Most people save their entire lives, only to retire and find out their savings won’t last. They trusted a low-interest savings account — and inflation quietly ate their purchasing power year after year. In 2026, with the US headline CPI sitting at 3.8% as of April and core inflation at 2.8%, letting your money sit idle is a slow financial loss. The solution? Learning how to build a dividend portfolio in 2026 — a proven strategy to generate consistent, growing passive income while your capital appreciates over time.

Key Takeaways:

- A dividend portfolio built on quality ETFs like SCHD and VOO can generate reliable passive income while outpacing inflation over the long term.

- Reinvesting dividends through a DRIP strategy activates the compounding snowball effect — turning modest starting capital into meaningful income.

- You don’t need $100,000 to start. Consistent monthly contributions, even as small as $50–$200, can build a life-changing income stream over 10–20 years.

Why Dividend Investing Makes Sense in 2026

The investment landscape in 2026 rewards income-focused investors more than ever before. With US inflation elevated and equity market volatility persisting — VOO (Vanguard S&P 500 ETF) posted a year-to-date total return of approximately +11.25% through late May 2026 with dividends reinvested — the case for dividend-paying assets alongside broad-market exposure is compelling. Dividend stocks and ETFs give you two powerful tailwinds: price appreciation AND regular cash income.

Moreover, high-quality dividend payers tend to be financially resilient companies. They generate real, consistent cash flows. That’s why they can sustain and grow their payouts even through recessions.

The Problem With Only Chasing Growth

Pure growth investing is exciting during bull markets. However, when markets correct, growth-only portfolios can lose 30–50% of their value with no income to cushion the blow. A dividend portfolio, by contrast, continues paying you while you wait for recovery. This psychological and financial buffer makes dividend investing particularly suited to long-term, wealth-building investors.

Step 1 — Define Your Dividend Investing Goal

Before you buy a single share, you must answer one critical question: What do you need your portfolio to do?

There are three types of dividend investors:

- Income-focused investors — Prioritize high current yield (4–6%+) to generate immediate cash flow. Best for those nearing or in retirement.

- Growth-focused investors — Prioritize dividend growth over current yield. They accept a lower starting yield (2–3%) in exchange for faster payout growth over time. Best for investors with a 10–20 year horizon.

- Balanced investors — Blend both approaches. They want steady income now AND meaningful growth. This is the most popular strategy for beginners in their 30s–50s.

Knowing your goal shapes every other decision — from which ETFs you choose to how you rebalance over time. If you’re still deciding between growth and income, our deep-dive on growth vs. dividend investing can help you choose the right path.

Step 2 — Understand the Core Building Blocks

A dividend portfolio in 2026 can be built from three asset types. Each serves a specific role.

Dividend ETFs (Best for Beginners)

Exchange-traded funds are the most beginner-friendly way to build a dividend portfolio in 2026. A single ETF instantly gives you exposure to dozens or hundreds of dividend-paying companies. You reduce single-stock risk dramatically. If you’re new to ETFs altogether, start with our beginner’s guide to ETF investing before going further.

The three most popular dividend ETF categories in 2026 are:

Dividend Growth Stocks (For Intermediate Investors)

Once you’re comfortable with ETFs, you can add individual dividend stocks. Strong foundational names in 2026 include companies like Microsoft (MSFT), Johnson & Johnson (JNJ), JPMorgan Chase (JPM), and PepsiCo (PEP) — blue-chip companies with long histories of growing their payouts. For beginners, keep individual stocks at no more than 20–30% of your portfolio.

REITs and Income ETFs (For Yield Enhancement)

Real Estate Investment Trusts (REITs) like Realty Income (O) are legally required to distribute 90% of taxable income as dividends. They can boost your overall portfolio yield meaningfully. Use them as a satellite position — not your core holding.

Step 3 — Build Your Portfolio Structure

The most battle-tested framework for dividend investors is the Core and Satellite approach. Your core holding provides stability and broad market exposure. Your satellite holdings add targeted income and yield enhancement. You can explore this strategy in depth in our core and satellite portfolio guide.

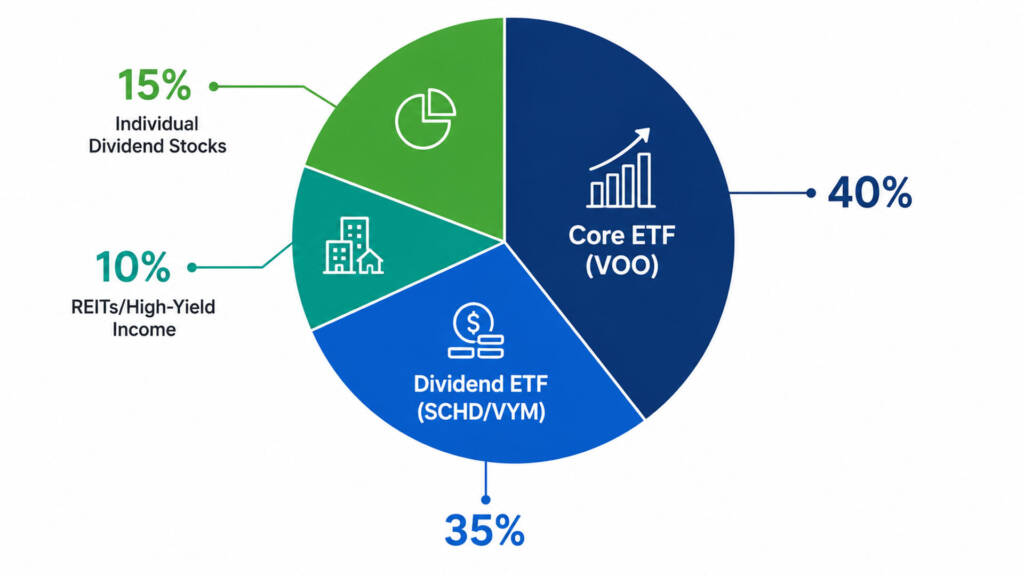

A Simple Starter Allocation for 2026

Here is a practical, beginner-friendly dividend portfolio structure:

- 40% — VOO (Vanguard S&P 500 ETF): Your bedrock. VOO tracks the S&P 500 and has delivered a 10-year+ annualized total return consistently above 10%, with +11.25% YTD through late May 2026 (dividends reinvested). It stabilizes the portfolio and ensures you capture broad US market growth.

- 35% — SCHD (Schwab US Dividend Equity ETF): Your dividend engine. SCHD currently yields approximately 3.2–3.4% and delivered a 1-year total return of 28.2% with a 10-year annualized return of 12.7%. Its Q1 2026 dividend of $0.2569 per share represents a 3.3% year-over-year increase — the largest Q1 payout in the ETF’s history.

- 15% — VYM (Vanguard High Dividend Yield ETF): Your income booster. VYM diversifies your dividend sources across hundreds of large-cap dividend payers. For a detailed SCHD vs. VYM comparison, see our SCHD vs. VYM breakdown.

- 10% — REITs or High-Yield Income (e.g., Realty Income, JEPQ): Your yield kicker. This slice adds higher current income. For a detailed look at combining a growth core with income enhancement, see our VOO and JEPQ portfolio article.

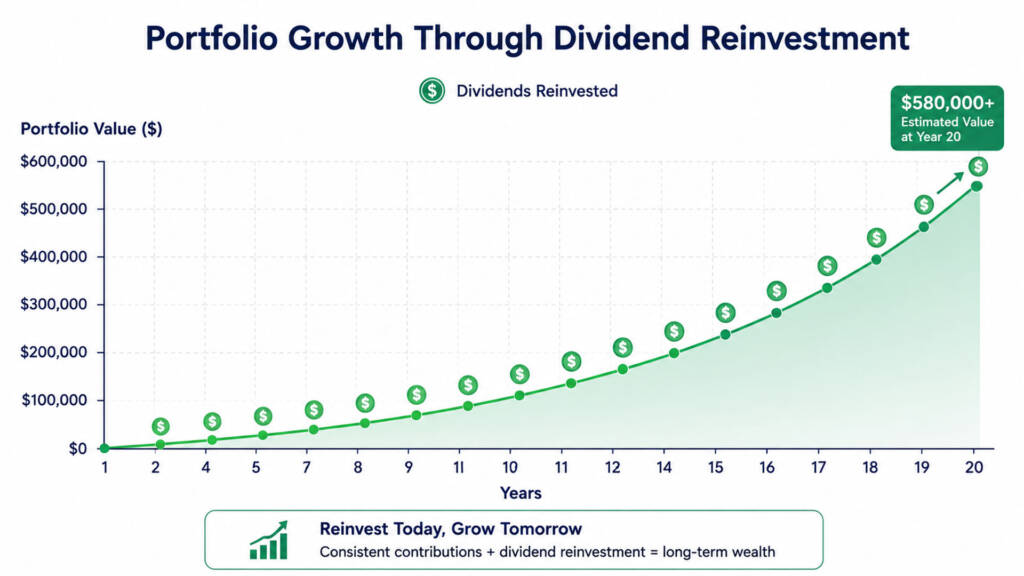

Step 4 — Run the Compounding Numbers

Numbers make strategies real. Let’s look at a realistic simulation based on today’s data.

Scenario: $5,000 Starting Capital + $300/Month

Assume you invest $5,000 today and add $300 each month. Your blended portfolio yield is approximately 3.0%. You reinvest all dividends (DRIP). You assume a modest blended annual total return of 9% per year (consistent with the long-term historical average of a diversified dividend ETF portfolio).

| Year | Portfolio Value (Approx.) | Annual Dividend Income |

|---|---|---|

| Year 1 | ~$9,100 | ~$273 |

| Year 3 | ~$18,400 | ~$552 |

| Year 5 | ~$28,900 | ~$867 |

| Year 10 | ~$62,500 | ~$1,875 |

| Year 20 | ~$212,000 | ~$6,360 |

Note: This is a projected illustration using historical return assumptions. It does not guarantee future results.

The power of this simulation is the dividend snowball effect — each reinvested dividend buys more shares, which generate more dividends, which buy even more shares. After Year 10, the growth curve steepens dramatically. For a deeper explanation of this concept, read our article on the dividend snowball effect.

Even if you can only invest $50 per month right now, starting is more important than the amount. Our guide on investing $50 a month in VOO shows you exactly why starting small still beats waiting.

Step 5 — Choose the Right Account and Broker

Your account type dramatically affects how much of your dividend income you actually keep.

- Roth IRA (US investors): Dividends and capital gains grow tax-free. This is the single most powerful account for long-term dividend investors. Contribute up to $7,000/year in 2026 (under age 50).

- Traditional IRA or 401(k): Contributions are pre-tax, but dividends are taxed upon withdrawal. Still highly beneficial for high earners.

- Taxable Brokerage Account: Suitable for contributions exceeding IRA limits. Qualified dividends are taxed at the lower capital gains rate (0%, 15%, or 20% depending on your income bracket).

For international investors accessing US dividend ETFs, platforms like Interactive Brokers provide access to US-listed ETFs with transparent fee structures. Be aware of the 30% US withholding tax on dividends for non-US residents — though this can often be reduced via tax treaties depending on your country of residence.

Step 6 — Automate With Dollar-Cost Averaging

The most reliable path to building wealth is removing emotion from the equation. Set a fixed monthly investment amount and automate it. You invest the same dollar amount every month — whether the market is up, down, or sideways. This strategy is called Dollar-Cost Averaging (DCA), and it is the single most effective habit you can build as a dividend investor. Our complete guide to dollar-cost averaging explained walks you through the exact mechanics.

DCA ensures you buy more shares when prices fall and fewer when prices rise. Over time, this lowers your average cost per share. It also eliminates the anxiety of trying to time the market — a game that even professional fund managers consistently lose.

Step 7 — Monitor, Rebalance, and Stay the Course

Building the portfolio is only half the job. You also need a simple maintenance plan.

When Should You Rebalance?

Most dividend investors rebalance once or twice per year. You check whether your allocation has drifted more than 5–10% from your target. If VOO has surged and now represents 55% of your portfolio instead of 40%, you trim it back and add to SCHD or VYM. Our guide on how often to rebalance your portfolio covers the exact criteria and process.

What to Do in a Market Crash

Market crashes feel terrifying. However, for dividend investors, they are actually buying opportunities. When prices fall, dividend yields rise (because yield = annual dividend ÷ price). This means you buy more shares at a higher effective yield. Read our guide on what to do when the stock market crashes so you’re mentally and strategically prepared before volatility hits.

Common Mistakes to Avoid When Building a Dividend Portfolio

Even motivated investors sabotage their results with a few predictable errors. Avoid these pitfalls:

- Chasing the highest yield: A 10% yield often signals a struggling company that may cut its dividend. Focus on sustainable yield (typically 2–5%) backed by healthy payout ratios (below 75%).

- Ignoring diversification: Concentrating in one sector (e.g., all energy or all REITs) exposes you to sector-specific risk. Spread holdings across 5–7 different industries.

- Starting with too many holdings: Beginners often own 40+ stocks and lose track of everything. Start with 2–3 ETFs. Add individual stocks only after you understand the fundamentals.

- Stopping contributions during downturns: This is the #1 wealth-destroying mistake. Market dips are discount sales on quality assets. Keep buying. See our full list of beginner investor mistakes to avoid.

- Ignoring fees: An expense ratio difference of 0.5% per year compounding over 20 years can cost you tens of thousands of dollars. Stick to low-cost ETFs.

Conclusion & Call to Action

Building a dividend portfolio in 2026 is not complicated — but it does require intention, consistency, and patience. Start with a clear goal. Choose a simple structure anchored by broad-market ETFs like VOO and quality dividend ETFs like SCHD. Automate your contributions. Reinvest your dividends. And stay the course when the market gets noisy. With US inflation at 3.8% as of April 2026, the real cost of not investing has never been higher.

The best time to start was yesterday. The second-best time is today.

Have you started building your dividend portfolio yet? Share your current strategy or questions in the comments below! And if you’re still comparing your ETF options, don’t miss our SCHD vs. DGRO 2026 comparison and our 3 ETF portfolio strategy guide for your next read.

FAQs

Q1: How much money do I need to start building a dividend portfolio in 2026?

A1: You can start building a dividend portfolio with as little as $50–$100. Many brokers like Fidelity and Charles Schwab now offer fractional shares, so you can buy a partial share of SCHD or VOO with any dollar amount. What matters most is not how much you start with, but that you start consistently and add to your portfolio every month through dollar-cost averaging.

Q2: What is the best dividend ETF to build a portfolio around in 2026?

A2: SCHD (Schwab U.S. Dividend Equity ETF) is widely considered the top choice for dividend portfolio building in 2026. It currently yields approximately 3.2–3.4%, has a rock-bottom expense ratio of 0.06%, and has delivered a 10-year annualized total return of 12.7%. Most experts recommend pairing SCHD with a broad-market core holding like VOO for balance between income and growth. You can compare SCHD against other top dividend ETFs in our SCHD vs. DGRO 2026 article.

Q3: Should I reinvest dividends or take them as cash in 2026?

A3: If you are in the wealth-building phase of your life (generally under 55–60 years old), reinvesting dividends through a DRIP (Dividend Reinvestment Plan) is almost always the superior choice. Reinvesting allows your dividends to buy more shares automatically, which then generate more dividends — compounding your income exponentially over time. Only consider taking dividends as cash once you need the income to cover living expenses.

Financial Disclaimer: This article is intended for educational and informational purposes only. The content does not constitute financial, investment, tax, or legal advice. All investment examples and projections shown are hypothetical and based on historical data — they do not guarantee future performance. Investing in the stock market involves risk, including the possible loss of principal. Always conduct your own due diligence and consult a licensed financial advisor before making any investment decisions. External reference: Investopedia – Dividend Investing