You’ve done your homework. You’ve discovered that VOO — the Vanguard S&P 500 ETF — is the gold standard for long-term investing. Now you’re ready to invest. But then you read the fine print: as a non-US investor, you could lose 30% of every dividend to the IRS — and potentially up to 40% of your portfolio to US estate tax if you pass away while holding it. That’s not a small footnote. That’s a wealth-destroying trap that millions of international investors unknowingly walk into every year. So in the VWRA vs. VOO debate, which ETF is actually the smarter choice for investors outside the United States? In 2026, the answer is clearer than ever — and this guide breaks it all down so you can invest with confidence.

Key Takeaways:

- VOO is unbeatable for US residents but carries two critical tax disadvantages for non-US investors: a 30% dividend withholding tax and potential US estate tax up to 40% on assets above $60,000

- VWRA (Vanguard FTSE All-World UCITS ETF, Ireland-domiciled) avoids both of those traps, paying only 15% dividend withholding tax at the fund level — and zero US estate tax risk — making it the superior choice for international investors

- Despite VOO’s slightly higher historical performance due to pure S&P 500 exposure, VWRA’s tax efficiency closes most of the gap for non-US investors in a long-term, accumulating strategy

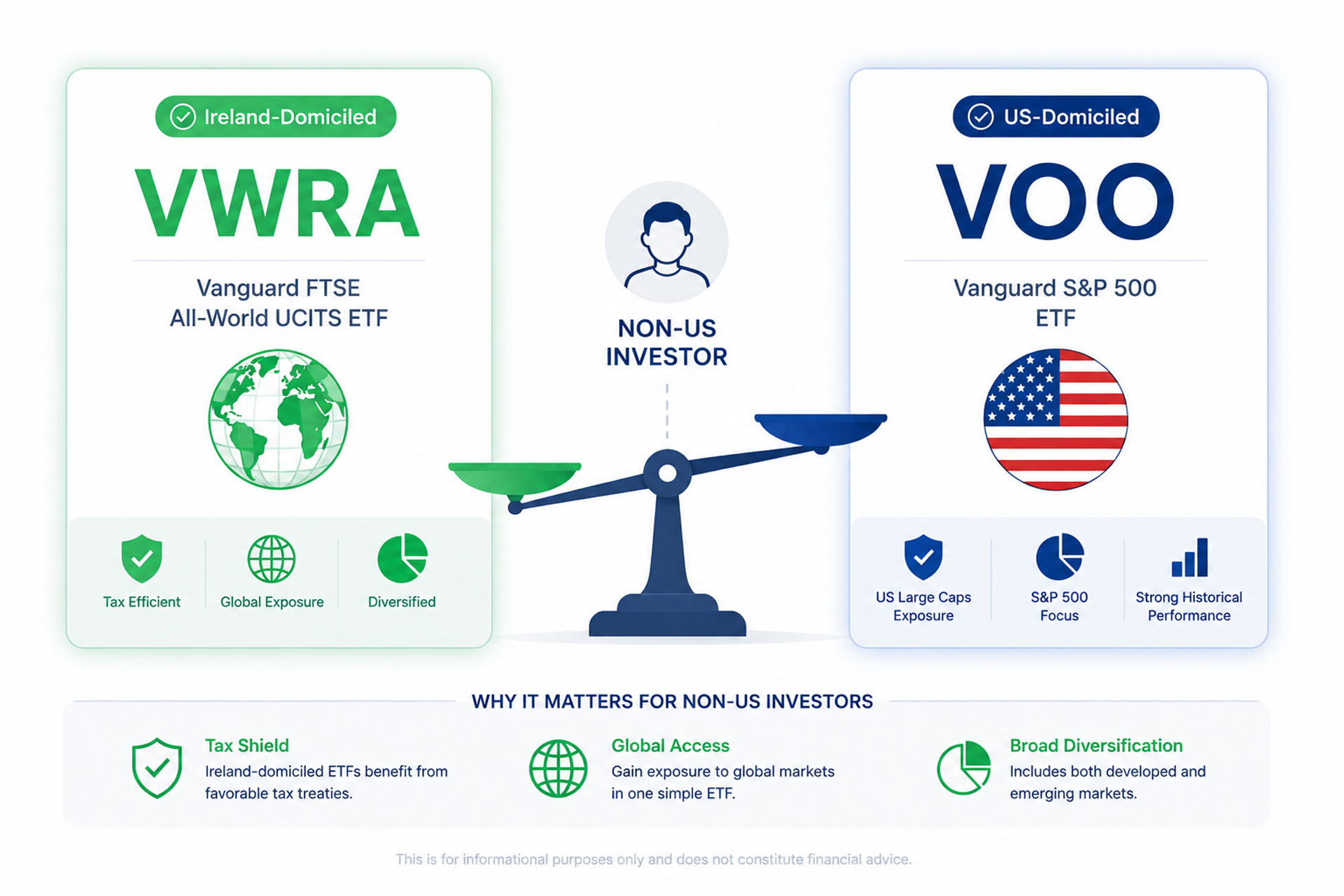

What Are VWRA and VOO?

Before diving into the comparison, let’s establish what each ETF actually is. Understanding their structure is key to understanding why one is better suited for international investors.

VOO — Vanguard S&P 500 ETF

VOO is a US-domiciled ETF managed by Vanguard and listed on the NYSE Arca. It tracks the S&P 500 Index, giving investors exposure to 500 of the largest publicly traded US companies. VOO has a razor-thin expense ratio of just 0.03% as of April 2026, and manages a staggering $927.8 billion in assets — making it one of the largest ETFs in the world. It is, without question, the benchmark for long-term US equity investing. However, its US domicile creates significant structural disadvantages for investors who reside outside the United States.

VWRA — Vanguard FTSE All-World UCITS ETF (Accumulating)

VWRA is an Ireland-domiciled, accumulating ETF listed on the London Stock Exchange (LSE). It tracks the FTSE All-World Index, which covers approximately 4,200 stocks across both developed and emerging markets worldwide — with US equities making up roughly 62–65% of the fund. VWRA carries an expense ratio of 0.22% and had an AUM of approximately $27.9 billion CHF as of early 2026. Because it is structured as a UCITS (Undertakings for Collective Investment in Transferable Securities) fund under Irish law, it benefits from the Ireland-US tax treaty and offers significant protection from US tax laws.

VWRA vs. VOO: The Critical Tax Comparison

This is where the debate gets real. For US investors, both ETFs are fine — but for international investors, the tax differences are massive. Let’s break them down one by one.

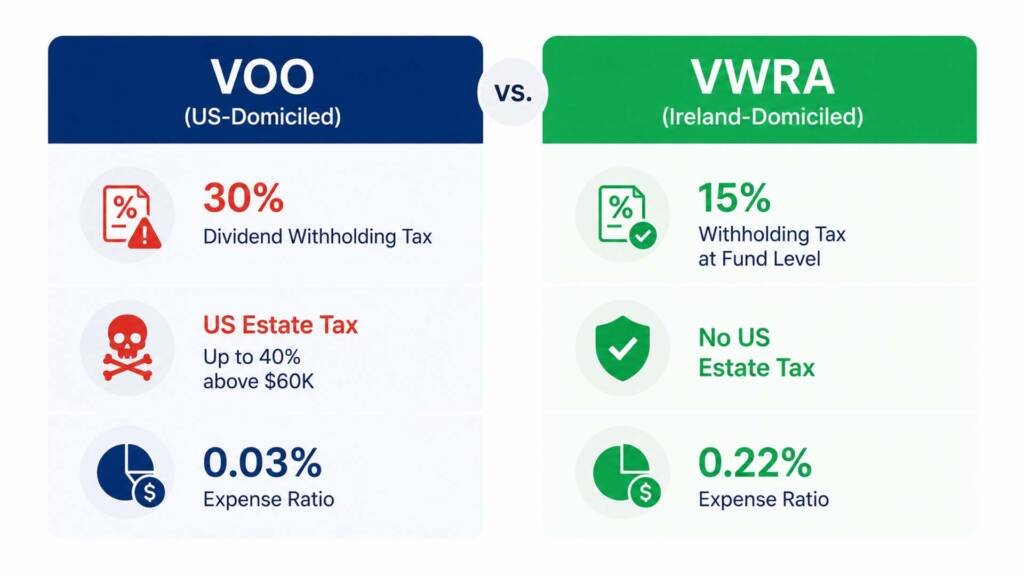

1. Dividend Withholding Tax

This is the single biggest financial difference between the two ETFs for non-US investors.

- VOO: When US companies inside VOO pay dividends, the IRS withholds a flat 30% tax before the money reaches a non-US investor. This is non-negotiable unless your country has a specific tax treaty with the US

- VWRA: Because VWRA is domiciled in Ireland, it benefits from the Ireland-US tax treaty, which reduces dividend withholding tax from 30% down to 15% at the fund level. Those dividends are then automatically reinvested inside the fund — so you as an investor never receive a taxable distribution

The math matters enormously here. If the S&P 500 yields approximately 1.3–1.5% in dividends annually, a 30% withholding rate on VOO costs a non-US investor roughly 0.39–0.45% per year in pure tax drag. With VWRA’s 15% rate paid inside the fund, that tax drag drops to approximately 0.20–0.23%. Over 20–30 years of compounding, that difference is substantial.

2. US Estate Tax — The Invisible Risk

This is the risk that almost no beginner international investor knows about — and it is potentially catastrophic.

- VOO (US-domiciled): If a non-US investor dies while holding VOO, the US government may levy an estate tax of up to 40% on the value of US-situated assets above $60,000. This $60,000 exemption is extremely low compared to the $13.61 million exemption available to US citizens. This means a non-US investor with as little as $60,001 in VOO could have their heirs face a tax bill of up to 40% of the excess amount.

- VWRA (Ireland-domiciled): Because VWRA is domiciled in Ireland — not the US — it is not classified as a US-situated asset. Therefore, non-US investors holding VWRA face zero US estate tax exposure, regardless of portfolio size

This single factor alone is a compelling reason for non-US investors to choose VWRA over VOO for any significant long-term accumulation.

3. Expense Ratio

Here, VOO wins decisively:

The gap is 0.19% annually. On a $50,000 portfolio, that’s roughly $95 per year more in fees with VWRA. However, when you factor in the tax advantages above — especially the 0.15–0.20% annual savings on dividend withholding tax alone — VWRA’s total cost for a non-US investor is often comparable or even lower than VOO on an after-tax basis.

VWRA vs. VOO: Side-by-Side Comparison

Performance: Does VWRA Keep Up With VOO?

This is the most common question — and the honest answer is: VOO has historically delivered higher raw returns because it focuses purely on the US market, which has outperformed global markets over the last decade. However, context matters enormously for non-US investors.

Historical Returns in Context

The S&P 500 delivered a remarkable +25.02% total return in 2024 and roughly +26.29% in 2023. VWRA, with its broader global diversification including emerging markets, generally underperforms the S&P 500 in strong US bull markets. However, VWRA’s 1-year return through late 2025 was approximately +18.63% — still an impressive figure for a globally diversified fund.

The key, however, is after-tax returns for non-US investors. Consider a $10,000 investment made in 2016:

- VOO (gross): With S&P 500 averaging approximately 12.6% annually over 10 years, $10,000 grows to approximately $32,900 before tax adjustments

- VOO (net for non-US): After applying ~0.39% annual dividend tax drag (30% on ~1.3% yield), real after-tax return drops modestly — but estate tax risk remains unresolved

- VWRA (net for non-US): With roughly 10–11% average annual growth and only ~0.20% annual dividend tax drag at the fund level, VWRA closes the gap significantly over time

For a non-US investor with a 20–30 year time horizon, the after-tax compounding math often favors VWRA — especially when the estate tax risk is factored into the equation.

Geographic Diversification as a Feature, Not a Bug

VWRA’s global exposure — covering Japan, the UK, Europe, India, and emerging markets alongside US equities — provides natural diversification that pure S&P 500 funds cannot offer. This is worth considering as US market concentration risk increases. If you’re interested in understanding how to balance a core ETF with satellite positions, our core and satellite portfolio guide shows exactly how to structure this approach.

Who Should Choose VWRA vs. VOO?

The decision ultimately comes down to one question: Where do you live and pay taxes?

Choose VOO If:

- You are a US citizen or permanent resident and pay US taxes

- You hold your investments inside a US tax-advantaged account (IRA, 401k, Roth IRA)

- You want maximum S&P 500 exposure at the lowest possible expense ratio

- You are already familiar with how to reinvest dividends manually

For US residents building a core position in VOO, our guide on investing $50 a month in VOO shows how consistent dollar-cost averaging can build serious wealth over time.

Choose VWRA If:

- You are a non-US investor residing in Asia, Europe, the Middle East, Africa, or Latin America

- You want to avoid the 30% US dividend withholding tax and the US estate tax risk entirely

- You prefer an accumulating ETF that automatically reinvests dividends — ideal for passive, set-and-forget investors

- You want built-in global diversification in a single fund, rather than managing multiple ETFs

- You invest through international brokers like IBKR, Saxo, or TD Direct and have access to LSE-listed instruments

How to Invest in VWRA as a Non-US Investor

VWRA trades on the London Stock Exchange under the ticker VWRA (USD-denominated) or VWRP (GBP-denominated). It is also available on Euronext Amsterdam and the Swiss Exchange (SIX). Most global brokers that service international investors — including Interactive Brokers (IBKR), Saxo Bank, and TD Direct Investing — provide access to LSE-listed UCITS ETFs.

Here’s a simple 3-step approach to building a VWRA-based core portfolio:

- Open an international brokerage account that supports UCITS ETFs (e.g., IBKR — available in most countries)

- Set VWRA as your core holding — target 80–90% of your equity allocation to VWRA for broad global diversification

- Apply dollar-cost averaging — invest a fixed amount monthly or quarterly, regardless of market conditions, to smooth out volatility over time

If you’re new to ETF investing and want to understand the fundamentals before committing capital, start with our beginner’s guide on what is ETF investing. It’s also worth reviewing the most common beginner investor mistakes before you place your first trade.

For authoritative external context on UCITS ETF structures and investor protections, see Vanguard’s official VWRA product page for full fund documentation and risk disclosures.

A Simple Compounding Simulation

Let’s make this tangible with a real-world example. Assume a non-US investor invests $500/month over 20 years in each ETF.

Assumptions:

- VOO gross annual return: ~10.5% (historical S&P 500 average, conservative estimate)

- VOO after-tax annual return for non-US investor: ~10.1% (after ~0.39% WHT drag on dividends)

- VWRA gross annual return: ~9.5% (global diversification, conservative estimate)

- VWRA after-tax annual return for non-US investor: ~9.3% (after ~0.20% WHT drag at fund level)

| VOO (After-Tax, Non-US) | VWRA (After-Tax, Non-US) | |

|---|---|---|

| Monthly Contribution | $500 | $500 |

| Projected 10-Year Value | ~$104,000 | ~$98,000 |

| Projected 20-Year Value | ~$397,000 | ~$365,000 |

| US Estate Tax Risk | Yes (up to 40% above $60K) | None |

| Effective 20-Year Wealth (after estate risk) | Uncertain — potentially reduced significantly | ~$365,000 fully protected |

These are projected outcomes based on historical averages — not guaranteed results. But the estate tax risk column changes everything. A $397,000 VOO portfolio held by a non-US investor at death could generate a US estate tax bill of approximately $134,800 (40% × [$397K − $60K]) — effectively erasing decades of compounding for your heirs.

Conclusion & Call to Action

The VWRA vs. VOO debate has a clear answer that depends entirely on your tax residency. For US investors, VOO remains the gold standard — the lowest-cost, most efficient S&P 500 tracker available. But for non-US investors, VWRA is the smarter long-term choice. It eliminates the 30% dividend withholding tax burden, removes US estate tax exposure entirely, and provides global diversification in a single, accumulating fund — all for a total cost that, after tax adjustments, is often comparable to VOO.

In 2026, with market access easier than ever and international brokers like IBKR serving investors across Asia, Europe, and beyond, there is no reason for non-US investors to accept the unnecessary tax drag of a US-domiciled ETF. Build your core position wisely — and let compounding do the work.

Found this comparison useful? Leave a comment below — especially if you’re investing from Southeast Asia, the Middle East, or Europe. Your experience could help other readers make a smarter choice. And if you want to go deeper, don’t miss our article on how often to rebalance your portfolio to keep your VWRA-based strategy on track over the long term.

Frequently Asked Questions

Q1: Is VWRA better than VOO for investors in Southeast Asia (e.g., Indonesia, Philippines, Singapore)?

A1: Yes — for most Southeast Asian investors, VWRA is the better choice. These countries generally do not have a tax treaty with the US that reduces the standard 30% dividend withholding tax. By holding VWRA instead, investors benefit from Ireland’s 15% WHT treaty rate (paid inside the fund), avoid US estate tax exposure entirely, and hold an accumulating fund that auto-reinvests dividends without manual action. This makes VWRA significantly more tax-efficient for long-term wealth building in this region.

Q2: Can I hold both VWRA and VOO in my portfolio?

A2: Technically yes — but it is generally not recommended for non-US investors. Holding VOO alongside VWRA reintroduces US dividend withholding tax at the full 30% rate and US estate tax exposure proportional to your VOO holdings. For non-US investors, a cleaner approach is to use VWRA as your primary core holding and add targeted satellite positions using other UCITS ETFs if needed. If you are a US investor, holding both creates unnecessary redundancy since VOO’s S&P 500 holdings are largely replicated within VWRA.

Q3: Does VWRA pay dividends?

A3: No — VWRA is an accumulating ETF, meaning it does not distribute dividends to investors. Instead, dividends received from underlying holdings are automatically reinvested back into the fund, increasing the NAV (net asset value) of each share you hold. This structure is ideal for long-term growth investors who want to maximize compounding without manually reinvesting distributions. This also means there is no dividend income to declare in most jurisdictions until you sell your shares — potentially simplifying your annual tax reporting significantly.

Financial Disclaimer: This article is intended for educational and informational purposes only. It does not constitute financial, investment, tax, or legal advice. Tax laws and withholding rates vary by country and individual circumstance. All historical returns and projected outcomes mentioned are based on past performance, which does not guarantee future results. Always consult with a licensed financial advisor, tax professional, or investment manager in your jurisdiction before making any investment decisions.