing. You plant it, water it consistently, and wait. The investors who make the most money are often the ones who simply get out of their own way.

Mistake #1: Trying to Time the Market

Timing the market means waiting for the “perfect” moment to buy or sell. It sounds logical. In practice, it’s one of the most destructive beginner investor mistakes you can make.

Morningstar found that funds with the most volatile cash flows — driven by investors jumping in and out — had an annual return gap of 1.8%, more than double the 0.8% gap seen in funds with stable inflows. Every time you pull out and re-enter, you risk missing the best days of the market.

How to avoid it:

- Invest on a regular schedule, regardless of market conditions (dollar-cost averaging)

- Automate contributions monthly so emotion doesn’t interfere

- Focus on time in the market, not timing the market

If you’re looking for a simple way to start, see our guide on investing $50 a month in VOO — a real-world example of consistent investing done right.

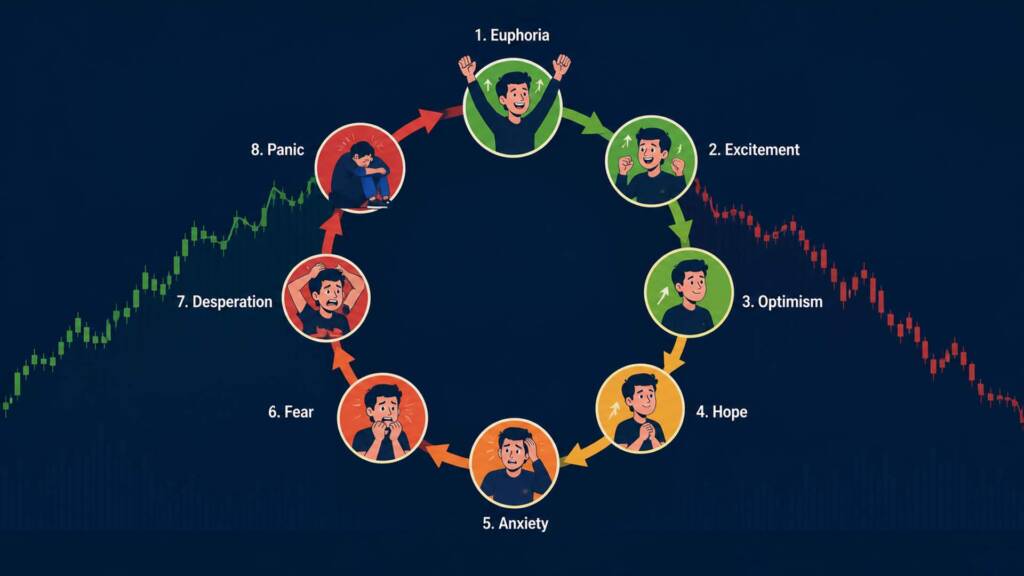

Mistake #2: Letting Emotions Drive Decisions

Fear and greed are the two most expensive emotions in investing. When markets drop, fear pushes beginners to sell. When markets surge, greed pushes them to pile in — often near the top. This pattern is well-documented and financially devastating.

In 2025, the S&P 500 — tracked by ETFs like VOO — delivered a 17.82% return. However, most retail investors who panic-sold during mid-year volatility missed a significant portion of those gains. The investors who stayed the course collected the full return.

How to avoid it:

- Write down your investment strategy before you start — and follow it

- Set price alerts instead of checking your portfolio daily

- Remember: a temporary dip is not a permanent loss unless you sell

However, this is easier said than done. Financial analysts consistently note that stress-driven micro-decisions are the single biggest threat to long-term wealth.

Mistake #3: Failing to Diversify

Putting all your money into one stock, one sector, or one country is a recipe for outsized risk. Many beginners in 2025 over-concentrated in U.S. tech stocks — and while it worked that year, Morningstar warned that ignoring non-U.S. stocks was a mistake in 2025 and remains a risk in 2026.

Diversification doesn’t mean owning 50 random stocks. It means spreading risk intelligently across asset classes, sectors, and geographies.

How to avoid it:

- Use broad-market ETFs that provide built-in diversification

- Don’t let any single position dominate your portfolio

- Consider pairing a growth ETF with an income-focused ETF

For a practical diversification model, check out our breakdown of the VOO and JEPQ portfolio — a two-fund strategy that balances growth and income. New to ETFs entirely? Start with what is ETF investing to build your foundation.

Mistake #4: Chasing Hot Tips and FOMO

Social media and financial news cycles create a constant stream of “can’t-miss” opportunities. AI stocks, meme coins, the next big IPO — beginners feel the pressure to act before they miss out. This is FOMO investing, and it rarely ends well.

The core problem is that by the time a stock is trending on social media, the early gains are already baked in. You’re buying the hype, not the value. Following friends’ or acquaintances’ tips without doing your own research is one of the most frequently cited mistakes among novice investors.

How to avoid it:

- Establish a personal investing strategy first — then evaluate any “hot tip” against it

- Ask: would I have bought this without the tip? If no, skip it

- Stick to fundamentally sound, low-cost index funds as your core holdings

Understanding the difference between growth and income strategies can also reduce FOMO-driven decisions. See our comparison of growth vs. dividend investing to find what actually fits your goals.

Mistake #5: Ignoring Fees and Expense Ratios

This one flies under the radar — but it compounds into a massive drag on returns over time. Many beginners simply don’t check what they’re paying in fund fees, advisory charges, or trading commissions.

Consider: a fund charging a 1% expense ratio versus one charging 0.03% (like VOO) may seem like a minor difference. Over 30 years on a $10,000 investment growing at 8% annually, that 0.97% difference translates into thousands of dollars in lost compounding.

How to avoid it:

- Always check the expense ratio before investing in any fund

- Prefer low-cost index ETFs over actively managed funds with high fees

- Use platforms with no transaction fees for ETF purchases

According to Investopedia, even small differences in expense ratios can significantly erode long-term wealth due to the power of compounding.

Real-World Scenario: What These Mistakes Look Like Together

Meet Alex, a 28-year-old who starts investing $200/month in 2024. In January 2025, he reads about a hot AI stock on Reddit, sells his ETF holdings to buy in, then panics and sells when it drops 20%. He sits in cash for three months, then jumps back in near the market high. Meanwhile, his fund — which would have returned 17.82% for the year — earned him almost nothing.

Compare this to Jamie, who sets up an automatic $200/month into a simple S&P 500 ETF, never touches it during volatility, and ends the year with close to the market’s full return. Same starting capital. Completely different outcome — not because of luck, but because Jamie avoided every mistake on this list.

Pros and Cons of a Disciplined Approach

| Approach | Pros | Cons |

|---|---|---|

| Consistent DCA into index ETFs | Low cost, emotion-free, market-matching returns | Won’t beat the market |

| Active stock picking | Potential for outperformance | High risk, time-intensive, fee-heavy |

| Waiting for the “right time” | Feels safer psychologically | Historically leads to underperformance |

Frequently Asked Questions

Q: What is the #1 beginner investor mistake?

A: Emotional decision-making — specifically, selling during downturns and buying during peaks — is the leading cause of underperformance, per Morningstar’s 2025 Mind the Gap study.

Q: How much does poor timing actually cost investors?

A: According to DALBAR, the average equity investor earned roughly 9.8% annually over the last decade versus the S&P 500’s ~13% — a multi-percentage-point annual shortfall driven primarily by behavioral mistakes.

Q: Is it too late to start investing if you’re a beginner in 2026?

A: No. Time in the market still matters more than timing. Starting with even $50/month in a diversified, low-cost ETF puts you ahead of the majority of people who never start at all.

Q: How do I know which ETF to start with?

A: Broad-market, low-cost ETFs like VOO are a popular starting point for beginners. Check our ETF investing guide for a step-by-step breakdown.

Q: Should beginners use dividend ETFs or growth ETFs?

A: It depends on your goals. Growth ETFs are better for long-term wealth accumulation; dividend ETFs provide income. Our guide on growth vs. dividend investing can help you decide.

Start Simple, Stay Consistent

The biggest edge a beginner investor has is time — but only if you use it wisely. Avoid these five beginner investor mistakes, stick to a consistent strategy, keep your costs low, and let compounding do the heavy lifting.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. All investing involves risk, including the possible loss of principal. Past performance is not indicative of future results. Please consult a qualified financial advisor before making investment decisions.