Most investors overcomplicate everything. They scroll through hundreds of ETFs, chase trending sectors, obsess over quarterly earnings — and end up with a bloated, overlapping portfolio that costs more and performs worse than a simple three-fund setup. Meanwhile, the “boring” investors who built a 3 ETF portfolio strategy back in 2015 quietly watched their wealth multiply — without a single sleepless night over individual stock picks. The truth is that complexity is the enemy of long-term investing success. In 2026, with the S&P 500 up approximately +9.66% YTD through late May and global markets recovering from earlier-year volatility, the case for a clean, diversified, low-cost three-fund approach has never been stronger. This guide gives you everything you need to build it — and actually stick with it.

Key Takeaways:

- The 3 ETF portfolio strategy — typically combining a US equity ETF, an international equity ETF, and a bond ETF — gives individual investors broad global diversification, low cost, and maximum simplicity in a single, manageable structure

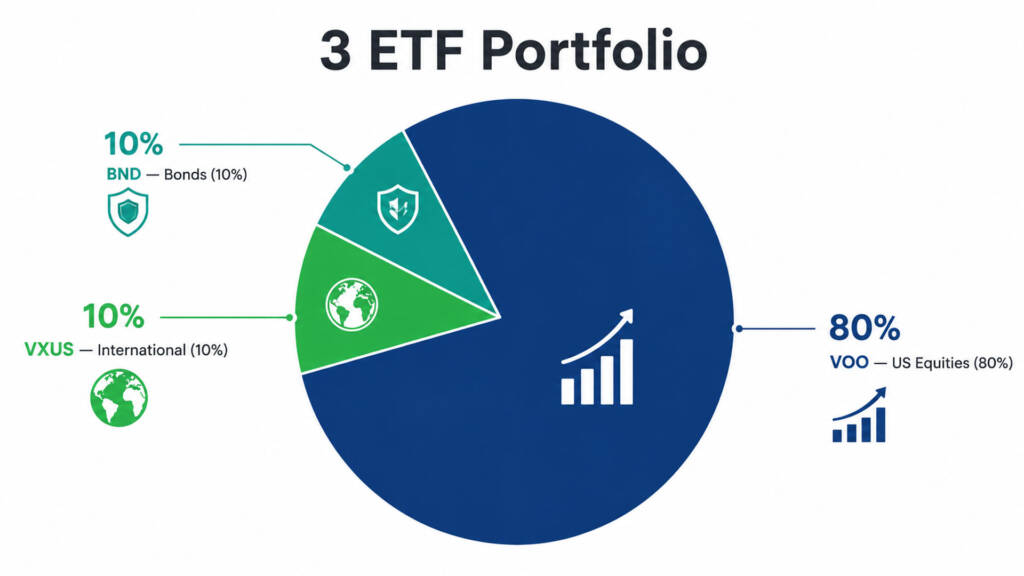

- VOO (S&P 500) anchors the portfolio as the core US equity holding, offering a 0.03% expense ratio and a long-term historical average return of approximately 10–12% annually — making it the essential foundation for any long-term passive investor

- A simple 80/10/10 or 70/20/10 allocation (US equities / international equities / bonds) is the most commonly recommended starting point for investors in the accumulation phase — adjustable based on age, risk tolerance, and timeline

What Is the 3 ETF Portfolio Strategy?

The 3 ETF portfolio strategy — also widely known as the “three-fund portfolio” or “Boglehead portfolio” — is a passive investing approach that uses just three low-cost index ETFs to achieve complete global diversification. The concept was popularized by the late John C. Bogle, founder of Vanguard, who championed the idea that most individual investors are better served by owning the entire market at minimal cost rather than trying to beat it.

The structure is elegantly simple. You hold:

- A US total market or S&P 500 ETF — for core domestic equity exposure

- An international equity ETF — for global diversification outside the US

- A bond ETF — for portfolio stabilization and downside protection

That’s it. Three funds. One strategy. Decades of compounding. The beauty of this approach is that it covers virtually every major asset class available to a retail investor — approximately 10,000+ individual stocks and bonds across the global economy — in a portfolio that takes less than 30 minutes per year to manage.

Why the 3 ETF Portfolio Works

Before building the portfolio, it’s worth understanding why this strategy has stood the test of time. The logic is grounded in three core investing principles.

1. Diversification Reduces Risk Without Sacrificing Return

By spreading your investment across US equities, global equities, and bonds, you reduce the risk that any single market, sector, or country downturn devastates your portfolio. When US tech stocks sold off sharply in early 2022, international and bond allocations cushioned the blow for three-fund investors. When bonds struggled in 2022 due to rising interest rates, US equities in the same portfolio had already delivered strong multi-year gains. No single holding ever sinks a well-diversified portfolio.

2. Low Fees Compound Into Real Wealth

The total weighted expense ratio of a typical 3-ETF portfolio — using VOO (0.03%), VXUS (0.07%), and BND (0.03%) — comes to approximately 0.03–0.05% annually. Compare that to the average actively managed mutual fund fee of 0.50–1.00% or higher. On a $100,000 portfolio over 30 years, that fee difference compounds into tens of thousands of dollars in additional wealth. Fees are the only guaranteed return you can control — and the 3-ETF portfolio minimizes them to nearly zero.

3. Simplicity Prevents Behavioral Mistakes

Most investment mistakes stem from emotional reactions — panic-selling during downturns, chasing hot sectors, over-trading. A three-fund portfolio eliminates most of those temptations. There is nothing to “watch” beyond your total allocation. There are no individual stock earnings reports to track. There are no sector rotations to time. You simply invest regularly, rebalance annually, and let the market do its work. This is exactly why avoiding common beginner investor mistakes starts with structural simplicity — and the 3-ETF portfolio is the simplest effective structure available.

The 3 ETFs: Our Recommended Building Blocks

There are multiple ways to build a three-fund portfolio, but for US investors and international investors targeting US market exposure, the following three ETFs represent the strongest 2026 combination:

ETF #1 — VOO: Vanguard S&P 500 ETF (Core US Equity)

VOO is the undisputed anchor of this portfolio. It tracks the S&P 500 Index, covers the 500 largest US companies, and delivers exposure to industries from technology and healthcare to financials and consumer goods. As of June 2026, VOO trades with a 0.03% expense ratio, manages approximately $1.5 trillion in AUM, and carries Morningstar’s top Gold Medalist Rating — the highest achievable. Its historical average annual return of approximately 10–12% makes it the single most powerful wealth-building instrument available to passive investors.

Recommended allocation: 60–80% of your total portfolio. VOO is the engine. Everything else plays a supporting role. If you’re still building your understanding of why VOO deserves this anchor position, our detailed guide on VOO as a core portfolio holding explains the full thesis.

ETF #2 — VXUS: Vanguard Total International Stock ETF (Global Diversification)

VXUS tracks the FTSE Global All Cap ex US Index, giving investors exposure to over 8,500 stocks across developed and emerging markets — Europe, Asia Pacific, Latin America, the Middle East, and more. With an expense ratio of just 0.07%, it is one of the most cost-efficient ways to diversify beyond US borders. As of mid-2026, international markets — particularly in Europe and parts of Asia — are showing competitive valuations compared to the historically stretched US market. Holding VXUS ensures you participate in global economic growth, not just American economic growth.

Recommended allocation: 10–20% of your total portfolio. This position provides geographic insurance. When US equities underperform for a stretch — as they did relative to international markets in 2002–2012 — your VXUS allocation keeps your portfolio growing.

Note for non-US investors: If you reside outside the United States, VXUS creates US estate tax exposure. Consider using VWRA (Vanguard FTSE All-World UCITS ETF) as a combined VOO + VXUS equivalent. Our VWRA vs. VOO comparison explains this in full detail.

ETF #3 — BND: Vanguard Total Bond Market ETF (Portfolio Stability)

BND tracks the Bloomberg U.S. Aggregate Float Adjusted Bond Index — covering US government bonds, corporate bonds, and mortgage-backed securities across all maturities. As of June 2026, BND carries an expense ratio of 0.03% and yields approximately 4.5–4.7% annually, making it a meaningful income contributor in today’s elevated interest rate environment. Bonds serve as the portfolio’s shock absorber. When equity markets fall sharply, bonds typically hold their value or even appreciate — providing both psychological stability and a source of dry powder for opportunistic rebalancing.

Recommended allocation: 10–20% of your total portfolio. Younger investors in the accumulation phase (under 45) can keep this at 10% or even lower. Investors within 10–15 years of retirement may want to gradually increase bond exposure toward 20–30% as they approach their income-distribution phase. See our guide on how often to rebalance your portfolio for a framework on adjusting allocations over time.

Building Your 3 ETF Portfolio: Allocation Frameworks

Your allocation across these three ETFs should reflect your age, risk tolerance, and time horizon. Here are three practical starting frameworks:

| Investor Profile | VOO (US Equity) | VXUS (International) | BND (Bonds) | Focus |

|---|---|---|---|---|

| Aggressive (20–35 yrs) | 80% | 10% | 10% | Maximum long-term growth |

| Moderate (35–50 yrs) | 70% | 20% | 10% | Balanced growth + stability |

| Conservative (50+ yrs) | 50% | 20% | 30% | Capital preservation + income |

These allocations are starting points — not rigid rules. Adjust based on your personal financial situation, investment goals, and any other assets you hold outside this portfolio. The important thing is to choose an allocation you can stick with through market volatility. A 100% equity investor who panic-sells during a correction will dramatically underperform a 70/20/10 investor who holds steady.

A Real-World Compounding Simulation

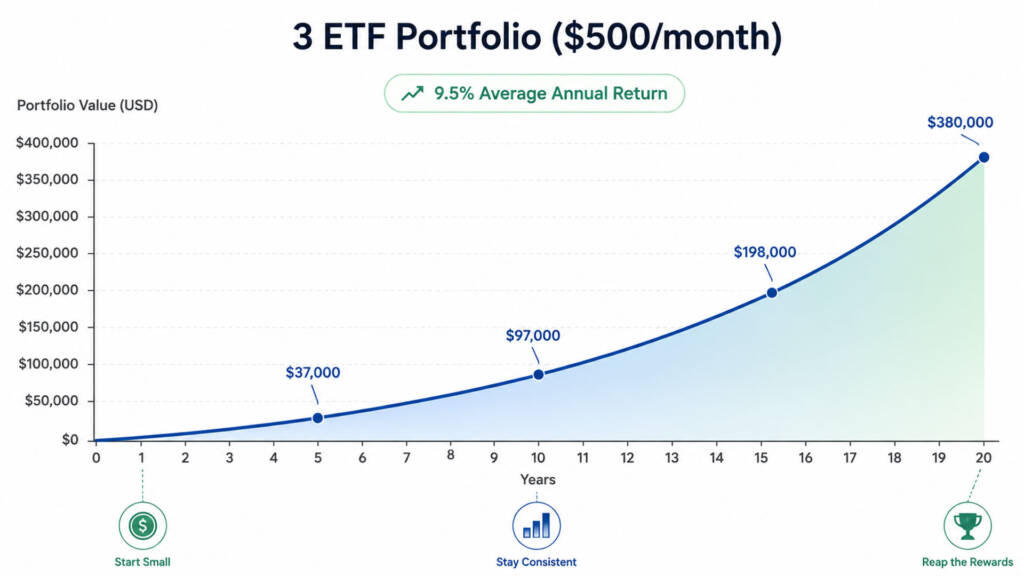

Let’s make this concrete. Here’s a projected growth simulation for the 80/10/10 allocation with a $500/month contribution starting in 2026. We use a blended weighted return of approximately 9.5% — conservative relative to historical performance — to account for the bond drag and international diversification.

These are projected outcomes based on historical averages — not guaranteed returns.

| Year | Total Contributed | Projected Portfolio Value | Projected Gain |

|---|---|---|---|

| Year 5 | $30,000 | ~$37,200 | ~$7,200 |

| Year 10 | $60,000 | ~$97,400 | ~$37,400 |

| Year 15 | $90,000 | ~$198,200 | ~$108,200 |

| Year 20 | $120,000 | ~$380,000 | ~$260,000 |

| Year 30 | $180,000 | ~$1,010,000 | ~$830,000 |

That’s the power of compounding in action. By Year 30, your $180,000 in total contributions has grown to over $1 million — with $830,000 of that being pure investment gain. This is why the 3 ETF portfolio strategy is the backbone of the FIRE (Financial Independence, Retire Early) movement and is recommended by virtually every credible financial planner for passive, long-term wealth building.

To maximize this effect, combine this strategy with consistent dollar-cost averaging — investing the same fixed amount every month regardless of market conditions. This ensures you buy more shares when prices are low and fewer when prices are high, naturally lowering your average cost basis over time.

How to Rebalance Your 3 ETF Portfolio

Over time, market movements will cause your allocation to drift from its target. For example, if US equities outperform strongly — as they did in 2023 and 2024 — your VOO allocation might grow from 80% to 88%, taking on more risk than intended. Annual rebalancing brings it back on track.

Here is a simple rebalancing framework for 3 ETF portfolio investors:

- Step 1: Review your portfolio once a year — same date annually

- Step 2: Check if any ETF has drifted more than ±5% from its target weight

- Step 3: Direct new contributions toward underweight positions first — before selling anything

- Step 4: If new contributions aren’t enough, sell a small portion of overweight holdings inside a tax-advantaged account (IRA/401k) to avoid triggering capital gains

- Step 5: Reassess your overall allocation as you age — gradually increasing BND exposure as you approach retirement

This process takes under 30 minutes per year. For a deeper framework, our complete guide on how often to rebalance your portfolio covers every approach in detail.

3 ETF Portfolio Variations Worth Considering

Once you’re comfortable with the base structure, you can customize it further based on your personal goals. Here are three proven variations:

Variation 1: Growth-Tilted (Replace BND with QQQ)

Replace your 10% bond allocation with QQQ (Invesco Nasdaq-100 ETF) for a pure growth tilt — ideal for younger investors with a 20+ year horizon who want additional tech exposure. Just understand that this removes your portfolio stabilizer entirely, increasing volatility significantly. Our QQQ vs. VOO comparison explores this tradeoff.

Variation 2: Income-Tilted (Replace BND with SCHD)

Replace your 10% bond allocation with SCHD (Schwab U.S. Dividend Equity ETF) for a portfolio that generates meaningful dividend income alongside equity growth. This creates a powerful hybrid — growth from VOO and VXUS, income from SCHD’s ~3.25% yield. This structure aligns beautifully with a dividend snowball strategy, where reinvested dividends compound aggressively over time.

Variation 3: Balanced Growth + Income (VOO + SCHD + BND)

This is our recommended variation for intermediate investors who want both growth and current income:

- 60% VOO — core US equity growth

- 30% SCHD — dividend income and quality US equities

- 10% BND — portfolio stability and interest income

This combination gives you strong capital appreciation from VOO, reliable growing dividends from SCHD, and bond-based stability from BND — a genuinely comprehensive, self-reinforcing portfolio. For more ideas on pairing income ETFs with your growth core, our VOO and JEPQ portfolio guide explores another powerful pairing.

For authoritative external context on building a diversified ETF portfolio, see Vanguard’s official investor education center for research-backed guidance on asset allocation principles.

Conclusion & Call to Action

The 3 ETF portfolio strategy is the most powerful wealth-building system available to individual investors in 2026 — not because it’s complex, but precisely because it’s not. Three funds. Broad global diversification. Ultra-low fees. Annual rebalancing. And the discipline to let compounding do its work over decades. With VOO as your core, VXUS as your global layer, and BND as your stabilizer, you hold a portfolio that rivals the diversification of billion-dollar institutional endowments — at a fraction of the cost.

The best time to build this portfolio was 10 years ago. The second-best time is today. Start with whatever you have — even investing $50 a month in VOO shows how small, consistent contributions build real wealth over time.

Which variation of the 3 ETF portfolio are you building — or thinking about building? Drop your current allocation in the comments below. And if you want to understand how dividend ETFs fit into this structure, don’t miss our deep-dive on SCHD vs. DGRO 2026 to choose the best income satellite for your three-fund core.

Frequently Asked Questions

Q1: What is the best 3 ETF portfolio combination for US investors in 2026?

A1: For US investors in 2026, the strongest 3 ETF combination is VOO (80%) + VXUS (10%) + BND (10%). VOO provides core S&P 500 exposure with a 0.03% expense ratio and Morningstar’s Gold rating. VXUS adds international diversification across 8,500+ global stocks at 0.07% expense ratio. BND delivers bond market stability and approximately 4.5–4.7% yield. Together, this portfolio covers virtually every major investable asset class on earth at a blended expense ratio of approximately 0.03–0.05% — making it one of the most efficient portfolios available to any individual investor.

Q2: Is a 3 ETF portfolio good for beginner investors?

A2: Yes — the 3 ETF portfolio strategy is arguably the single best starting framework for beginner investors. It requires no stock selection skills, no market timing, and no complex analysis. Beginners simply choose their target allocation (e.g., 80/10/10 or 70/20/10), invest a fixed amount monthly through dollar-cost averaging, and rebalance annually. The strategy eliminates most behavioral mistakes — panic-selling, chasing trends, over-trading — that typically destroy beginner investor returns. It’s the same core strategy recommended by Vanguard, Morningstar, and the Boglehead investment community.

Q3: How often should I rebalance my 3 ETF portfolio?

A3: For most long-term investors, annual rebalancing is the optimal frequency — supported by research from Vanguard and Fidelity. You review your allocation once a year and rebalance only if any position has drifted more than 5 percentage points from its target weight. The most tax-efficient approach is to direct new monthly contributions toward underweight positions first, before selling any holdings. This method avoids triggering capital gains taxes in taxable accounts while keeping your allocation disciplined. For tax-advantaged accounts (IRA, 401k), you can rebalance freely without any tax consequences.

Financial Disclaimer: This article is intended for educational and informational purposes only. It does not constitute financial, investment, tax, or legal advice. All projected portfolio values and compounding simulations are based on historical average returns and do not guarantee future results. Individual outcomes will vary based on contribution amounts, market conditions, timing, and personal tax situations. Always consult a licensed financial advisor before making any investment decisions.