Most people think you need thousands of dollars to start building real wealth through dividends. They watch the market from the sidelines, convinced that meaningful passive income is out of reach. The truth is, the dividend snowball effect makes even $50 a month a powerful wealth-building engine — if you understand how compounding works and stay consistent.

Key Takeaways:

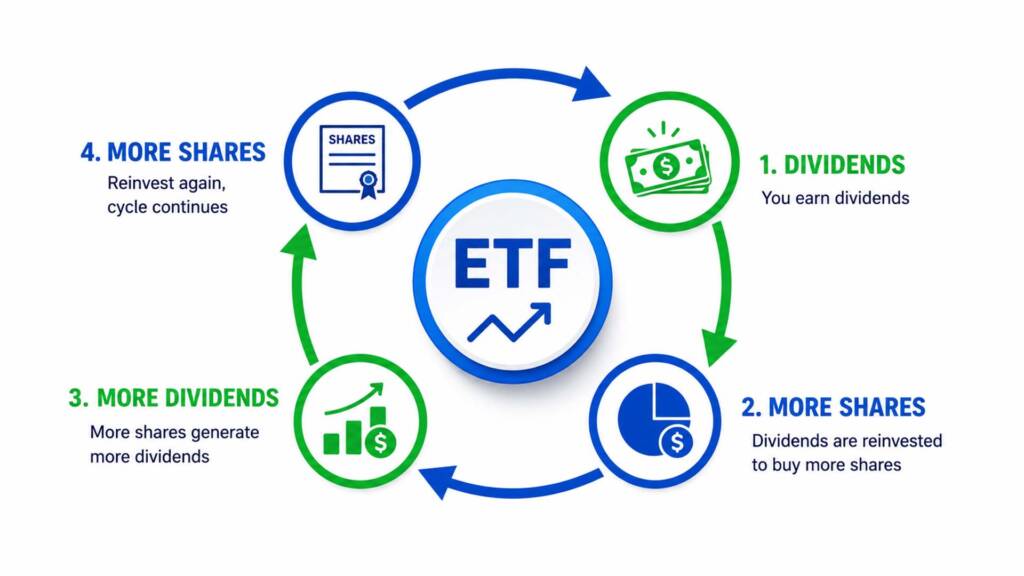

- The dividend snowball effect uses reinvested dividends to buy more shares, which then generate even more dividends — compounding exponentially over time.

- You can start with as little as $50–$100/month in broad-market ETFs like VOO or dividend-focused ETFs like SCHD to set the snowball in motion.

- Consistent contributions, dividend reinvestment (DRIP), and time are the three pillars that transform small investments into significant passive income streams.

What Is the Dividend Snowball Effect?

The dividend snowball effect is the process by which reinvested dividend payments generate progressively larger dividends over time. Think of it like a snowball rolling downhill. At first, it’s tiny and slow. But as it rolls, it picks up more snow, grows larger, moves faster, and eventually becomes unstoppable — even though you may have only packed the first handful of snow yourself.

When you reinvest dividends instead of cashing them out, those payments buy additional shares. Those new shares then produce their own dividends in the next cycle. Each reinvestment cycle slightly increases your total share count, and since dividends are paid per share, your next payout is always a little bigger. Over years and decades, this compounding creates dramatically accelerating growth that’s nearly impossible to replicate through savings accounts alone.

The Math Behind the Snowball

The S&P 500 has delivered a long-term average annual total return of approximately 10.4% (with dividends reinvested) since 1957. That historical figure is the backbone of every dividend snowball projection. Without dividends being reinvested, returns are considerably lower — which proves that the reinvestment component is not optional if you want maximum compounding.

Why Small Investments Are Enough to Start

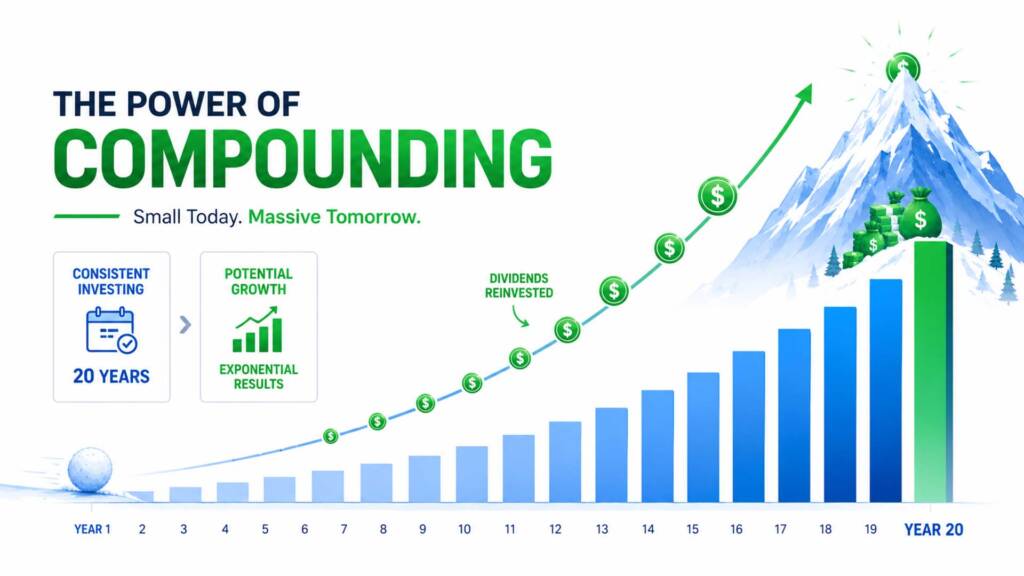

A common beginner mistake is waiting until you have a “significant” amount of capital before investing. But the dividend snowball effect rewards time in the market above all else. Even $50 a month, invested consistently into the right vehicles, can grow into a meaningful income stream over a 20–30 year horizon.

Here’s a simple, data-driven simulation based on current figures:

| Monthly Contribution | Annual Return (Historical ~10%) | After 20 Years | After 30 Years |

|---|---|---|---|

| $50/month | 10% | ~$37,900 | ~$113,000 |

| $100/month | 10% | ~$75,900 | ~$226,000 |

| $250/month | 10% | ~$189,800 | ~$565,000 |

| $500/month | 10% | ~$379,600 | ~$1,130,000 |

These are projected outcomes based on historical S&P 500 averages. They do not represent guaranteed returns. However, they illustrate how small, consistent investments harness the dividend snowball effect over time.

The key is starting now, not waiting for a bigger paycheck or a “perfect” entry point.

The Three Engines of Your Dividend Snowball

1. Adding Fresh Capital (Packing the Snow)

Your monthly contributions are the foundation of the snowball. In the early years of your investing journey, your personal savings rate matters more than your investment returns. The more you consistently contribute, the larger your base of shares, and the larger your dividend payout becomes. Automate your investments so contributions happen without requiring willpower.

- Set up automatic transfers on payday to your brokerage account.

- Invest every month regardless of whether markets are up or down.

- Even modest increases — adding $10 more per month each year — dramatically change your 20-year outcome.

2. Reinvesting Dividends (Rolling Downhill)

This is the core mechanism of the dividend snowball effect. When you enroll in a Dividend Reinvestment Plan (DRIP), your broker automatically uses every dividend payment to purchase more shares of the same ETF or stock — usually at no extra commission.

Charles Schwab, Fidelity, and Interactive Brokers all offer free DRIP enrollment. For VOO holders, the most recent Q1 2026 dividend was $1.87 per share, paid on March 31, 2026. Every one of those dollars, when reinvested, buys a fractional share that will generate its own dividend in Q2, Q3, and Q4.

Pro tip: Never turn off your DRIP during market downturns. Falling prices mean your dividends buy more shares — which actually accelerates your snowball.

3. Focusing on Dividend Growth (Snowball to Avalanche)

Not all dividend yields are created equal. What separates a slow-growing snowball from an avalanche is dividend growth rate — how much the company or ETF raises its dividend payout each year. A 3% yield that grows at 7% annually will eventually far outpace a 5% yield that stays flat.

This is precisely why dividend growth ETFs like SCHD are so popular. As of May 2026, SCHD offers a dividend yield of approximately 3.34% and just raised its Q1 2026 dividend by 3.3% year-over-year to $0.2569 per share. That kind of consistent annual increase is what turns a modest snowball into an avalanche over a decade.

Choosing the Right ETFs to Build Your Snowball

Not all ETFs serve the same role in a dividend snowball strategy. For beginners and international investors targeting US markets, a two-layer approach works best.

Layer 1: VOO as Your Stable Core

VOO (Vanguard S&P 500 ETF) should be the primary, stable foundation of your portfolio. As of May 2026, VOO trades around $678 per share with a dividend yield of approximately 1.05%, paying $7.12 annually per share. While VOO’s yield is modest, its long-term total return (price appreciation + dividends reinvested) has historically driven most of the S&P 500’s ~10.4% average annual gain.

For a deeper understanding of ETF basics, read our guide: What Is ETF Investing?

Also explore how VOO functions as a core holding in our article: VOO ETF as a Core Portfolio Strategy

Layer 2: SCHD for Dividend Income

SCHD (Schwab U.S. Dividend Equity ETF) complements VOO by providing a significantly higher dividend yield and a strong track record of dividend growth. Its current 3.34% yield with consistent annual raises makes it a powerful snowball accelerator alongside VOO’s growth engine.

For a detailed breakdown of how to combine these two ETFs, see our portfolio walkthrough: VOO and JEPQ Portfolio Guide

Wondering how to start with just $50/month? Read: Investing $50 a Month in VOO

How to Set Up Your Dividend Snowball in 5 Steps

Getting your dividend snowball rolling is simpler than most beginners expect. Follow these five steps to build yours today:

- Open a brokerage account — Use a trusted global platform like Interactive Brokers (IBKR), which offers fractional share investing, commission-free ETF access, and DRIP support — so you can buy into VOO or SCHD with as little as $1. IBKR is especially well-suited for international investors targeting US markets, offering a regulated, SEC-compliant environment with SIPC protection up to $500,000.

- Start with a core ETF — Begin with VOO as your primary holding. This gives you broad S&P 500 exposure with built-in dividend payments.

- Add a dividend-growth ETF — Layer SCHD into your portfolio for a higher yield and faster snowball acceleration.

- Enable DRIP immediately — Log in to your brokerage settings and turn on dividend reinvestment for every position.

- Automate monthly contributions — Schedule a fixed monthly transfer on payday so the process runs without willpower or discipline.

Avoid the common traps that derail new investors by reading: Top Beginner Investor Mistakes to Avoid

Growth vs. Dividend Investing: Which Is Better?

A question many beginners ask is whether a dividend snowball strategy is better than pure growth investing. The honest answer is: both have merit, and the best portfolios often include both. Growth stocks (like those in QQQ) reinvest their profits back into the business rather than paying dividends, which can produce extraordinary capital gains.

However, dividend investing adds an important psychological and mechanical advantage — you see your reinvested dividends working, which reinforces long-term commitment and makes it less tempting to sell during downturns. For a full breakdown of the trade-offs, read our article: Growth vs. Dividend Investing: What’s Right for You?

For authoritative research on dividend reinvestment strategies, the Vanguard Investor Education Center and Investopedia’s Compounding Guide offer excellent supplemental reading.

Real-World Dividend Snowball Simulation

Let’s make this concrete with a real-world simulation using current 2026 data.

Scenario: You invest $200/month split between VOO and SCHD (60/40). You reinvest all dividends and assume a blended annual total return of 9% (conservative, below the historical 10.4% average).

| Year | Total Invested | Portfolio Value (9% return) | Annual Dividend Income |

|---|---|---|---|

| Year 1 | $2,400 | ~$2,510 | ~$60 |

| Year 5 | $12,000 | ~$15,100 | ~$380 |

| Year 10 | $24,000 | ~$38,600 | ~$970 |

| Year 20 | $48,000 | ~$133,800 | ~$3,350 |

| Year 30 | $72,000 | ~$366,400 | ~$9,160 |

By year 30, your $200/month habit generates over $9,000 in annual dividend income — a figure that grows every single year without you lifting a finger, purely through the dividend snowball effect. These are projected figures based on historical averages, not guaranteed returns.

Common Dividend Snowball Mistakes to Avoid

Even a well-intentioned strategy can underperform if you fall into these traps:

- Chasing high yields blindly — A 10%+ yield often signals financial distress or an unsustainable payout. Focus on yield + dividend growth rate together.

- Turning off DRIP during downturns — Market crashes are the best time to let dividends buy more shares cheaply. Never stop the reinvestment.

- Selling during volatility — The S&P 500 returned -18.11% in 2022, then bounced back with +26.29% in 2023. Selling locks in losses and kills your snowball momentum.

- Ignoring tax efficiency — Hold dividend-paying ETFs in tax-advantaged accounts (Roth IRA, 401k) whenever possible to maximize reinvestment impact.

- Not starting because “the amount is too small” — $50/month invested today is worth more than $500/month invested five years from now, due to compounding time advantage.

Conclusion & Call to Action

The dividend snowball effect is one of the most powerful and accessible wealth-building strategies available to everyday investors. You don’t need a large salary, a financial advisor, or years of market experience. You need consistency, patience, and the discipline to reinvest every dividend you receive. Start with as little as $50 a month in VOO or SCHD, enable your DRIP, and let compounding do the heavy lifting over time.

Your snowball starts small — but given enough time rolling downhill, it becomes unstoppable.

Ready to start your dividend snowball journey? Leave a comment below sharing your current monthly investment amount or your target passive income goal. Or, continue building your knowledge by reading our related guide: VOO and JEPQ Portfolio Strategy.

Frequently Asked Questions

Q1: How long does it take to see the dividend snowball effect work?

Most investors begin noticing meaningful compounding acceleration around the 5–7 year mark, though the mathematical effect starts from day one. The first few years are about building your base share count through consistent contributions. By year 10+, dividend reinvestment adds a compounding layer that increasingly accelerates growth.

Q2: Can I build a dividend snowball with ETFs instead of individual stocks?

Absolutely — and for most beginners, ETFs are the preferred vehicle. ETFs like VOO and SCHD offer instant diversification, lower risk than single stocks, and consistent quarterly dividends that are ideal for DRIP enrollment. Individual dividend stocks require more research and carry concentration risk.

Q3: What is the best brokerage to start a dividend snowball in 2026?

For both US-based and international investors, Interactive Brokers (IBKR) is one of the top-rated platforms for dividend ETF investing. It offers fractional shares, automatic dividend reinvestment, low commissions on US-listed ETFs, and SIPC protection up to $500,000 — making it ideal for building a long-term dividend snowball with small capital. You can open an account and start investing in VOO or SCHD with as little as $1.

Financial Disclaimer: This article is for educational and informational purposes only and does not constitute financial, investment, or tax advice. All numerical examples are based on historical data and projected outcomes — they do not represent guaranteed returns. Past performance is not indicative of future results. Always consult a qualified financial advisor before making investment decisions.