You have started investing in stocks and ETFs — and then the market drops 15% in two weeks. Your portfolio turns red. Your stomach drops. You wonder whether you made a terrible mistake. That fear is real, and millions of beginner investors experience it every single year. The solution is not to panic-sell. Instead, it is to build a smarter, more balanced portfolio that can weather volatility without derailing your long-term goals. For many investors, bond ETFs are that balancing tool — and in this guide to bond ETF beginners 2026, you will learn exactly how they work, which ones to consider, and how to decide if they belong in your portfolio right now.

Key Takeaways:

- Bond ETFs reduce portfolio volatility by providing a low-correlation asset class that often holds its value — or rises — when stocks fall.

- The Federal Reserve’s current target rate of 3.5%–3.75% makes bond yields historically attractive, with funds like BND yielding ~4.1% and TLT offering a yield-to-maturity of ~5.04%.

- Inflows into bond ETFs are up 50% in 2026 vs. the prior year, signaling that institutional and retail investors alike are rapidly rediscovering fixed income.

What Is a Bond ETF?

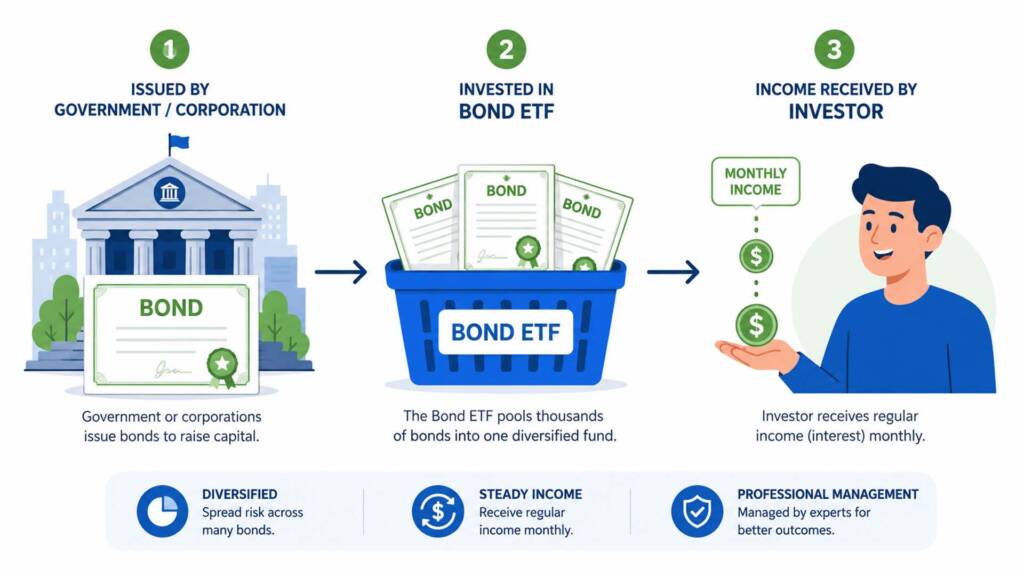

A bond ETF (Exchange-Traded Fund) is a basket of bonds packaged into a single fund that trades on a stock exchange like a regular stock. Instead of buying one government or corporate bond — which can cost $1,000 to $5,000 minimum — you buy one share of a bond ETF for a fraction of the price.

Think of it this way: a bond ETF is like a fruit basket. Rather than buying one apple (a single bond), you buy a basket filled with apples, oranges, and bananas — hundreds of different bonds from different issuers, all in one purchase. This instantly gives you diversification, liquidity, and lower entry costs — all critical advantages for beginner investors.

Bond ETFs typically pay monthly distributions (income from the interest on the bonds they hold), making them a popular tool for passive income strategies. To understand more about how ETFs work in general, read our foundational guide: What Is ETF Investing?

How Bonds Work: The Basics Every Beginner Needs to Know

Before investing in bond ETFs, you need to understand the asset class underneath them. A bond is essentially a loan you give to a government or corporation. In return, they pay you interest (the coupon) at regular intervals, then return your principal at a set maturity date.

There are three key concepts every beginner must understand:

- Yield: The annual interest income a bond pays, expressed as a percentage of its price. Higher yield typically means more income — but also more risk.

- Duration: A measure of how sensitive a bond’s price is to changes in interest rates. Longer duration = greater price swings when rates change.

- Credit Quality: Bonds are rated from AAA (safest) down to “junk” (speculative). Investment-grade bonds carry lower risk; high-yield bonds pay more but carry more default risk.

The Crucial Inverse Relationship: Bond Prices vs. Interest Rates

Here is the concept that trips up most beginners. When interest rates rise, bond prices fall — and when rates fall, bond prices rise. This inverse relationship is critical for 2026 planning.

The Federal Reserve currently holds its benchmark rate at 3.5%–3.75% — unchanged for three consecutive meetings as of June 2026. The market expects rates to stabilize near this level through the end of 2026. This means bond prices are not under the same upward pressure they faced during 2022–2023 rate hikes — making now a much more attractive entry point for bond ETF investors.

Why Bond ETFs Are Surging in Popularity in 2026

Bond ETFs are not just for retirees anymore. According to BlackRock’s 2026 data, bond ETF inflows are up 50% year-over-year, with over $200 billion in net inflows recorded through May 2026 alone. Here is why the trend is accelerating:

- Attractive yields: With the Fed rate at 3.5%–3.75%, bond ETFs now offer meaningful income — a far cry from the near-zero yields of 2020–2021.

- Market volatility: Tariff uncertainty, trade disruptions, and equity market swings in early 2026 pushed investors toward defensive assets.

- Portfolio ballast: High-quality bonds have historically shown a low or negative correlation with stocks during market crashes — providing a real cushion.

- Accessibility: Modern brokers allow you to buy bond ETFs with as little as one share, sometimes even fractionally.

The Best Bond ETFs for Beginners in 2026

Not all bond ETFs are created equal. Below is a curated comparison of the most beginner-friendly options, based on current data as of June 2026.

| ETF | Full Name | Expense Ratio | Yield / YTM | Duration | Best For |

|---|---|---|---|---|---|

| BND | Vanguard Total Bond Market ETF | 0.03% | ~4.10% | ~6 yrs | Total bond market, beginners |

| AGG | iShares Core U.S. Aggregate Bond ETF | 0.03% | ~4.2% | ~6 yrs | Broad investment-grade exposure |

| TLT | iShares 20+ Year Treasury Bond ETF | 0.15% | 5.04% YTM | ~26 yrs | Income seekers, rate-play investors |

| SGOV | iShares 0-3 Month Treasury Bill ETF | 0.09% | ~4.5% | <1 yr | Capital preservation, ultra-safe |

| LQD | iShares iBoxx $ Investment Grade Corporate Bond ETF | 0.14% | ~5.2% | ~8 yrs | Corporate bond income |

| FBND | Fidelity Total Bond ETF | 0.36% | ~4.8% | ~6 yrs | Active management with Morningstar Gold rating |

BND — Best Overall for Beginners

The Vanguard Total Bond Market ETF (BND) is the go-to recommendation for most beginners. It tracks the Bloomberg U.S. Aggregate Float Adjusted Index — giving you exposure to over 10,000 U.S. investment-grade bonds, including Treasuries, government agency bonds, and corporate bonds.

Its expense ratio of just 0.03% is among the lowest in the industry. At a current yield of approximately 4.10%, BND offers meaningful income at very low cost. Furthermore, its moderate 6-year duration makes it far less volatile than a long-bond fund like TLT.

AGG — The Industry Standard

The iShares Core U.S. Aggregate Bond ETF (AGG) is virtually identical to BND in scope and cost. Both track similar benchmarks and are widely used by financial advisors as the “default” bond allocation in balanced portfolios. If your broker offers commission-free trading on iShares products, AGG may be the more cost-efficient choice for you.

TLT — Higher Yield, Higher Risk

The iShares 20+ Year Treasury Bond ETF (TLT) is for investors who want more income and can stomach more volatility. TLT currently offers a yield-to-maturity of 5.04% — but its 26-year average maturity means its price swings significantly with rate changes. TLT fell -31.41% in 2022 alone when rates spiked. Beginners should approach TLT cautiously.

SGOV — The Safe Parking Spot

The iShares 0-3 Month Treasury Bill ETF (SGOV) invests in ultra-short Treasury bills. It is essentially a cash-equivalent fund — highly stable, highly liquid, and currently yielding around 4.5%. It is an excellent choice for the “safe” portion of a portfolio or for investors waiting for better opportunities in stocks.

Should You Add Bonds to Your Portfolio? (The Honest Answer)

The answer depends almost entirely on your age, time horizon, and risk tolerance. Here is a simple framework to help you decide:

✅ You SHOULD consider bonds if:

- You are 40 years old or older and need to start protecting accumulated wealth

- You experience significant anxiety during stock market drawdowns

- You want monthly income to supplement dividend payments from equity ETFs

- You hold a large equity position (e.g., VOO-heavy) and want to reduce overall portfolio volatility

- You have a short-to-medium time horizon of 3–7 years for a specific financial goal

❌ You may want to LIMIT bonds if:

- You are in your 20s or early 30s with a 30+ year investment horizon — time is your ultimate risk buffer

- You are in an aggressive growth phase and can tolerate drawdowns in exchange for higher long-term returns

- You already hold dividend ETFs like SCHD that provide income with some equity upside (read our SCHD ETF Review 2026 for comparison)

The Classic Portfolio Allocation Models

Financial theory has long guided investors with simple allocation rules. Here are two starting frameworks:

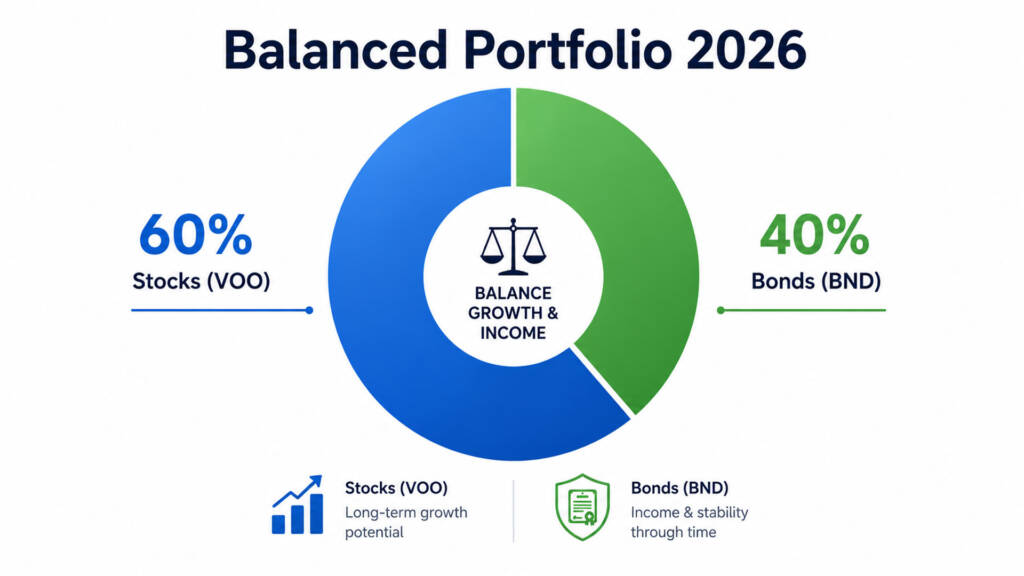

The 60/40 Portfolio

The most traditional approach allocates 60% to stocks and 40% to bonds. This model aims to capture equity growth while bonds provide stability and income during downturns. A simple 60/40 implementation might look like:

- 60% VOO (S&P 500 exposure, core growth engine)

- 40% BND or AGG (total bond market, income and stability)

The Age-Based Rule of Thumb

A common heuristic says: your bond allocation percentage should roughly equal your age. A 30-year-old holds 30% bonds; a 60-year-old holds 60% bonds. This rule is a starting point — not a rigid formula — but it provides a simple, intuitive framework for beginners. For a deeper look at building your full portfolio structure, explore our Core and Satellite Portfolio strategy guide.

A Simple Bond ETF Compounding Simulation

Let’s look at a realistic income simulation using current data. Assume you invest $10,000 in BND today, with a current yield of ~4.10%, and reinvest all monthly distributions.

⚠️ These are projected outcomes based on current yield and flat price assumption. Actual returns will vary based on interest rate movements and price appreciation or depreciation.

| Year | Projected Portfolio Value (Dividends Reinvested) |

|---|---|

| Year 1 | ~$10,410 |

| Year 3 | ~$11,278 |

| Year 5 | ~$12,219 |

| Year 10 | ~$14,930 |

| Year 15 | ~$18,244 |

This may look modest compared to SCHD or VOO’s historical equity returns — and that is entirely by design. Bonds are not meant to be your wealth-building engine. Instead, they are the shock absorber that keeps your overall portfolio stable so your equity positions have time to recover during downturns.

Now combine a $10,000 BND position with a $20,000 VOO position in a simple 60/40 split. During a hypothetical -30% stock market crash, your VOO position drops to $14,000, but your BND position holds or slightly gains, cushioning the overall portfolio loss from -30% to approximately -18%. That protection can be the difference between panic-selling at the bottom and staying invested for the eventual recovery. For more on what to do when markets crash, read our guide: What to Do When the Stock Market Crashes.

Risks Every Beginner Must Understand

Bond ETFs are significantly safer than stocks — but they are not risk-free. Be aware of these key risks:

- Interest Rate Risk: If rates rise unexpectedly, bond prices fall. Long-duration funds like TLT are most vulnerable. Short-duration funds like SGOV are nearly immune to this risk.

- Credit Risk: Corporate bond ETFs like LQD carry the risk that issuers could default. Treasury ETFs like BND and TLT carry virtually zero default risk, as they are backed by the U.S. government.

- Inflation Risk: If inflation outpaces your bond yield, your real (inflation-adjusted) return becomes negative. Monitor the Consumer Price Index alongside your bond holdings.

- Withholding Tax for International Investors: Non-U.S. investors may face a 30% withholding tax on bond ETF income distributions unless a reduced tax treaty rate applies. Factor this into your net yield calculation.

How to Start Investing in Bond ETFs

Getting started is straightforward. Follow these steps:

- Open a brokerage account that provides access to U.S. markets. For international investors, Interactive Brokers is widely regarded as the best low-cost option. Open your account here: IBKR Referral — Start Investing in Bond ETFs

- Decide on your bond allocation using the age-based or 60/40 framework above.

- Choose your bond ETF — for most beginners, start with BND or AGG for simplicity and cost-efficiency.

- Use Dollar-Cost Averaging (DCA) — invest a fixed amount monthly rather than timing the market. Read our Dollar-Cost Averaging Explained guide for a step-by-step walkthrough.

- Reinvest distributions — set up automatic dividend reinvestment (DRIP) if your broker supports it.

- Rebalance annually — if stocks run up and bonds drift below your target %, rebalance back. Read our guide on How Often to Rebalance Your Portfolio for a practical schedule.

For additional reading on avoiding the most common pitfalls, check out our article on Beginner Investor Mistakes to Avoid before making your first purchase.

Conclusion & Call to Action

Bonds are not glamorous. They will not make your portfolio explode upward in a bull market. However, they will protect your wealth when markets get turbulent — and in 2026, with equities running hot and macro uncertainty still present, that protection is more valuable than ever.

For bond ETF beginners in 2026, the path is clear: start simple. BND or AGG give you the entire U.S. investment-grade bond market at essentially zero cost. Combine them with a core equity position in VOO, and you have the foundation of a genuinely resilient, balanced portfolio.

Are you already holding bonds in your portfolio, or are you still 100% in stocks? Drop a comment below — I’d love to hear your current allocation and your biggest question about fixed income. And if you’re ready to take the next step, read our companion article: How to Build a Dividend Portfolio in 2026 to see how bonds fit into a complete income-generating strategy.

FAQs

Q1: What is the best bond ETF for beginners in 2026?

A1: For most beginners in 2026, BND (Vanguard Total Bond Market ETF) and AGG (iShares Core U.S. Aggregate Bond ETF) are the top choices. Both have expense ratios of just 0.03%, offer broad exposure to thousands of investment-grade U.S. bonds, and currently yield approximately 4.1–4.2%. They are simple, liquid, and beginner-friendly. If you want ultra-safe, short-term exposure, SGOV (0–3 Month Treasury Bill ETF) at ~4.5% yield is also excellent for capital preservation.

Q2: Should a beginner investor add bond ETFs to their portfolio alongside VOO?

A2: Yes — for most investors, adding bond ETFs alongside VOO creates a more balanced, resilient portfolio. VOO gives you broad U.S. stock market growth, while BND or AGG provides stability, income, and a cushion during equity downturns. A classic starting allocation for a 30–40 year old might be 70–80% VOO and 20–30% BND, rebalanced annually. Younger investors (20s) may choose to keep bond exposure minimal and lean heavily into equity growth.

Q3: How do interest rates affect bond ETFs in 2026?

A3: Bond prices move inversely to interest rates. When rates rise, bond ETF prices fall — and vice versa. The Federal Reserve has held its benchmark rate steady at 3.5%–3.75% for three consecutive meetings as of June 2026, and markets expect rates to remain near this level through year-end. This rate stability is relatively favorable for bond ETF investors, as it reduces the risk of further price declines that occurred during the aggressive rate-hike cycle of 2022–2023. Short-duration bond ETFs like BND and SGOV are much less sensitive to rate movements than long-duration funds like TLT.

Financial Disclaimer: This article is for educational and informational purposes only and does not constitute financial, investment, tax, or legal advice. All yield figures, performance data, and projections referenced reflect current or historical information and are not a guarantee of future results. Bond ETF investments carry risks including interest rate risk, credit risk, and inflation risk, and you may receive back less than you invest. International investors should also consider the tax implications of foreign income distributions in their jurisdiction. Always conduct your own due diligence and consult a licensed financial advisor before making any investment decisions.