Most new investors share one crippling fear: “What if I invest right before a market crash?” That fear keeps countless people sitting on the sidelines — watching inflation eat away at their savings — while the market quietly compounds wealth for everyone else. Here is the hard truth: trying to time the market perfectly is a losing game, even for Wall Street professionals. The solution is a simple, proven, and completely stress-free strategy called dollar-cost averaging explained in full detail right here. By the end of this article, you will understand exactly how DCA works, why it removes investing anxiety, and how to apply it to ETFs like VOO starting today.

Key Takeaways:

- Dollar-cost averaging (DCA) means investing a fixed dollar amount at regular intervals, regardless of market conditions — removing the pressure to “time” your entry perfectly.

- Consistency beats timing. Historical data shows the S&P 500 has delivered an average annual return of approximately 10% over the long term, rewarding those who stayed invested steadily.

- ETFs like VOO are ideal DCA vehicles because they offer instant diversification, low expense ratios, and a track record of long-term growth aligned with the US economy.

What Is Dollar-Cost Averaging?

Dollar-cost averaging is the practice of investing a fixed dollar amount into an asset — like a stock, ETF, or mutual fund — at regular, scheduled intervals, regardless of whether the market is going up or down. The US Securities and Exchange Commission defines it simply as “investing your money in equal portions, at regular intervals, regardless of the ups and downs in the market.”

The mechanics are elegantly simple. When prices are high, your fixed dollar amount buys fewer shares. When prices are low, that same fixed amount buys more shares. Over time, this automatic behavior lowers your average cost per share — a concept known as the “averaging” effect that gives the strategy its name.

This approach is the polar opposite of market timing. Instead of agonizing over charts and economic news cycles, you set a schedule and let automation do the work. As Fidelity Investments describes it, your purchases happen “regardless of the changes in price for the stock or other investment, potentially helping reduce the impact of volatility on the overall purchase.”

Why Most Investors Fail Without a System

The biggest enemy of the retail investor is not the market — it is emotion. Fear and greed drive most amateur investing decisions. Investors panic-sell during downturns and buy aggressively at market peaks. This cycle destroys returns and causes significant financial damage over time.

Consider what happened in early 2022: the S&P 500 dropped 18.19% for the full year. Many investors who tried to time the bottom either sold too early or bought too late. Meanwhile, disciplined DCA investors kept buying throughout the dip — and when the market roared back +26.32% in 2023 and +24.98% in 2024, those extra discounted shares multiplied their gains.

Without a system, investing becomes reactive and emotional. DCA creates a system — a repeatable, automated, emotion-proof process that keeps your wealth-building engine running regardless of headlines or market noise. This is one of the most common beginner investor mistakes to avoid: letting fear override your long-term plan.

Dollar-Cost Averaging Explained: How It Actually Works

Let’s walk through a real-world example. Imagine you commit to investing $200 every month into VOO, the Vanguard S&P 500 ETF.

| Month | VOO Price | Shares Bought | Total Invested |

|---|---|---|---|

| January | $520 | 0.385 | $200 |

| February | $490 | 0.408 | $400 |

| March | $460 | 0.435 | $600 |

| April | $475 | 0.421 | $800 |

| May | $510 | 0.392 | $1,000 |

| June | $535 | 0.374 | $1,200 |

After six months, you’ve invested $1,200 and accumulated approximately 2.415 shares. Your average cost per share is roughly $497 — lower than the June price of $535. An investor who waited and tried to buy at the “perfect” June price spent more per share than you did. Your patience and consistency paid off.

The Power of Compounding With DCA

DCA becomes truly powerful when compounding enters the equation. External Link: Investopedia — Dollar-Cost Averaging Compounding means your returns generate their own returns, accelerating growth exponentially over time.

The VOO ETF has delivered an average annual return of approximately 10.24% (compound annual growth rate) over the past 30 years as of April 2026. Using that historical benchmark, here is how a simple $300/month DCA plan into VOO might project:

| Time Horizon | Total Invested | Projected Portfolio Value (10% avg. annual return) |

|---|---|---|

| 5 Years | $18,000 | ~$23,231 |

| 10 Years | $36,000 | ~$61,453 |

| 20 Years | $72,000 | ~$229,085 |

| 30 Years | $108,000 | ~$678,146 |

⚠️ These are projected outcomes based on historical average returns. Past performance does not guarantee future results.

The difference between $108,000 invested and a potential $678,146 portfolio is the compounding effect working silently over decades. This is not fantasy — this is the historical math of owning a broad-market index. You can explore this concept further in our article on investing $50 a month in VOO — proof that even small, consistent investments create enormous outcomes.

Why ETFs Are the Perfect DCA Vehicle

Not all investments are equally suited for DCA. Individual stocks carry company-specific risk — a single earnings miss or scandal can wipe out years of gains. Broad-market ETFs, by contrast, spread your investment across hundreds or thousands of companies simultaneously. If one company underperforms, the overall index barely flinches.

For a deep understanding of how ETFs function, read our foundational guide: What Is ETF Investing?

The three most DCA-friendly ETFs for long-term wealth building include:

- VOO (Vanguard S&P 500 ETF) — Tracks 500 of America’s largest companies. Expense ratio: 0.03%. Historical 30-year CAGR: ~10.24%. This should serve as the core holding (60%+) of any long-term DCA portfolio.

- QQQM (Invesco Nasdaq-100 ETF) — Focuses on the top 100 Nasdaq-listed tech companies. Higher growth potential with slightly higher volatility. Ideal as a growth booster (15–20% allocation).

- SCHD (Schwab U.S. Dividend Equity ETF) — Tracks dividend-paying US stocks. Provides income and stability, balancing out the growth-oriented holdings.

A DCA strategy anchored in VOO reflects one of the most time-tested investment principles: own the market, don’t try to beat it. For a detailed portfolio structure combining VOO with income-generating ETFs, read our guide on the VOO ETF core portfolio.

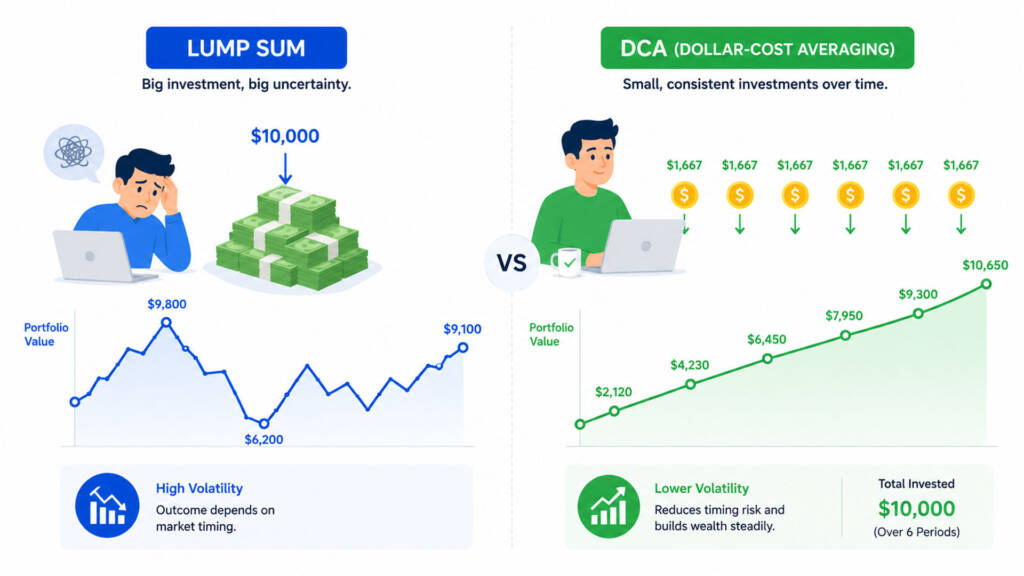

Dollar-Cost Averaging vs. Lump Sum Investing

A common debate among investors is: should you DCA or invest a lump sum? The data offers a nuanced answer. Morgan Stanley’s analysis of over 1,000 historical seven-year periods found that lump-sum investing generated slightly higher annualized returns in more than 56% of cases — by an average of roughly 0.42% for stock-heavy portfolios.

However, that finding assumes you have a large sum of capital ready to deploy and the psychological discipline to hold through an immediate drawdown. For the majority of retail investors who are building wealth through a monthly paycheck, lump sum investing is simply not realistic.

More importantly, DCA’s true advantage is behavioral. Research consistently shows that investors who experience a large early loss after a lump-sum investment are far more likely to panic-sell and lock in permanent losses. DCA investors, however, remain calm because they know they have future purchases planned at potentially lower prices. As Morgan Stanley concluded, “keeping all your money on the sidelines for fear of getting it wrong may be the least advisable approach.” DCA solves that by keeping you consistently invested.

| Factor | DCA | Lump Sum |

|---|---|---|

| Best for | Paycheck investors, beginners | Windfall/inheritance investors |

| Market timing risk | Very low | High |

| Psychological stress | Low | High |

| Long-term return potential | Slightly lower (on average) | Slightly higher (on average) |

| Discipline required | Low (automated) | High |

| Risk of panic selling | Low | Higher |

How to Start Dollar-Cost Averaging in 4 Simple Steps

Starting a DCA strategy is far simpler than most beginners expect. Here is a clear, actionable path:

Step 1: Choose your ETF(s)

Start with a core position in VOO as your primary holding. You may also consider comparing growth vs. dividend investing to decide whether to add a dividend ETF like SCHD alongside your growth allocation.

Step 2: Set your fixed monthly amount

Choose an amount you can comfortably invest every month without affecting your emergency fund. Even $50/month is a powerful starting point — the habit matters more than the amount in the early stages.

Step 3: Automate your purchases

Use a brokerage account that supports recurring automatic investments. Platforms like Fidelity, Charles Schwab, and Interactive Brokers (IBKR) allow you to schedule automatic purchases on a weekly or monthly basis. Automation removes emotion entirely from the equation.

Step 4: Stay the course and rebalance annually

Do not check your portfolio every day. DCA is a long-game strategy. Review your allocation once or twice per year and rebalance if your target weights shift significantly. If you want to build a more structured portfolio around your DCA plan, explore our guide to the VOO and JEPQ portfolio for a balanced growth-and-income approach.

DCA in a Volatile Market: 2026 Context

Market context matters. As of May 2026, the S&P 500 has navigated a period of moderate volatility — with year-to-date performance showing a -4.33% price return through Q1 2026, followed by recovery momentum into Q2. This is precisely the environment where DCA proves its worth.

Investors who paused their contributions during the early 2026 dip missed the recovery bounce. Those who kept their automatic monthly purchases running accumulated extra shares at discounted prices — and are now positioned for amplified gains as the market recovers. VOO’s long-term average annual return since inception sits at approximately 14.70% (including dividends) as of April 2026. Short-term volatility is simply noise against that long-term signal.

The current environment is a reminder that time in the market always beats timing the market — a principle that DCA enforces by design.

Conclusion & Call to Action

Dollar-cost averaging is not a complicated hedge fund strategy. It is a disciplined, automated, and stress-free approach to building real wealth over time — accessible to anyone with a brokerage account and a willingness to stay consistent. By investing a fixed amount regularly into broad-market ETFs like VOO, you automatically buy more shares when prices dip and let compounding do the heavy lifting over decades.

The S&P 500’s historical returns — averaging over 10% annually across 30 years — are not a secret. The secret is simply showing up every month, regardless of what the headlines say.

Ready to put this strategy into action? Start exploring our related guides below, and drop a comment sharing how much you plan to invest monthly — our community would love to hear from you!

👉 Related Reading:

- What Is ETF Investing? A Complete Beginner’s Guide

- Investing $50 a Month in VOO — What Happens Over 10 Years?

- The Dividend Snowball Effect: How Reinvesting Changes Everything

Frequently Asked Questions

Q1: Is dollar-cost averaging a good strategy for beginners who are new to the stock market?

A1: Yes, dollar-cost averaging is widely considered one of the best strategies for beginners. It eliminates the stress of timing the market, requires no technical analysis, and works with any budget. By automating small, regular contributions into a diversified ETF like VOO, beginners build wealth steadily without needing to predict market movements.

Q2: How much money do I need to start dollar-cost averaging into ETFs?

A2: You can begin DCA with as little as $1 if your broker supports fractional share investing. Most major US brokerages — including Fidelity, Schwab, and IBKR — allow fractional purchases, meaning you can invest a fixed dollar amount (e.g., $50 or $100/month) into high-priced ETFs like VOO without needing to afford a full share. The key is consistency, not the size of each contribution.

Q3: What is the difference between dollar-cost averaging and lump sum investing?

A3: Dollar-cost averaging spreads your investment over time in fixed installments, while lump sum investing deploys all available capital at once. Lump sum investing has historically outperformed DCA in approximately 56% of cases, but only for investors with large capital ready to deploy and the psychological discipline to hold through volatility. For most working investors building wealth from a paycheck, DCA is the more practical, lower-stress, and more sustainable approach.

Financial Disclaimer: This article is intended for educational and informational purposes only and does not constitute financial advice, investment advice, or a recommendation to buy or sell any security. All figures mentioned represent historical or projected outcomes and do not guarantee future results. Investment in securities involves risk, including the possible loss of principal. Always conduct your own due diligence and consult a licensed financial advisor or registered investment professional before making any investment decisions.