The market is in freefall. Your portfolio is flashing red. The news screams “worst drop since 2008.” Your finger hovers over the sell button — and every instinct you have is telling you to press it. This moment is the most dangerous in all of investing. Not because the crash is permanent. But because the decisions made during a crash determine whether you walk away with life-changing wealth — or lock in real, permanent losses. Knowing exactly what to do when the stock market crashes is the single most important skill a long-term ETF investor can develop. This guide gives you a clear, data-backed plan for staying calm, staying invested, and coming out stronger on the other side.

Key Takeaways:

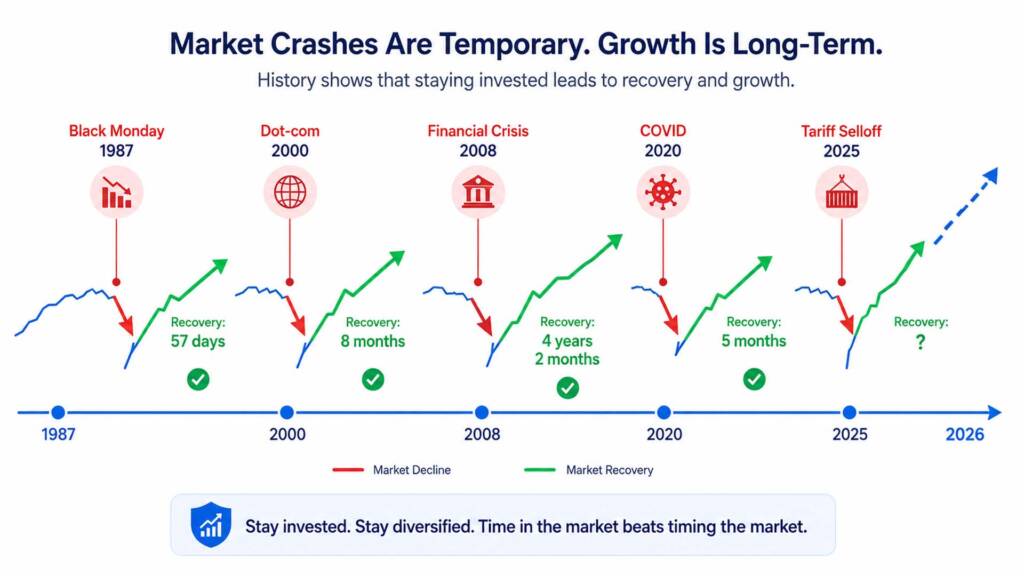

- Market crashes are temporary. The S&P 500 has recovered from every single crash in its 150-year history — including the April 2025 tariff-driven selloff that wiped out $5 trillion in two days, only to fully recover by May 2025.

- Panic selling is the #1 wealth destroyer. Missing just the 10 best trading days in a decade can cut your total returns by more than half — and those best days almost always occur within weeks of the worst days.

- Crashes are buying opportunities for disciplined ETF investors. Dollar-cost averaging into VOO during a downturn means you accumulate more shares at lower prices — shares that compound at full value when the market recovers.

Why Stock Market Crashes Are Normal (and Expected)

Before learning what to do when the stock market crashes, you need to truly internalize one fact: crashes are not anomalies. They are a built-in feature of equity markets.

Morningstar’s analysis of 150 years of market data confirms that major market crashes have occurred regularly throughout history. Invesco’s research shows the average time to recovery from a 5–10% downturn is just three months, and from a 10–20% correction, approximately eight months. Even severe bear markets — defined as a 20% or greater decline — have recovered within one to two years on average.

Consider the most recent examples. In April 2025, President Trump’s “Liberation Day” tariff announcement sent the S&P 500 into near bear market territory, wiping out $5 trillion in market cap in just two days — the largest two-day loss in S&P 500 history. The Nasdaq briefly entered bear market territory. Fear was extreme — the VIX (market fear gauge) spiked to 52, one of its highest readings ever recorded. Yet by early May 2025, the market had fully recovered after Trump paused the most severe tariffs. The S&P 500 finished 2025 up approximately 17% — the third consecutive year of double-digit gains.

What the Data Says About Recovery

Hartford Funds compiled data on the S&P 500’s 10 worst single-day drops between 1981 and 2025. The findings are remarkable:

| Crash Event | One-Day Drop | Days to Recover | 1-Year Return After |

|---|---|---|---|

| Black Monday (Oct 1987) | –20.47% | 264 days | +23.19% |

| COVID-19 Crash (Mar 9, 2020) | –7.60% | 57 days | +41.10% |

| Asian Financial Crisis (Oct 1997) | –6.87% | 8 days | +21.48% |

Source: Hartford Funds, S&P 500 Index 1981–2025

In all but one instance, the S&P 500 delivered double-digit positive returns within one year of its worst single-day drops. The message is unambiguous: the investors who held — and especially those who bought more — were richly rewarded. Those who sold locked in their losses permanently.

The Biggest Mistake: Panic Selling

This deserves its own section because it is so destructive — and so common. Panic selling is the single greatest wealth destroyer for retail investors, and it happens because human brains are wired to avoid pain, not maximize long-term gain.

When you sell during a crash, you do three devastating things simultaneously:

- You lock in temporary losses as permanent, realized losses

- You exit the market before the recovery begins — and the recovery almost always begins when conditions feel the worst

- You face the impossible task of deciding the “right time” to buy back in — which most investors never do, missing the rebound entirely

According to Yahoo Finance, 80% of Americans were at least slightly concerned about a recession in late 2025 — right before the S&P 500 recovered to finish the year up 17%. That fear, amplified by news headlines, was the single greatest threat to their long-term returns — not the market itself.

The antidote to panic is preparation. Investors who have a written plan for what to do when the market drops are measurably less likely to make reactive, emotion-driven decisions. That plan starts with understanding your portfolio’s structure. If you haven’t yet built a structured framework, our article on the Core and Satellite Portfolio Strategy provides exactly that blueprint.

7 Proven Steps: What to Do When the Stock Market Crashes

Here is your step-by-step action plan — grounded in data, designed for ETF investors.

Step 1 — Do Absolutely Nothing (First 48 Hours)

The most valuable action you can take immediately after a crash begins is inaction. Give yourself at least 48 hours before making any portfolio decision. Emotional decision-making in the first hours of a crash is responsible for some of the most costly investor mistakes in market history. Close the app. Step away from the screen. Remember: your time horizon is measured in decades, not days.

Step 2 — Review Your Written Investment Plan

Pull up your investment thesis and remind yourself why you own what you own. Ask yourself these three questions:

- Has the fundamental long-term case for VOO or your ETFs changed? (A tariff scare or earnings miss does not change the 30-year case for US equities.)

- Has your personal financial situation changed? (Job loss or an upcoming large expense may require a genuine reassessment — and that’s okay.)

- Is the decline driven by temporary sentiment or a structural, permanent economic shift? (Historically, nearly all crashes are the former.)

If the answers point to “nothing fundamental has changed,” your plan remains valid. Stay the course.

Step 3 — Accelerate Your Dollar-Cost Averaging

A market crash is not a red light for investing. It is a green light — specifically a flashing neon green light. When VOO drops 15–20%, you are buying the same 500 companies at a significant discount. The shares you accumulate during a downturn are the ones that will compound most powerfully when the market recovers to new highs.

In early 2026, VOO briefly traded around $529–$650 before recovering to $679+ by May 2026. Investors who accelerated their contributions during that period locked in shares at discount prices — shares that appreciated 15–28% within weeks. This is precisely the mechanism our article on Dollar-Cost Averaging Explained describes in detail. Consistency plus downturns equals compounding acceleration.

Step 4 — Rebalance Your Portfolio Strategically

Market crashes naturally distort your target asset allocation. If your core holding (VOO) drops 20% but your income satellite (JEPQ) drops only 8%, your portfolio is now underweight the asset that has the most recovery upside. Rebalancing — selling the relatively outperforming position and buying more of the underperforming one — forces you to buy low automatically.

This isn’t market timing. It is systematic discipline. Set a rebalancing trigger: if any position drifts more than 5–7 percentage points from its target weight, rebalance. Annual or semi-annual reviews capture most rebalancing opportunities without over-trading.

Step 5 — Consider Tax-Loss Harvesting (US Investors)

If you hold individual positions that are significantly down — say, a sector ETF satellite that dropped 25% — you may be able to sell at a loss to offset capital gains elsewhere in your portfolio. This is called tax-loss harvesting, and it is one of the few genuine silver linings of a market decline for taxable account holders.

The key rule: after selling for the loss, wait 31 days before repurchasing the same ETF to avoid the IRS wash-sale rule. During that 31-day window, you can hold a similar (but not identical) ETF to maintain market exposure. For example, selling VTI at a loss and temporarily holding SCHB maintains your equity position without triggering the wash-sale rule. Always consult a tax professional before executing this strategy.

Step 6 — Avoid Checking Your Portfolio Daily

Research consistently shows that investors who check their portfolios daily make significantly worse long-term decisions than those who check monthly or quarterly. During a crash, daily portfolio monitoring is the financial equivalent of checking the weather every five minutes during a storm. It amplifies anxiety without adding any useful information.

Set a calendar reminder for your next scheduled portfolio review (monthly or quarterly), and close the brokerage app. Your ETFs — particularly VOO — are managed by algorithms that automatically adjust holdings. You don’t need to manage them. You need to let them work.

Step 7 — Educate, Don’t Ruminate

Use the crash as a learning moment rather than a panic trigger. Read about how previous crashes unfolded and recovered. Review the historical data table from earlier in this article. Study your own behavioral responses — did you feel the urge to sell? When? That self-knowledge is invaluable for the next downturn. Understanding common behavioral traps is the focus of our guide on Beginner Investor Mistakes to Avoid, which covers the full spectrum of costly decisions new and intermediate investors make.

How ETFs Hold Up Better Than Individual Stocks During Crashes

This is one of the most compelling arguments for building your portfolio around broad-market ETFs. Individual stocks can go to zero — and many do during severe downturns. ETFs cannot go to zero unless every single company in the index simultaneously fails — which, in the case of the S&P 500, would mean the complete collapse of the American economy.

Consider what happened during the April 2025 tariff selloff. Some individual stocks — especially those in import-dependent sectors — dropped 40–60% and never fully recovered. Meanwhile, VOO dropped sharply but recovered entirely within weeks. The diversification built into a 500-company ETF is the most powerful crash defense available to a retail investor.

Additionally, broad-market ETFs like VOO automatically rebalance as companies grow and shrink. As weaker companies drop in market cap, their weight in the index decreases. As stronger companies grow, their weight increases. You never need to manage individual company risk — the index does it for you. For a deeper comparison of why individual stocks carry far more crash risk than diversified ETFs, see our article: Stocks vs. ETFs for Long-Term Wealth.

The Compounding Power of Buying During Crashes

Let’s make the opportunity real with a straightforward simulation. Suppose you invest $500/month into VOO consistently. Now compare two scenarios across a hypothetical 20-year period:

| Scenario | Strategy | Behavior During 3 Crashes | Projected 20-Year Outcome |

|---|---|---|---|

| Investor A | $500/month VOO | Stops contributions during each crash | ~$285,000 |

| Investor B | $500/month VOO | Doubles contributions to $1,000/month during each crash | ~$380,000+ |

| Investor C | $500/month VOO | Panic-sells during first crash, re-enters 6 months later | ~$210,000 |

Projections based on ~10.5% historical annualized total return for VOO. For illustrative purposes only. Past performance does not guarantee future results.

The difference between Investor B and Investor C — both of whom had the same monthly income and starting point — exceeds $170,000. That gap is created entirely by behavior during crashes, not by investment selection or intelligence. This is also why building even a small emergency fund outside your investment portfolio is critical — it ensures you never need to sell investments during a downturn due to a cash shortfall.

For a practical guide on building your portfolio around a consistent VOO position that weathers every storm, read: Investing $50 a Month in VOO — because the principles of consistent investing apply at every contribution level.

What to Do If the Crash Is Prolonged: Bear Market Playbook

Bear markets — defined as a 20% or greater decline from recent highs — are rarer but more emotionally grueling. Investopedia’s research shows bear markets typically last between nine and fifteen months on average. The longest in recent history — the dot-com crash of 2000–2002 — lasted approximately 2.5 years.

Here is your extended playbook if the downturn persists:

- Shift satellite contributions to your core. During a prolonged bear market, reduce satellite ETF contributions and increase VOO allocations. Core stability matters most in extended downturns.

- Add a bond or treasury ETF buffer. iShares’ IEF (7–10 Year Treasury Bond ETF) or BND can serve as a temporary safe-haven allocation — typically 10–15% — that holds value while equities decline.

- Review dividend income as a psychological anchor. During a bear market, your SCHD or JEPQ dividends keep arriving in your account every quarter. This tangible cash flow reinforces the reality that your investments are still working, even while prices are depressed. For a deeper look at this concept, explore our article on the Dividend Snowball Effect.

- Do not extend your time horizon backward. A 30-year investor who experiences a bear market 10 years in still has 20 years for compounding to work. The math remains overwhelmingly in your favor.

You can also find detailed guidance on navigating turbulent markets directly from BlackRock’s iShares team at their Turbulent Markets Strategy Center, and Investopedia offers an authoritative explainer on how long bear markets last with historical data across every major US market downturn.

Conclusion & Call to Action

The question of what to do when the stock market crashes has a simple, data-backed answer: stay calm, keep buying, and trust the structure you’ve already built. Every crash in S&P 500 history has been followed by a recovery. Every investor who stayed invested — and especially those who accelerated contributions during the downturn — was ultimately rewarded. The crash is not the threat. Your reaction to the crash is.

VOO returned 281% over the past decade despite multiple crashes, corrections, tariff scares, and geopolitical shocks along the way. That’s the return of investors who held. Not the ones who sold.

How did you handle the 2025 tariff selloff? Did you hold, buy more, or panic sell? Share your experience in the comments — your story might help another investor stay the course. And if you want to build the kind of structured, crash-resilient portfolio that makes these decisions easier, start with our complete guide: The Core and Satellite Portfolio Strategy.

Frequently Asked Questions

Q1: Should I sell my ETFs when the stock market crashes?

A1: In almost all cases, no. Selling your ETFs during a crash converts a temporary, paper loss into a permanent, realized loss. The S&P 500 has recovered from every major crash in its history — including the April 2025 tariff selloff that wiped $5 trillion in two days, recovering fully within weeks. The only legitimate reason to sell during a crash is if your personal financial situation has fundamentally changed — such as needing cash for an emergency expense. This is exactly why maintaining a 3–6 month emergency fund outside your investment portfolio is essential before you invest.

Q2: How long does it typically take for the stock market to recover after a crash?

A2: Recovery time varies by severity. According to Invesco’s research, the average recovery from a 5–10% downturn is approximately three months, and from a 10–20% correction, approximately eight months. Severe bear markets (20%+ declines) have historically recovered within one to two years on average, though the dot-com bust took about 2.5 years. Importantly, Hartford Funds’ data shows that the S&P 500 delivered double-digit positive returns in all but one instance within one year of its worst single-day crashes since 1981 — making staying invested the statistically dominant strategy.

Q3: Is it a good idea to buy more ETFs when the market crashes?

A3: Yes — for investors with a long time horizon, a crash is one of the best buying opportunities available. Buying VOO when it trades 15–20% below its recent high means you’re acquiring shares in America’s 500 largest companies at a discount. Those discounted shares compound at full value once the market recovers. The discipline of buying during downturns — through consistent dollar-cost averaging — is the mechanism that separates wealth-building investors from those who merely participate in the market. Just ensure you have an adequate emergency fund before investing additional capital, so you’re never forced to sell at the wrong time.

Financial Disclaimer: This article is intended for educational and informational purposes only. The strategies, data, historical examples, and compounding simulations presented here are based on publicly available market data and historical performance as of May 2026. Nothing in this article constitutes personalized financial advice, a recommendation to buy or sell any specific security, or a guarantee of future investment returns. All investing involves risk, including the possible loss of principal. Market recoveries referenced are historical and do not guarantee that future downturns will recover within similar timeframes. Always conduct your own due diligence and consult with a licensed financial advisor or registered investment professional before making any investment decisions.