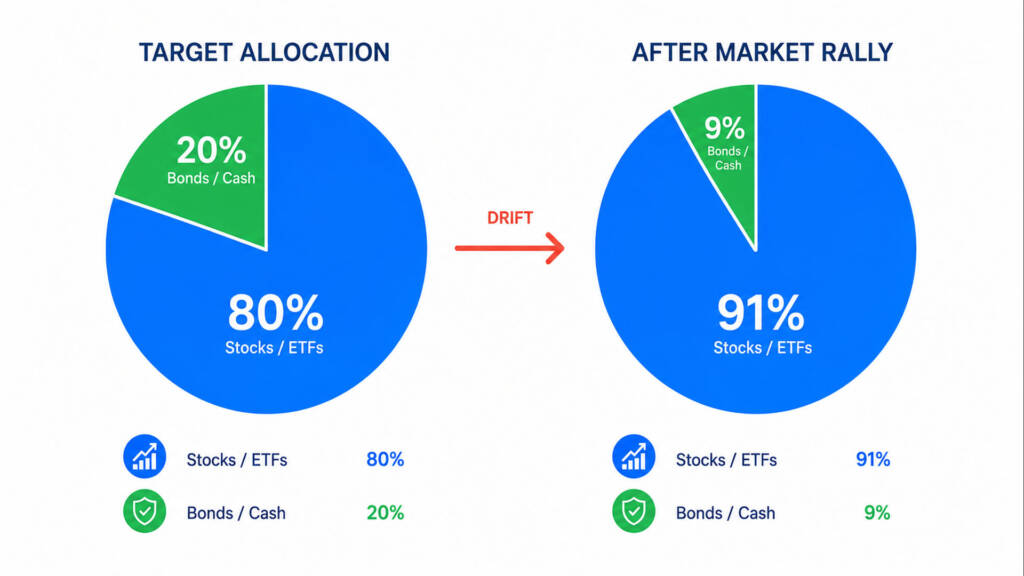

You built a solid portfolio — stocks, ETFs, maybe some bonds. Then the market moved. Your carefully planned 80/20 split is now sitting at 91/9, and you’re not sure what to do. Sound familiar? This is one of the most common — and most costly — problems passive investors face without a rebalancing plan. Drift in your asset allocation quietly changes your risk profile without you ever making a conscious decision. In 2026, with markets recovering from early-year volatility (the S&P 500 is up approximately +9.66% YTD through late May, after a choppy start), the question of how often to rebalance portfolio is more relevant than ever. The good news is that rebalancing doesn’t have to be complicated. With the right strategy, you can stay disciplined, cut risk, and protect your long-term wealth.

Key Takeaways:

- Annual or semi-annual rebalancing is optimal for most long-term ETF investors — frequent enough to control drift, infrequent enough to minimize costs

- A 5% threshold rule — rebalancing only when an asset class drifts 5 percentage points from its target — is one of the most cost-efficient approaches

- Rebalancing in tax-advantaged accounts (IRA, 401k) first avoids triggering unnecessary capital gains taxes in taxable accounts

What Is Portfolio Rebalancing (and Why Does It Matter)?

Portfolio rebalancing is the process of realigning the weights of your holdings back to your original target asset allocation. When one asset class grows faster than others, it takes up a larger share of your portfolio — and changes your actual risk exposure without you doing anything. For example, if you started 2024 with a classic 70% equities / 30% bonds split, the S&P 500’s total return of +25% in 2024 alone would have pushed your equity weight significantly above your target. Without rebalancing, you could be taking on far more risk than you initially intended.

This matters because your target allocation was built to reflect your risk tolerance and time horizon. Letting it drift means you could experience a much sharper drawdown in a downturn — like 2022’s -18.11% S&P 500 total return — than you were emotionally or financially prepared to handle. Therefore, rebalancing is not about chasing performance; it is about staying true to your long-term investment plan.

How Often Should You Rebalance Your Portfolio?

This is the core question — and fortunately, research gives us a clear framework. Vanguard’s own analysis concludes that annual rebalancing is optimal for most investors, noting that neither monthly/quarterly rebalancing nor waiting 2+ years represents the best approach. Fidelity outlines three practical approaches you can adopt today:

- Calendar-Based Rebalancing: Rebalance on a fixed schedule — typically once a year (most popular) or semi-annually

- Threshold-Based Rebalancing: Rebalance only when an asset drifts by a set percentage — commonly 5% — from its target weight

- Hybrid Rebalancing: Review your portfolio quarterly, but only rebalance if allocations have drifted beyond your 5% threshold

Most independent research — including analysis from White Coat Investor — reinforces that you should not rebalance more frequently than once a year, and that every 2–3 years is often perfectly fine for a diversified, long-term portfolio. The key insight from Elm Wealth’s 2026 analysis is sharp: “the difference in expected risk-adjusted return between any reasonable rebalancing frequency is negligible”. So don’t obsess over the perfect timing. Focus on having a plan and executing it consistently.

The 5% Threshold Rule Explained

The 5% threshold rule is arguably the most practical approach for DIY investors managing an ETF portfolio. It works like this: you set a trigger level — say, ±5 percentage points from your target weight. You only rebalance when an asset class crosses that boundary. For example, if your target for VOO (Vanguard S&P 500 ETF) is 70% of your portfolio and it grows to 76%, that triggers a rebalancing event. This method minimizes unnecessary trades and transaction costs while keeping your risk level disciplined.

Some advisors use a relative threshold of 20–25% instead of an absolute 5% — meaning if a 10% target position grows to 12.5% (a 25% relative increase), that’s the trigger. Either rule works well. The best one is simply the one you will actually follow.

Annual vs. Semi-Annual vs. Quarterly

Here is a practical comparison to help you choose your frequency:

| Frequency | Pros | Cons | Best For |

|---|---|---|---|

| Quarterly | Catches drift early | Higher transaction costs, over-trading | Active traders, volatile allocations |

| Semi-Annual | Good balance of control and cost | Slightly more work | Intermediate investors |

| Annual | Low cost, tax-efficient, research-backed | May miss significant drift | Most long-term ETF investors |

| Threshold-Only | Most cost-efficient, reactive | Requires regular monitoring | Disciplined investors with a specific drift limit |

| Hybrid (Annual + 5% Threshold) | Best of both worlds | Needs consistent review cadence | Most recommended approach |

Rebalancing Strategies for ETF Investors in 2026

If your portfolio is built around broad-market ETFs like VOO as a core holding — which we strongly recommend as the stable foundation of a long-term portfolio — rebalancing is straightforward. VOO returned +29.43% over the past 12 months through May 2026, meaning an equity-heavy portfolio has likely drifted significantly toward stocks. This is a powerful real-world trigger to review your allocation today.

Here are the four main rebalancing strategies ETF investors use, adapted from expert sources:

1. Calendar Rebalancing

Set a date — January 1st, your portfolio anniversary, or any fixed date — and review on that day each year. This is simple, low-effort, and research-backed. Most financial planners recommend this as the starting point for beginner investors.

2. Threshold (Drift) Rebalancing

As described above, this triggers a rebalance only when a position deviates beyond a predetermined band. This approach minimizes unnecessary trades and is especially tax-efficient, since you’re not forced to sell on a schedule regardless of market conditions.

3. Cash Flow Rebalancing

This is a brilliant, often-overlooked strategy for investors who are still in the accumulation phase. Instead of selling overweight assets, you direct new contributions toward your underweight assets. For instance, if your bonds allocation has shrunk below target, your next investment goes into bonds rather than equities. This eliminates transaction costs and potential tax events entirely. If you’re using dollar-cost averaging — contributing regularly to your portfolio — you can layer this strategy on top effortlessly.

4. Dividend-Directed Rebalancing

If you hold dividend ETFs like SCHD or VYM alongside your growth positions, you can use incoming dividends to purchase underweight assets rather than reinvesting them automatically. This is a tax-smart method that aligns well with a dividend snowball strategy. It also pairs naturally with a VOO and JEPQ portfolio, where JEPQ’s monthly income distributions can be redirected to rebalance into your core equity holding.

A Real-World Rebalancing Example

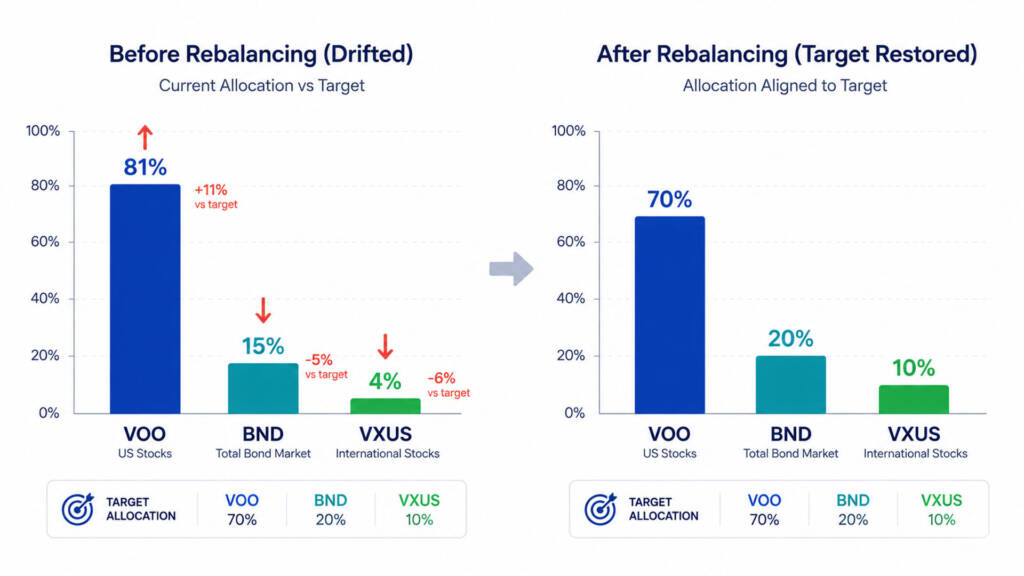

Let’s make this concrete with a simple simulation. Imagine you started 2023 with a $10,000 portfolio split as follows:

- VOO (S&P 500 ETF): $7,000 (70%)

- BND (Bond ETF): $2,000 (20%)

- VXUS (International ETF): $1,000 (10%)

Fast-forward to late 2025. After the S&P 500 returned +26.29% in 2023 and +25.02% in 2024, your VOO position would have grown substantially, while bonds lagged. Your allocation might now look more like:

- VOO: ~$11,800 (≈81% of portfolio)

- BND: ~$2,200 (≈15%)

- VXUS: ~$1,100 (≈4% — well below 10% target)

Your equity exposure has quietly jumped from 70% to over 80%. Your international exposure has been cut in half. Without rebalancing, you’re now a more aggressive investor than you planned to be — and you didn’t choose that. Selling a portion of VOO to bring it back to 70% and buying VXUS to return it to 10% restores your intentional risk profile. This single annual action keeps your portfolio doing exactly what you designed it to do.

Tax Considerations When Rebalancing

Taxes are the most common reason investors avoid rebalancing — and also one of the most misunderstood barriers. Here is what you actually need to know:

- Tax-advantaged accounts first: Always rebalance inside your IRA, Roth IRA, or 401(k) first. No capital gains taxes are triggered on sales inside these accounts, making them the most flexible rebalancing zone.

- In taxable accounts, use cash flows: Direct new contributions and dividends toward underweight assets to avoid selling appreciated positions and triggering a taxable event.

- Tax-loss harvesting: If some positions are at a loss in a down year (like 2022’s -18.11% S&P 500 return), you can sell those losers to offset gains from winners — reducing your tax bill while rebalancing.

- Long-term capital gains rates: If you do sell appreciated assets in a taxable account, holding positions for over 12 months qualifies you for the lower long-term capital gains tax rate (0%, 15%, or 20% depending on income), rather than the higher short-term rate.

One of the most common beginner investor mistakes is either never rebalancing at all, or panic-selling during a downturn to “rebalance” — which is actually market timing in disguise. Check out our guide on what to do when the stock market crashes to understand how to separate rebalancing decisions from emotional reactions.

How to Build Your Personal Rebalancing Plan

Follow these five steps to create a rebalancing system that actually sticks:

- Define your target allocation. Start with your risk tolerance and time horizon. A common starting point for long-term investors is 80% broad-market equities (e.g., VOO) and 20% bonds or alternatives. Review our core and satellite portfolio guide for a structured approach.

- Choose your rebalancing method. For most readers of this blog, the hybrid approach — annual calendar review + 5% drift threshold — is the optimal starting point. It’s easy, cost-efficient, and research-backed.

- Set a recurring calendar reminder. Put it in your phone now. January 1st, your birthday, a tax deadline — pick a memorable date and commit to it.

- Use new contributions to rebalance first. Before selling anything, redirect any fresh capital toward underweight positions. This is simple, free, and tax-neutral.

- Prioritize tax-advantaged accounts. Do your rebalancing trades inside your IRA or 401(k) first. Reserve taxable accounts for cash-flow rebalancing only.

For further reading on building a rock-solid ETF foundation, explore our piece on stocks vs. ETFs for long-term investing and the growth vs. dividend investing comparison to understand how your asset mix choice affects your rebalancing needs.

Also see: External Authority — Vanguard’s official guide to portfolio rebalancing for a research-backed institutional perspective.

Conclusion & Call to Action

Rebalancing your portfolio is not about perfectly timing the market or making constant adjustments. It’s about maintaining the intentional, disciplined strategy you committed to when you first started investing. Research from Vanguard, Fidelity, and independent analysts consistently points to the same answer: annual or semi-annual rebalancing, combined with a 5% drift threshold, delivers the best balance of risk control and cost efficiency for most long-term investors.

In 2026 — with VOO up nearly +9.66% YTD and the S&P 500 having returned over +25% in 2024 — now is an excellent time to open your brokerage account, review your allocations, and ask one simple question: “Does my portfolio still match my plan?”

Ready to take action? Leave a comment below telling us how you currently handle rebalancing — or if this is the first time you’ve thought about it. And if you’re still building your foundational portfolio, don’t miss our article on investing $50 a month in VOO to see how consistent contributions and disciplined rebalancing can compound into real wealth over time.

Frequently Asked Questions

Q1: Is it bad to rebalance your portfolio too often?

A1: Yes — rebalancing too frequently (e.g., monthly or weekly) can hurt your returns by increasing transaction costs, triggering unnecessary tax events, and causing you to sell winning positions prematurely. Research from Vanguard shows that monthly or even quarterly rebalancing offers no meaningful performance advantage over annual rebalancing. For most ETF investors, once a year is the sweet spot.

Q2: Should I rebalance my portfolio during a market crash?

A2: A market crash is actually a natural rebalancing opportunity — your equity positions may have dropped enough to bring them below your target weight, meaning you should be buying equities (specifically broad-market ETFs like VOO), not selling them. However, it’s critical to separate disciplined rebalancing from panic reactions. Use your pre-set threshold rules, not emotions, to guide any decision. For a full framework, read our guide on what to do when the stock market crashes.

Q3: Can I rebalance a portfolio without paying taxes?

A3: Yes — there are several tax-free or tax-minimizing rebalancing strategies. First, rebalance inside tax-advantaged accounts like a Roth IRA or 401(k), where no capital gains taxes apply. Second, use cash flow rebalancing — direct new contributions and dividend income toward underweight assets instead of selling overweight ones. Third, apply tax-loss harvesting in down years to offset any gains. With smart planning, many investors rebalance their portfolios annually without triggering a single taxable event.

Financial Disclaimer: This article is intended for educational and informational purposes only. It does not constitute financial, investment, tax, or legal advice. All historical returns mentioned are past performance and do not guarantee future results. Individual circumstances vary — always consult with a licensed financial advisor, tax professional, or investment manager before making any changes to your investment portfolio.