You’ve been investing for a while — maybe you hold a few ETFs, maybe a stock or two. But something feels off. Your portfolio lacks structure. One month it surges; the next it drops harder than the market. You don’t have a real plan — you have a collection. That uncertainty quietly erodes both your returns and your confidence. Here’s the truth: most successful long-term investors don’t just pick great assets. They build a core and satellite portfolio — a structured framework that combines the stability of broad-market index funds with the growth potential of targeted, high-upside positions. By the end of this article, you’ll have a clear, actionable blueprint to build your own.

Key Takeaways:

- A core and satellite portfolio anchors 60–80% of your capital in a stable, low-cost broad-market ETF (like VOO) and deploys 20–40% in targeted “satellite” positions for enhanced returns.

- As of May 2026, VOO is priced at $679.44 with a YTD return of +8.68% and a 1-year return of +26.68% — demonstrating the power of a consistent core holding through volatile markets.

- Satellite ETFs like SMH and QQQM have delivered +54.48% and +15.57% YTD in 2026 respectively — showing how targeted satellite exposure can meaningfully boost total portfolio returns above the market average.

What Is a Core and Satellite Portfolio?

The core and satellite portfolio is one of the most respected investment frameworks in modern wealth management. Its logic is elegant in its simplicity: protect the bulk of your wealth in a proven, diversified core, then use a smaller satellite allocation to pursue targeted, higher-upside opportunities.

The concept was formalized by institutional portfolio managers who recognized a fundamental truth: consistently beating the market is nearly impossible, but participating in specific high-growth trends is not. The strategy borrows the best of two worlds — passive investing’s compounding reliability and active investing’s growth potential — while minimizing the worst of each.

According to UBS Asset Management, a typical core-satellite framework allocates roughly 80% to core holdings and 20% to satellite positions, though this ratio can be adjusted based on your risk tolerance, time horizon, and investment goals. For most retail investors building long-term wealth, a 60/40 or 70/30 split is a practical and powerful starting point.

Why the Core Matters: Building on Bedrock

The core is the most critical element of your entire portfolio. It is non-negotiable. Get this wrong, and no satellite position will save you. Get this right, and even a poor satellite selection won’t derail your wealth-building trajectory.

VOO: The Gold Standard Core Holding

For US market investors in 2026, VOO (Vanguard S&P 500 ETF) is the benchmark core holding — and the data backs it up at every time horizon.

Here’s VOO’s current performance snapshot as of May 15, 2026:

- Current Price: $679.44

- YTD Return (2026): +8.68%

- 1-Year Total Return: +26.68%

- 52-Week Range: $529.11 – $689.10

- Expense Ratio: 0.03%

- Total Net Assets: $927.8 billion

- Dividend Yield: ~1.1%

Critically, VOO’s low 0.03% expense ratio means you keep nearly every dollar of market return. Compare that to the average actively managed fund charging 0.5–1.0%, and the difference compounds to tens of thousands of dollars over a 30-year holding period.

The S&P 500 has delivered a 1-year return of +25.21% as tracked by S&P Dow Jones Indices, and VOO mirrors this precisely. Even during 2026’s early volatility — when the index briefly dipped into negative territory — VOO recovered strongly, closing May 2026 with a positive YTD return of +8.68%. That resilience is exactly what a core holding is designed to provide.

For a deep dive into why VOO works so well as a portfolio anchor, read our dedicated article: VOO ETF Core Portfolio — Why It’s the Foundation Every Investor Needs.

Other Strong Core ETF Options

While VOO is the preferred core for most investors, alternative core choices exist depending on your goals:

- SCHD — for income-focused investors who want dividends as part of their core

- VT (Vanguard Total World Stock ETF) — for globally diversified investors who want international exposure in their core

- QQQM — for investors with higher risk tolerance who want tech-heavy growth as their core

However, for most beginner-to-intermediate investors, VOO remains the optimal core choice: diversified across 500 of America’s largest companies, historically proven over decades, and nearly free to own.

What Are Satellite Positions?

Satellites are the growth accelerators of your portfolio. They typically represent 20–40% of your total allocation and are designed to outperform the core over specific time windows by targeting high-conviction themes, sectors, or income strategies.

Satellites are NOT lottery tickets. They are deliberate, researched, tactical positions that complement — not compete with — your core. The key discipline: never let your satellite positions grow so large that they threaten the stability your core provides.

Types of Satellite Positions

1. Growth Satellite — QQQM (Invesco Nasdaq-100 ETF)

QQQM gives you concentrated exposure to the 100 largest non-financial Nasdaq companies — think Apple, Microsoft, Nvidia, Meta, and Amazon. As of May 15, 2026, QQQM has delivered a YTD return of +15.57% and an extraordinary 1-year return of +37.24%, nearly 11 percentage points above VOO’s 1-year return. For investors who believe US technology will continue to drive long-term economic growth, QQQM is the cleanest satellite vehicle available. Its expense ratio of just 0.15% keeps cost impact minimal.

2. Sector Satellite — SMH (VanEck Semiconductor ETF)

SMH focuses exclusively on the semiconductor industry — the foundational hardware layer of the AI revolution. The results in recent years have been staggering: +54.48% YTD in 2026 and a jaw-dropping +125.82% 1-year return as of May 15, 2026. Companies like Nvidia, TSMC, and Broadcom dominate its holdings. This is a high-conviction, high-volatility satellite — appropriate for aggressive growth investors comfortable with significant drawdowns.

3. Dividend Income Satellite — SCHD (Schwab U.S. Dividend Equity ETF)

SCHD adds a growing income layer to your portfolio. It currently yields approximately 3.2–3.5%, with a 10-year historical dividend growth rate of ~10–12% annually. In a portfolio context, SCHD’s defensive characteristics — its heavy exposure to consumer staples, healthcare, and energy — also provide meaningful downside protection. It posted a YTD return of approximately +16.72% in 2026, outpacing VOO during a period of market volatility. For a full breakdown of SCHD’s mechanics and comparison against VYM, see our dedicated article: SCHD vs. VYM: Comparing the Best High-Dividend ETFs in 2026.

4. Income Boost Satellite — JEPQ (JPMorgan Nasdaq Equity Premium Income ETF)

JEPQ generates enhanced monthly income by selling covered call options on Nasdaq-100 holdings. It typically yields 8–11% annually, paid monthly — making it particularly powerful as a cash flow satellite for income-oriented investors. The trade-off is capped upside during strong bull markets, which is why it belongs in the satellite layer — not the core. For a real-world portfolio combining VOO and JEPQ, see: VOO and JEPQ Portfolio Strategy.

Building Your Core and Satellite Portfolio: Step by Step

Now it’s time to build. Follow these five steps to structure your own core and satellite portfolio from scratch.

Step 1 — Define Your Risk Profile and Time Horizon

Before allocating a single dollar, know your constraints. Ask yourself honestly:

- How many years until I need this money? (10, 20, 30+ years?)

- How would I react if my portfolio dropped 25% in 90 days?

- Do I need current income from my investments, or am I purely growth-focused?

Your answers determine your core-to-satellite ratio. A conservative investor with a 10-year horizon might run 80% core / 20% satellite. An aggressive investor with a 25-year horizon might go 60% core / 40% satellite.

Step 2 — Establish Your Core Position First

Start with VOO. This is non-negotiable as your foundation. Set up automatic monthly contributions — even $100 or $200 — and never stop buying, regardless of market conditions. This is the dollar-cost averaging discipline that separates wealthy investors from ones who constantly react to news. To understand why consistency is the most powerful tool in investing, read our guide on Dollar-Cost Averaging Explained.

Step 3 — Select 2–4 Satellite Positions Maximum

More is not better in satellite investing. Over-diversifying satellites defeats their purpose — you end up recreating the index at higher cost and complexity. Choose 2–4 satellites that target different, non-overlapping themes:

- One growth satellite (e.g., QQQM for tech/Nasdaq exposure)

- One sector satellite (e.g., SMH for semiconductors, XLV for healthcare, XLF for financials)

- One income satellite (e.g., SCHD for dividend growth or JEPQ for monthly income)

Step 4 — Set Hard Allocation Limits

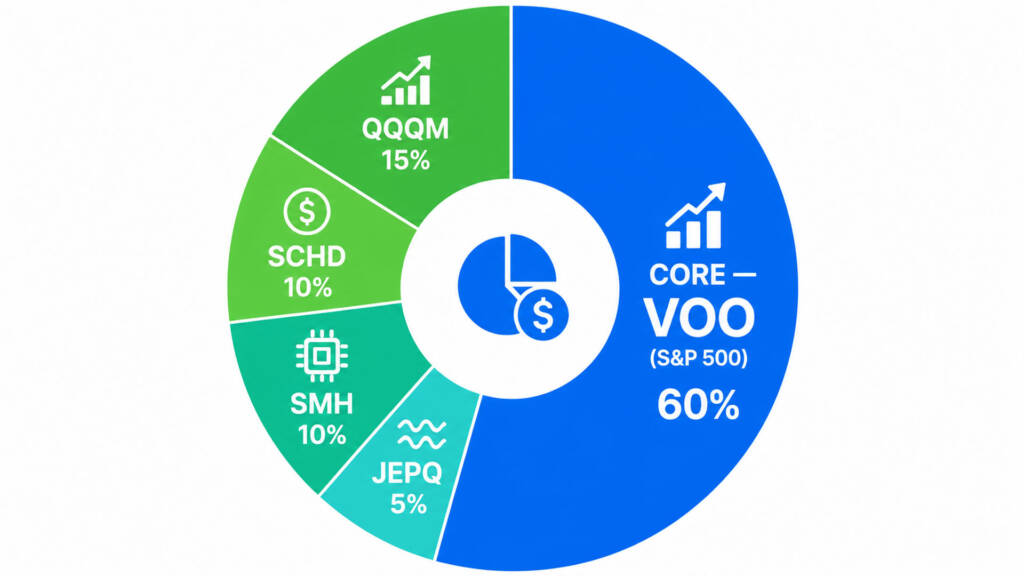

Write down your target allocation and commit to it. A practical starting framework:

| Position | ETF | Allocation |

|---|---|---|

| Core | VOO | 60% |

| Growth Satellite | QQQM | 15% |

| Dividend Satellite | SCHD | 10% |

| Sector Satellite | SMH | 10% |

| Income Satellite | JEPQ | 5% |

Review this allocation every 6–12 months. Rebalance if any single position drifts more than 5 percentage points from its target weight.

Step 5 — Reinvest All Dividends and Stay the Course

The compounding power of dividend reinvestment is staggering over decades. Between VOO’s ~1.1% yield, SCHD’s ~3.5% yield, and JEPQ’s ~8–11% yield, your portfolio generates meaningful income even in the early years — and reinvesting that income accelerates compounding exponentially. For a deeper look at how this mechanism works, explore our article on the Dividend Snowball Effect.

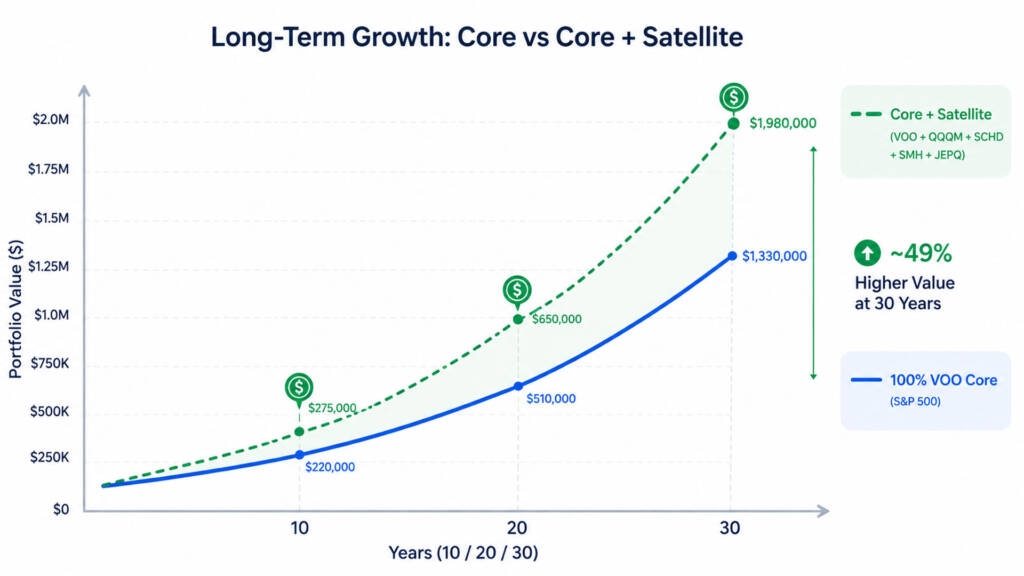

The Compounding Simulation: Core-Only vs. Core + Satellite

Let’s model two portfolios side by side, both starting with a $500 initial investment and $400/month in contributions.

Portfolio A — Core Only (100% VOO):

Using VOO’s 10-year annualized return of approximately 13.5% (including dividends reinvested).

Portfolio B — Core + Satellite:

Using a blended return assumption of ~14.5% (60% VOO at 13.5% + 15% QQQM at ~18% + 10% SCHD at ~11% + 10% SMH at ~22% + 5% JEPQ at ~14%), weighted by allocation.

| Timeframe | Portfolio A (VOO Core Only) | Portfolio B (Core + Satellite) |

|---|---|---|

| 10 Years | ~$99,700 | ~$106,400 |

| 20 Years | ~$434,200 | ~$479,800 |

| 30 Years | ~$1,640,000 | ~$1,910,000 |

Projections based on historical annualized returns. Past performance does not guarantee future results. All figures are for illustrative purposes only.

The 30-year difference of ~$270,000 on identical monthly contributions illustrates why portfolio structure matters — not just asset selection. That additional $270K comes from a disciplined satellite allocation layered on top of a rock-solid core.

Common Mistakes to Avoid

Even a well-designed core and satellite framework can fail if investors make these errors:

- Over-weighting satellites: When a satellite like SMH surges +54% in a year, it’s tempting to add more. Resist. Rebalance back to target weights to lock in gains and maintain your intended risk profile.

- Chasing last year’s winner: Satellite selection should be forward-looking and thesis-driven — not backward-looking and return-chasing.

- Abandoning the core during downturns: During periods like early 2026 when the S&P 500 briefly dipped, many investors panic-sold. Those who held VOO saw it recover to +8.68% YTD by mid-May.

- Ignoring costs: Each satellite adds an expense ratio. Keep total blended portfolio costs below 0.15–0.20%.

- Skipping rebalancing: Without periodic rebalancing, a hot satellite can grow to dominate your portfolio and defeat the entire framework’s purpose.

For a complete guide on the most costly investment errors beginners and intermediate investors make, read: Beginner Investor Mistakes to Avoid.

You can also explore this strategy further through Vanguard’s own research on core-satellite investing and Investopedia’s foundational breakdown of core-satellite strategy mechanics.

Conclusion & Call to Action

A core and satellite portfolio isn’t just a strategy — it’s a philosophy of investing with intention. It gives you the stability of broad market exposure through a core holding like VOO, the growth acceleration of targeted satellites like QQQM and SMH, and the income consistency of dividend-focused positions like SCHD. Most importantly, it gives you a structure — something that holds firm when emotions and market headlines are pushing you in every direction.

With VOO at $679.44, SMH up +54.48% YTD, and QQQM delivering +15.57% YTD as of May 2026, the data makes a compelling case for this framework right now. The market rewards disciplined structure. The only question remaining is: when will you build yours?

What does your current portfolio look like? Are you running a core-only strategy, a full core and satellite framework, or somewhere in between? Share your setup in the comments below — we read every one. And if you’re comparing your dividend satellites, don’t miss our deep-dive: SCHD vs. VYM: Comparing the Best High-Dividend ETFs in 2026.

Frequently Asked Questions

Q1: What is the ideal core and satellite portfolio allocation for a beginner investor?

A1: For most beginners, a simple 70% core / 30% satellite split works well. Start with 70% in VOO as your core, then allocate 30% across 2–3 satellites — for example, 15% QQQM for growth, 10% SCHD for dividend income, and 5% JEPQ for monthly cash flow. This keeps the portfolio manageable, low-cost, and diversified without overwhelming complexity. As your confidence and knowledge grow, you can refine the satellite layer with more targeted sector positions.

Q2: How often should I rebalance a core and satellite portfolio?

A2: Most financial experts recommend reviewing and rebalancing your core and satellite portfolio once or twice per year — or whenever any single position drifts more than 5 percentage points from its target allocation. Annual rebalancing is sufficient for most long-term investors and avoids over-trading costs and tax implications. The key is to rebalance systematically based on your plan, not reactively based on market movements or news headlines.

Q3: Can I build a core and satellite portfolio with a small amount of money — say, $100 per month?

A3: Absolutely — and starting small is far better than waiting until you have “enough.” With fractional share investing available on platforms like IBKR, Fidelity, and Robinhood, you can build a diversified core and satellite portfolio with as little as $50–$100 per month. Allocate $60 to VOO (core), $15 to QQQM, $15 to SCHD, and $10 to JEPQ — and increase contributions as your income grows. The power of compounding rewards consistency far more than it rewards the starting balance. For a practical example, see our article on Investing $50 a Month in VOO.

Financial Disclaimer: This article is intended for educational and informational purposes only. The portfolio frameworks, compounding simulations, and ETF data presented here are based on historical performance and publicly available market data as of May 2026. Nothing in this article constitutes personalized financial advice, a recommendation to buy or sell any specific security, or a guarantee of future investment returns. All investing involves risk, including the possible loss of principal. Satellite investments carry additional risks compared to broad-market index funds, including higher volatility, sector concentration risk, and liquidity risk. Always conduct your own due diligence and consult with a licensed financial advisor or registered investment professional before making any investment decisions.