Imagine waking up on a Tuesday morning — no alarm, no commute, no boss. You are 40 years old, financially free, and your investment portfolio quietly funds your life while you sleep. Sounds impossible? For millions of people pursuing FIRE strategy ETF investing, it is not just possible — it is a structured, repeatable plan. The problem is that most people spend 40+ years working toward a retirement they barely enjoy, trading their best years for a paycheck. The system is designed to keep you working until 65. But what if you could compress that timeline to 15 or 20 years — or even less? The FIRE movement (Financial Independence, Retire Early) combined with disciplined ETF investing gives you a proven mathematical path to exit the workforce decades ahead of schedule. This guide breaks down exactly how FIRE strategy ETF investing works in 2026, which ETFs to own, and the real numbers behind an early retirement plan.

Key Takeaways:

- FIRE is built on two rules: the Rule of 25 (save 25× your annual expenses) and the 4% Rule (withdraw 4% per year in retirement) — giving you a clear, calculable target.

- Your savings rate is the single most powerful lever in FIRE — a 50% savings rate gets you to financial independence in approximately 17 years, regardless of your income level.

- Low-cost, broad-market ETFs like VOO are the preferred investment vehicle for FIRE portfolios — offering diversification, near-zero fees, and historical returns averaging ~10% per year that compound powerfully over 15–25 years.

What Is the FIRE Movement?

FIRE stands for Financial Independence, Retire Early. It is a personal finance and lifestyle movement built on one core idea: by saving and investing aggressively early in life, you can accumulate enough wealth to live off your investment returns indefinitely — without ever working again.

The FIRE movement gained momentum through the personal finance community and books like Your Money or Your Life and the influential blog Mr. Money Mustache. Today, in 2026, it has become a mainstream financial philosophy with dedicated communities, calculators, and thousands of documented success stories — from teachers and software engineers to retail workers who retired in their 30s and 40s.

FIRE is not about deprivation forever. It is about front-loading sacrifice — living below your means for 10–20 years — so that you can live entirely on your terms for the next 40–50 years. The mathematical elegance is that the same behavior (saving aggressively) both grows your portfolio faster and reduces the portfolio size you need to retire, because you prove you can live on less.

The Four Main Types of FIRE

Not all FIRE paths look the same. Here are the four most common variations:

- Lean FIRE: Retiring on a minimal budget — typically under $40,000/year. Requires extreme savings and a simple lifestyle. Best for those who prioritize freedom over consumption.

- Fat FIRE: Retiring comfortably on $80,000–$150,000+ per year. Requires a larger portfolio but maintains a full lifestyle without compromise.

- Barista FIRE: Reaching partial financial independence, then working part-time (e.g., as a barista or freelancer) to cover day-to-day expenses while investments grow. The middle path.

- Coast FIRE: Saving enough early so that your portfolio will grow to your FIRE number by traditional retirement age — even without additional contributions. Then you only need to earn enough to cover living expenses.

The Two Mathematical Pillars of FIRE

FIRE rests on two foundational formulas. Together, they give you a precise savings target and a sustainable withdrawal strategy.

Pillar 1: The Rule of 25 (Your FIRE Number)

Your FIRE Number is the total portfolio value you need to retire. The Rule of 25 calculates it simply:

FIRE Number = Annual Expenses × 25

| Annual Expenses | FIRE Number |

|---|---|

| $30,000 (Lean FIRE) | $750,000 |

| $50,000 (Moderate) | $1,250,000 |

| $80,000 (Comfortable) | $2,000,000 |

| $120,000 (Fat FIRE) | $3,000,000 |

The Rule of 25 is the inverse of the 4% Rule. If you can safely withdraw 4% per year, you need 25 times your annual spending (1 ÷ 0.04 = 25). Use our free FIRE Calculator to calculate your personal FIRE number in minutes.

Pillar 2: The 4% Rule (Your Safe Withdrawal Rate)

The 4% Rule originates from the landmark Trinity Study (1998), which analyzed historical stock and bond portfolio data from 1926 to 1995. The study found that a portfolio of 50% stocks and 50% bonds survived 95% of 30-year retirement periods when the investor withdrew 4% of the initial balance annually, adjusted for inflation.

In 2026, Morningstar’s updated analysis suggests that 3.9% is the most conservative safe starting withdrawal rate for a traditional retiree, while flexible spenders may withdraw up to 5.7% depending on their specific portfolio and spending adaptability.

However, there is a critical caveat for early retirees: the original Trinity Study modeled 30-year retirements. If you retire at 35, you need your portfolio to last 50–60 years. Updated safe withdrawal rate research shows:

| Withdrawal Rate | 30-Year Success | 40-Year Success | 50-Year Success | 60-Year Success |

|---|---|---|---|---|

| 3.0% | 100% | 100% | 100% | 100% |

| 3.5% | 100% | 99% | 98% | 97% |

| 4.0% | 95% | 89% | 85% | 82% |

| 4.5% | 86% | 78% | 72% | 68% |

The takeaway: early retirees targeting a 50–60-year retirement should use a 3.25%–3.5% withdrawal rate to ensure near-certainty. This means saving 28–30× your annual expenses — a slightly higher bar, but one that dramatically improves your long-term security.

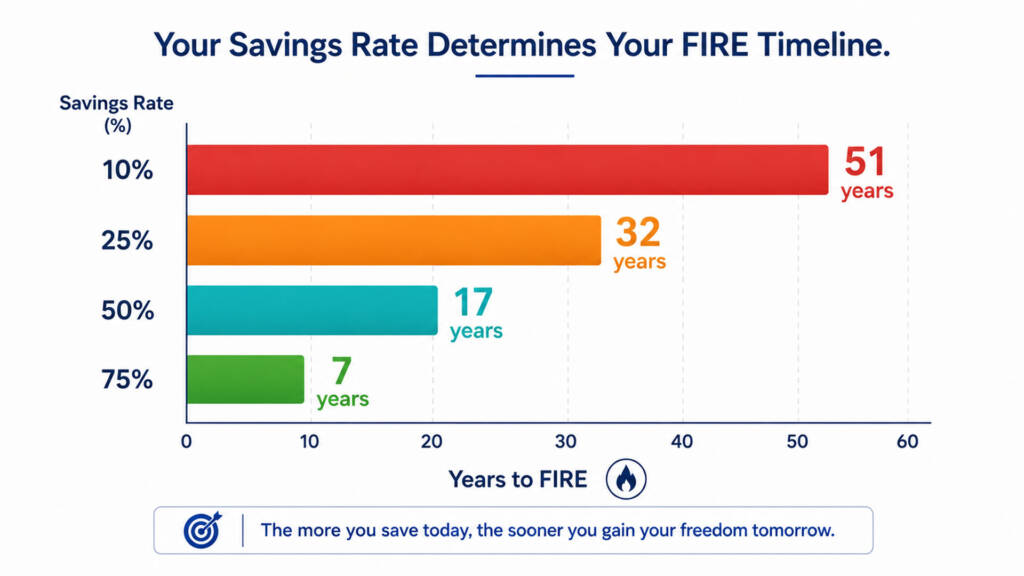

How Your Savings Rate Controls Everything

Your savings rate is the single most powerful variable in your FIRE timeline — more impactful than your income, investment returns, or any other factor.

Here is why it matters so much: a higher savings rate does two things simultaneously. First, it grows your portfolio faster because you invest more each month. Second, it proves you can live on less — which lowers your FIRE number. This double leverage is why even modest increases in savings rate dramatically compress your retirement timeline.

| Savings Rate | Years to FIRE (at 7% real return) |

|---|---|

| 10% | ~51 years |

| 25% | ~32 years |

| 50% | ~17 years |

| 75% | ~7 years |

T. Rowe Price’s research confirms: while a 15% savings rate is sufficient for retiring at 65, achieving FIRE requires a minimum 30% savings rate, with most aggressive FIRE pursuers targeting 50–70%.

The Best ETFs for a FIRE Portfolio in 2026

The FIRE community has converged on a clear consensus: low-cost, broad-market index ETFs are the optimal vehicle for building and sustaining a FIRE portfolio. The reasons are straightforward — minimal fees, maximum diversification, tax efficiency, and historically reliable long-term returns. Here are the core ETF building blocks:

VOO — Vanguard S&P 500 ETF (The FIRE Foundation)

VOO is the cornerstone of the vast majority of FIRE portfolios. It tracks the S&P 500’s 500 largest U.S. companies, charges just 0.03% in fees, and has delivered historical average annual returns of approximately 10.5–11% over the long term. In 2026, VOO trades near $676–$678 with a YTD return of approximately 5–6%.

VOO’s simplicity is its greatest strength. You get instant exposure to companies like Apple, NVIDIA, Microsoft, Amazon, and Meta — the engines of the U.S. economy — in a single, set-it-and-forget-it holding. Our complete VOO ETF core portfolio guide explains exactly how to build your entire FIRE foundation around this one ETF.

VTI — Vanguard Total Stock Market ETF

VTI extends beyond the S&P 500 to capture the entire U.S. stock market — over 3,500 companies including mid-cap and small-cap stocks. It carries the same 0.03% expense ratio as VOO and has a 99%+ correlation with it, making the two nearly interchangeable as a FIRE foundation. VTI’s broader coverage gives exposure to the “next generation” of potential large-cap leaders — an advantage in long 20–40-year FIRE accumulation horizons.

SCHD — Schwab U.S. Dividend Equity ETF (The Retirement Income Layer)

SCHD plays a different but critical role in a FIRE portfolio — particularly during retirement. With a current yield of approximately 3.2% and a 10-year dividend growth rate of ~10.6%, SCHD generates rising monthly income without forcing you to sell shares. As you transition from accumulation (building wealth) to distribution (living off your portfolio), SCHD’s growing dividend stream can cover a meaningful portion of your living expenses. For a detailed overview, see our SCHD ETF review for 2026.

BND — Vanguard Total Bond Market ETF (The Stability Buffer)

BND provides bond exposure to cushion against sequence of returns risk — one of the most dangerous threats to early retirees. A standard FIRE portfolio shifts toward a higher bond allocation (20–30%) as you approach and enter retirement, helping to stabilize withdrawals during equity market downturns.

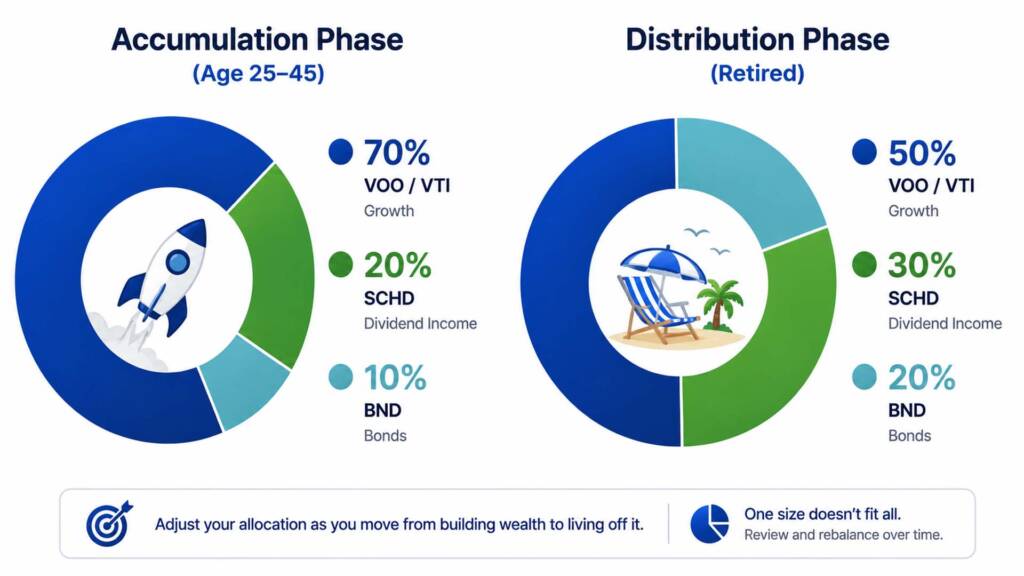

Building Your FIRE ETF Portfolio: Two Phases

A FIRE ETF portfolio operates in two distinct phases: accumulation and distribution. Each requires a different emphasis.

Phase 1: Accumulation (Building Your FIRE Number)

During accumulation — the years before reaching your FIRE number — your goal is maximum growth with controlled risk. A typical allocation for a FIRE investor in their 20s–40s might look like this:

- 70% VOO or VTI — Core growth engine, full U.S. equity exposure

- 20% SCHD — Dividend growth layer, reinvest dividends during accumulation

- 10% BND — Stability buffer, reduces volatility without crushing returns

The key strategy during accumulation is dollar-cost averaging — investing a fixed amount every month regardless of market conditions. This eliminates the need to time the market and ensures you buy more shares when prices fall.

Phase 2: Distribution (Living Off Your Portfolio)

Once you reach your FIRE number, you transition to distribution — living off your portfolio without depleting it. A common allocation shift looks like this:

- 50% VOO/VTI — Continued equity growth to stay ahead of inflation

- 30% SCHD — Rising dividend income stream to minimize shares sold

- 20% BND — Cash/bond buffer (1–2 years of expenses in stable assets)

The bond buffer is specifically designed to combat sequence of returns risk — the danger that a severe market crash in your first years of retirement permanently impairs your portfolio before it can recover. By keeping 1–2 years of expenses in cash or bonds, you avoid selling equity ETFs during deep drawdowns.

Our 3-ETF portfolio strategy guide walks through this exact structure with practical allocation percentages for every life stage.

A Real FIRE Compounding Simulation

Let’s run two concrete scenarios using a $2,000/month investment into VOO at a historical average return of approximately 10% per year:

Scenario A: 25-Year-Old Starting Today

| Year | Age | Monthly Investment | Estimated Portfolio Value |

|---|---|---|---|

| Year 5 | 30 | $2,000 | ~$154,000 |

| Year 10 | 35 | $2,000 | ~$413,000 |

| Year 15 | 40 | $2,000 | ~$833,000 |

| Year 20 | 45 | $2,000 | ~$1,530,000 |

| Year 25 | 50 | $2,000 | ~$2,650,000 |

At $2,650,000 and annual expenses of $80,000, this investor hits a Fat FIRE number at age 50 — 15 years before traditional retirement.

Scenario B: Reaching Lean FIRE Faster ($50,000 Annual Expenses)

| Target | FIRE Number | Monthly Savings Needed | Est. Years to FIRE |

|---|---|---|---|

| Lean FIRE ($30K/yr) | $750,000 | $1,000/mo | ~18 years |

| Moderate FIRE ($50K/yr) | $1,250,000 | $1,500/mo | ~20 years |

| Comfortable FIRE ($80K/yr) | $2,000,000 | $2,500/mo | ~22 years |

These are illustrative projections based on a 10% historical annual return on a VOO-anchored portfolio. Actual results will vary. These do not account for inflation, taxes, or varying market returns.

The power of these numbers is undeniable: even at a modest $1,000/month — less than $33/day — a consistent investor can reach Lean FIRE in under two decades. For inspiration on starting small, our guide on investing just $50 a month in VOO proves that every dollar invested early makes a disproportionate difference.

Managing Sequence of Returns Risk in Early Retirement

Sequence of returns risk (SORR) is the single greatest threat to FIRE portfolios. It occurs when a major market crash hits in the first few years of retirement — forcing you to sell depreciated shares to fund living expenses, permanently impairing your portfolio’s recovery capacity.

The 2000–2002 dot-com crash and 2008–2009 financial crisis both demonstrated how devastating early retirement crashes can be. Here are the proven strategies FIRE practitioners use to mitigate this risk:

- The Cash/Bond Bucket: Keep 1–2 years of living expenses in cash or BND so you never sell equities during a down market.

- Flexible Spending: Reduce discretionary spending by 10–15% during severe downturns, protecting your portfolio without panic selling.

- Conservative Withdrawal Rate: Use 3.25%–3.5% instead of 4% if your retirement spans 50+ years.

- Part-Time Income (Barista FIRE): Even $10,000–$15,000/year in part-time income dramatically reduces portfolio withdrawal pressure in the critical early years.

- Dividend Income: SCHD’s growing dividend stream covers part of your expenses without requiring you to sell shares — a built-in SORR buffer.

When markets do crash, the right response is almost never to sell. Our guide on what to do when the stock market crashes gives you a step-by-step playbook for staying calm and making smart decisions during market downturns.

Step-by-Step: How to Start Your FIRE Journey in 2026

Ready to begin? Here is your action plan, starting today:

- Calculate your FIRE Number. Multiply your current annual expenses by 25 (for 4% withdrawal) or 28.5× (for 3.5% withdrawal). Use our FIRE Calculator for a personalized projection.

- Maximize your savings rate. Identify your current rate. Push aggressively toward 30–50%+. Every 5% increase shaves years off your timeline.

- Open a tax-advantaged account. Max out your 401(k) contribution ($23,500 in 2026) and Roth IRA contribution ($7,000 in 2026) first. Tax-free or tax-deferred growth compounds massively over 20+ years.

- Build your FIRE ETF core. Start with VOO or VTI as your primary holding. Add SCHD for income and BND for stability as your portfolio grows.

- Enable automatic investing. Automate monthly contributions so you never skip a payment. Consistency beats timing every time.

- Reinvest all dividends. During accumulation, always reinvest. The dividend snowball effect compounds your wealth exponentially over time.

- Rebalance annually. Review your allocations once per year. Our guide on how often to rebalance your portfolio shows you exactly when and how to do this efficiently.

- Start today. Every month you delay is disproportionately expensive. A 25-year-old who starts immediately has mathematically proven advantages over a 30-year-old — not because of income, but because of compounding time.

Open your brokerage account at Interactive Brokers — one of the most cost-effective platforms for both U.S. and international investors — to start building your FIRE portfolio with low commissions and full access to VOO, VTI, SCHD, and BND. For further research, Investopedia’s comprehensive FIRE guide and Vanguard’s official fund resources are authoritative starting points.

Conclusion & Call to Action

FIRE strategy ETF investing is not a get-rich-quick scheme. It is a disciplined, mathematically proven framework that combines aggressive saving with the compounding power of low-cost index ETFs. In 2026, with tools like VOO, VTI, and SCHD available at near-zero cost, early retirement is more accessible than ever — for Americans and international investors alike.

The path is clear: calculate your FIRE number, increase your savings rate, invest consistently in broad-market ETFs, manage sequence of returns risk with smart allocation, and stay the course through market volatility. The math does not lie.

Where are you on your FIRE journey? Leave a comment below — whether you are just starting, actively pursuing FIRE, or already financially independent. And if you want to dive deeper into building the right ETF portfolio for your FIRE goals, start with our passive income ETF portfolio guide and our 3-ETF portfolio strategy for step-by-step allocation blueprints.

FAQs

Q1: How much money do I need to retire early using the FIRE strategy with ETFs?A1: Your FIRE number depends entirely on your annual expenses, not your income. Using the Rule of 25, multiply your annual expenses by 25. For example: $40,000/year in expenses requires a $1,000,000 FIRE portfolio; $60,000/year requires $1,500,000; $80,000/year requires $2,000,000. If you plan to retire before age 45 and need your portfolio to last 50+ years, use a more conservative 3.5% withdrawal rate — meaning you need approximately 28.5× your annual expenses for greater safety. Use our FIRE Calculator to get your exact personalized number based on your current savings, monthly contributions, and expected return assumptions.

Q2: Is VOO or VTI better for a FIRE ETF portfolio?A2: Both VOO and VTI are excellent FIRE portfolio anchors, and the difference in long-term outcomes is minimal. VOO tracks the S&P 500 (~504 large-cap stocks, 0.03% fee) and is slightly more concentrated in proven mega-cap companies. VTI covers the entire U.S. stock market (~3,500+ stocks, 0.03% fee) and adds mid- and small-cap exposure that can outperform over longer horizons. For a 20–30-year FIRE accumulation horizon, many investors prefer VTI for its broader coverage — but either choice is sound. The most important factor is not which one you choose, but that you start investing consistently and stay invested through every market cycle. Our detailed VTI vs VOO comparison covers every nuance to help you decide.

Q3: What is the biggest risk of retiring early with the FIRE strategy, and how do I protect against it?A3: The biggest risk is sequence of returns risk (SORR) — the danger of a major market crash occurring in the first 5–10 years of retirement, forcing you to sell depreciated ETF shares for living expenses. This early depletion permanently impairs your portfolio’s recovery even if markets bounce back. The proven mitigation strategies are: (1) maintaining a 1–2 year cash/bond buffer (BND) so you never sell equities during drawdowns; (2) using a conservative 3.25%–3.5% withdrawal rate for 50+ year retirements; (3) holding SCHD for dividend income that covers expenses without requiring you to sell shares; and (4) maintaining flexible spending habits to reduce withdrawals by 10–15% during severe downturns. For a broader strategy on staying disciplined when markets turn volatile, our guide on what to do when the stock market crashes is essential reading.

Financial Disclaimer: This article is intended for educational and informational purposes only. It does not constitute financial, investment, tax, or legal advice. All data, projections, compounding simulations, withdrawal rate analyses, and savings rate calculations referenced herein are based on historical data, publicly available research, and illustrative models as of June 2026. The 4% Rule, Rule of 25, and associated FIRE calculations are planning heuristics — not guarantees of any outcome. Past investment performance does not guarantee future results. All investing involves risk, including the potential loss of principal. Individual financial situations, income levels, tax obligations, expense structures, and risk tolerances vary significantly. Early retirement planning is complex and highly personalized. Always consult a licensed financial advisor, certified financial planner (CFP), and qualified tax professional before making any major investment or retirement decisions.