Most people think investing is only about buying stocks and hoping prices go up. But there is a second, often more powerful way to build wealth — and millions of investors are quietly using it right now. The problem is that many beginners never hear about it. They chase volatile growth stocks, stress over every market dip, and end up with an emotional rollercoaster instead of a wealth-building system. This approach leads to anxiety, poor decisions, and missed compounding opportunities. The solution is dividend growth investing — a proven strategy that builds rising passive income over time, rewards patience, and works whether the market goes up or down. This beginner’s guide breaks down exactly how dividend growth investing for beginners works, which ETFs to consider in 2026, and how to start today.

Key Takeaways:

- Dividend growth investing focuses on owning companies that consistently increase their dividend payments year after year — not just stocks with the highest yield today.

- Reinvesting dividends through a DRIP (Dividend Reinvestment Plan) creates a powerful compounding effect — one that has historically delivered 50% higher returns over 20 years compared to keeping dividends as cash.

- In 2026, dividend growth strategies are outperforming — SCHD has gained 27.1% in the past year while offering a 3.2% yield, proving that income and total return are not mutually exclusive.

What Is Dividend Growth Investing?

Dividend growth investing is a long-term wealth-building strategy. It focuses on buying shares in high-quality companies that regularly increase the amount they pay out to shareholders as dividends. Rather than chasing the highest yield today, a dividend growth investor prioritizes sustainability and consistent annual raises in income.

Think of it like a landlord who buys rental properties. The goal is not to flip houses for a quick profit. Instead, the investor collects monthly rent — and each year, that rent goes up. Over time, the income grows larger, the properties appreciate in value, and the investor builds real wealth without constant effort.

This strategy is especially powerful in 2026. As market volatility, sticky inflation, and economic uncertainty continue, dividend growth strategies are offering a compelling combination of stability, rising income, and competitive total returns. For a broader look at how this strategy compares to pure growth approaches, our article on growth vs. dividend investing is essential reading.

Key Terms Every Beginner Should Know

Before going further, let’s define the core vocabulary of dividend growth investing:

- Dividend: A cash payment a company distributes to shareholders, typically every quarter.

- Dividend Yield: The annual dividend payment divided by the stock’s current price. A $3 annual dividend on a $100 stock = a 3% yield.

- Dividend Growth Rate: The annual percentage by which a company raises its dividend. Higher is better.

- Payout Ratio: The percentage of earnings paid out as dividends. A lower ratio (under 60–70%) signals that dividends are sustainable.

- Yield on Cost (YOC): Your dividend income divided by what you originally paid — not the current price. This metric grows beautifully over time as dividends increase.

- DRIP: A Dividend Reinvestment Plan — automatically uses your dividends to buy more shares instead of paying you cash.

- Dividend Aristocrat: An S&P 500 company that has raised its dividend for at least 25 consecutive years.

Why Dividend Growth Investing Works: The Compounding Engine

The secret weapon of dividend growth investing is compounding. When you reinvest your dividends through a DRIP, your dividends buy more shares. More shares generate more dividends. Those dividends buy even more shares. Over years and decades, this creates an exponential snowball effect.

Schwab’s research illustrates this beautifully. Consider two investors, each owning 100 shares of a stock at $100 per share with a 4% annual dividend yield. One investor re-invests all dividends through a DRIP; the other keeps the cash. After 20 years, assuming a flat stock price and steady 4% yield, the DRIP investor’s portfolio grows to more than $22,000 — while the cash-keeper ends up with only $18,000. That is a 50% higher return from the same starting position.

Now, add in rising dividends and stock price appreciation — which both happen in a quality dividend growth portfolio — and the numbers become truly remarkable.

The Yield on Cost Magic

Here is where dividend growth investing becomes especially exciting for long-term holders. Consider SCHD, the Schwab U.S. Dividend Equity ETF. As of June 2026, SCHD offers a trailing dividend yield of approximately 3.2% with a 10-year average annual dividend growth rate of around 10.6%.

Using the Rule of 72, a dividend growing at 10% doubles every ~7 years. So if you buy SCHD today at a 3.2% yield:

| Year | Approximate Yield on Cost |

|---|---|

| Today (2026) | 3.2% |

| Year 7 (~2033) | ~6.4% |

| Year 14 (~2040) | ~12.8% |

| Year 21 (~2047) | ~25.6% |

This is an illustrative projection based on SCHD’s historical 10-year dividend growth rate of ~10.6%. Past growth rates do not guarantee future dividend increases.

This is why long-time SCHD investors now report earning over a 12.5% dividend yield on their original cost basis — their income effectively doubled multiple times while the market went up around them. That is the magic of buying quality and holding patiently.

The Dividend Aristocrats: Proof That Consistency Wins

Dividend Aristocrats are S&P 500 companies with at least 25 consecutive years of dividend increases. These are not lucky companies — they are businesses with durable competitive advantages, strong cash flows, and disciplined management teams.

Some 2026 examples of dividend aristocrats investors are watching closely include:

- Sysco (SYY) — The largest U.S. foodservice distributor, with 56 consecutive years of dividend increases and a current yield of ~3.0%.

- Dover Corp. (DOV) — A diversified industrial company that has raised its dividend for 35 consecutive years.

- Cincinnati Financial (CINF) — A property and life insurance specialist with 26 years of increases and a 2.32% yield.

- Genuine Parts Co. (GPC) — A global automotive and industrial parts distributor with 35 consecutive years of dividend growth.

These companies have navigated recessions, market crashes, inflation, and global crises — and still raised their dividends every single year. That kind of reliability is exactly what dividend growth investing for beginners is built upon. To understand how the dividend snowball builds over time using real stocks and ETFs, visit our deep dive on the dividend snowball effect.

The Best Dividend Growth ETFs for Beginners in 2026

If picking individual stocks feels daunting, dividend growth ETFs offer instant diversification across dozens or hundreds of dividend-growing companies. Here are the top options to consider in 2026:

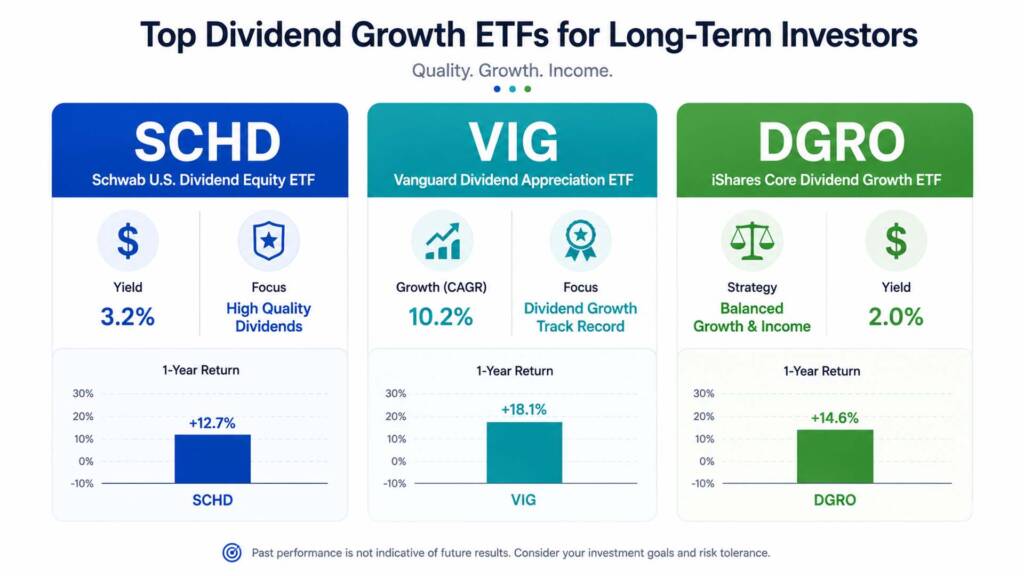

SCHD — Schwab U.S. Dividend Equity ETF

SCHD is arguably the most popular dividend growth ETF for U.S. investors. It tracks the Dow Jones U.S. Dividend 100 Index and holds 104 high-quality dividend-paying stocks. As of June 2026, key data includes:

- Dividend Yield: ~3.2%

- Expense Ratio: 0.06%

- 1-Year Total Return: 27.1%

- 10-Year Dividend Growth Rate: ~10.6%

- P/E Ratio: ~17x

SCHD’s 2026 portfolio is heavily weighted toward Energy (20%) and Consumer Staples (19%) following its annual rebalance, and its minimal Technology exposure (8%) has worked in its favor as high-valuation tech stocks face scrutiny. For a detailed review, check out our full SCHD ETF review for 2026.

VIG — Vanguard Dividend Appreciation ETF

VIG takes a growth-first approach to dividends. It tracks the S&P U.S. Dividend Growers Index and holds 347 stocks — requiring at least 10 consecutive years of dividend increases for inclusion.

- Dividend Yield: ~1.5%

- Expense Ratio: 0.04%

- 1-Year Total Return: 19.6%

- 5-Year CAGR (since inception): ~10.2%

- Dividend Growth Rate (5Y): ~5%

VIG’s lower yield reflects its focus on quality and growth consistency over current income. Its payout ratio of just 39% signals that its holdings have enormous headroom to keep raising dividends for years ahead. If you prioritize long-term dividend reliability over current income, VIG is a compelling choice.

DGRO — iShares Core Dividend Growth ETF

DGRO occupies the middle ground. It requires a minimum of 5 consecutive years of dividend growth and a payout ratio below 75%, making it more inclusive than VIG but more disciplined than a pure high-yield fund.

- Dividend Yield: ~2.0–2.04%

- Expense Ratio: 0.08%

- 1-Year Total Return: 22.07%

- Inception-to-Date Avg Annual Return: ~12.23%

- Dividend Growth Streak: 11 consecutive years

Quick Comparison: SCHD vs VIG vs DGRO

| Feature | SCHD | VIG | DGRO |

|---|---|---|---|

| Issuer | Schwab | Vanguard | iShares |

| Holdings | 104 | 347 | ~400+ |

| Expense Ratio | 0.06% | 0.04% | 0.08% |

| Dividend Yield | ~3.2% | ~1.5% | ~2.0% |

| 1-Year Total Return | 27.1% | 19.6% | 22.07% |

| Min Dividend Growth Req. | Quality screen | 10+ years | 5+ years |

| Best For | Higher current income | Long-term growth | Balanced approach |

For a deeper side-by-side analysis of SCHD and DGRO, our SCHD vs DGRO 2026 comparison walks through every metric in detail.

How to Start Dividend Growth Investing as a Beginner

Starting is simpler than most people think. Follow these steps to build your first dividend growth portfolio in 2026:

Step 1: Open a Brokerage AccountChoose a low-cost, reliable brokerage. Interactive Brokers is an excellent choice for both U.S. and international investors, offering fractional shares, low commissions, and automatic DRIP enrollment.

Step 2: Start With a Broad Core HoldingBefore adding dividend ETFs, anchor your portfolio with a broad-market ETF like VOO (S&P 500). This gives you stable, diversified large-cap exposure as a foundation. Our guide to building a VOO ETF core portfolio is an excellent starting point.

Step 3: Add a Dividend Growth ETFLayer in SCHD, VIG, or DGRO based on your income vs. growth preference. A common beginner allocation is 70% VOO + 30% SCHD, giving you both broad market growth and rising dividend income.

Step 4: Enable DRIPTurn on automatic dividend reinvestment for every holding. This is the single most impactful action a beginner can take. As Schwab’s research shows, reinvestment leads to 50% more wealth over 20 years — automatically, with zero extra effort.

Step 5: Contribute Consistently With Dollar-Cost AveragingInvest a fixed amount regularly — monthly or bi-weekly — regardless of market conditions. This strategy, known as dollar-cost averaging, removes emotion from investing and reduces the impact of market timing.

Step 6: Reinvest, Rebalance, RepeatCheck your portfolio annually. Rebalance if allocations drift significantly. Most importantly — do not panic-sell during downturns. Dividend-paying companies that have survived 25+ years of market cycles are designed for exactly these moments.

A Simple $300/Month Compounding Simulation

To make this concrete, let’s simulate investing $300 per month into a dividend growth ETF portfolio with a blended historical total return of approximately 10% per year (conservative blend of SCHD, VIG, and VOO):

| Timeframe | Estimated Portfolio Value | Estimated Annual Dividend Income* |

|---|---|---|

| 5 Years | ~$23,200 | ~$700 |

| 10 Years | ~$61,000 | ~$1,950 |

| 20 Years | ~$228,000 | ~$7,300 |

| 30 Years | ~$678,000 | ~$21,700 |

Dividend income estimates assume a blended 3.2% yield on the total portfolio value at each stage. These are illustrative projections based on historical data and do not guarantee future results.

The power of this approach lies not just in the final portfolio value — but in the fact that your annual income stream grows every single year, thanks to rising dividends and reinvestment. By year 30, a $300/month investment could be generating over $1,800 per month in dividend income alone.

Common Mistakes Beginners Make in Dividend Growth Investing

Even great strategies fail with poor execution. Here are the mistakes to avoid:

- Chasing the highest yield. A 10% yield may signal a struggling company about to cut its dividend — the dreaded “yield trap.” Always check the payout ratio and dividend history.

- Not reinvesting dividends. Taking dividend cash instead of enrolling in DRIP sacrifices the compounding engine that makes this strategy so powerful.

- Ignoring total return. Dividend growth investing is not just about income — the best dividend growth ETFs like VIG have generated a total return of 602% since inception in 2006.

- Over-concentrating in one sector. Spreading across consumer staples, healthcare, industrials, financials, and utilities reduces risk dramatically.

- Selling during market crashes. Dividend growth companies are specifically designed to maintain — and even raise — dividends during downturns. Selling destroys your compounding runway. Review our guide on what to do when the stock market crashes before markets get choppy.

For a comprehensive list of beginner pitfalls across all investing styles, our guide to common beginner investor mistakes is highly recommended.

Conclusion & Call to Action

Dividend growth investing for beginners is one of the most powerful and beginner-friendly wealth-building strategies available today. It rewards patience, eliminates the need to time the market, and builds a rising stream of passive income that can eventually cover your living expenses. In 2026, with dividend strategies like SCHD outperforming the broader market on a total return basis, there has rarely been a better time to start.

Whether you start with $50 or $500 a month, the principles are the same: buy quality, reinvest dividends, and stay consistent. The compounding engine does the heavy lifting for you — you just need to give it time.

Ready to take the next step? Open a brokerage account at Interactive Brokers to start investing in dividend growth ETFs with low costs and automatic DRIP. For further research, Investopedia’s dividend growth investing resource center and Vanguard’s official fund pages are excellent authoritative references.

Which dividend growth ETF are you most interested in — SCHD, VIG, or DGRO? Leave a comment below and share your portfolio plan. And if you’re ready to build a full passive income portfolio, check out our complete guide to building a dividend portfolio in 2026.

FAQs

Q1: How much money do I need to start dividend growth investing as a beginner?A1: You can start dividend growth investing with as little as $10–$50 using fractional shares through a brokerage like Interactive Brokers. There is no minimum threshold — what matters far more than your starting amount is the consistency of your contributions and reinvesting every dividend you earn. A $100/month disciplined investor who starts today will outperform a $10,000 lump-sum investor who stops contributing and cashes out dividends.

Q2: What is the difference between high-yield dividend investing and dividend growth investing?A2: High-yield dividend investing prioritizes the highest current income — often targeting ETFs or stocks with yields of 5–10% or more. Dividend growth investing, by contrast, prioritizes companies that consistently raise their dividend each year, even if the starting yield is modest (1.5–3.5%). Over time, dividend growth investing typically builds a higher “yield on cost” and generates superior total returns because the companies raising dividends tend to be fundamentally stronger businesses. The risk of pure high-yield strategies is “yield traps” — companies paying unsustainably high dividends that later cut or eliminate payments.

Q3: What are the best dividend growth ETFs for beginners in 2026?A3: For most beginners in 2026, the top three dividend growth ETFs to consider are SCHD (Schwab, 3.2% yield, 0.06% expense ratio, best for current income), VIG (Vanguard, 1.5% yield, 0.04% expense ratio, best for long-term quality), and DGRO (iShares, 2.0% yield, 0.08% expense ratio, best for a balanced approach). Most beginners benefit from pairing one of these with a broad-market core ETF like VOO for total market stability. For a head-to-head analysis, see our SCHD vs DGRO 2026 and passive income ETF portfolio guides.

Financial Disclaimer: This article is intended for educational and informational purposes only. It does not constitute financial, investment, tax, or legal advice. All data, returns, simulations, and projections referenced in this article are based on historical performance and publicly available information as of June 2026. Past performance does not guarantee future results. All investing involves risk, including the potential loss of principal. Individual financial situations, goals, and risk tolerances vary significantly. Always conduct thorough due diligence and consult a licensed financial advisor or investment professional before making any investment decisions.