Most people know they should be investing — but life gets in the way. You miss a contribution here, forget to buy there, and suddenly months go by without putting a single dollar to work. Meanwhile, the market keeps moving. That hesitation and inconsistency is silently costing you years of compounding growth. The good news? You can completely eliminate the guesswork with a proven automate investments ETF strategy that works around the clock — even while you sleep.

Key Takeaways:

- Automating your ETF investments removes emotion and timing from the equation, which are the two biggest threats to long-term wealth building.

- Dollar-cost averaging (DCA) into broad-market ETFs like VOO has historically generated ~10% annualized returns over the long run.

- A “Set It and Forget It” strategy requires just four steps: choose your ETF, set a recurring amount, enable DRIP, and rebalance annually.

Why Automating Your Investments Changes Everything

Most investors fail not because they pick the wrong stocks — but because they behave badly. They panic sell during crashes. They wait for the “perfect” entry point that never comes. Automation removes you from your own worst enemy: yourself.

When you automate investments using an ETF strategy, you commit to buying on a fixed schedule regardless of market conditions. This behavior is backed by decades of evidence. The S&P 500 has historically delivered approximately 10% annualized returns over the long run, including dividends, and has risen in roughly 70% of all calendar years. That consistent upward trend rewards the patient, systematic investor more than any market timer.

In 2026, VOO — the Vanguard S&P 500 ETF — reached a milestone by becoming the first ETF to surpass $1 trillion in assets under management, driven by $69 billion in investor inflows. That level of institutional and retail confidence reflects exactly why this ETF is the cornerstone of automated investing strategies worldwide.

The Psychology Behind Automation

When you automate, you stop treating investing as an event and start treating it as a habit. Habits require zero willpower after they’re established. This is the same principle behind direct deposit into a savings account — you spend what you don’t see. Automated investing works the same way, except the money compounds at a historically superior rate compared to cash sitting idle.

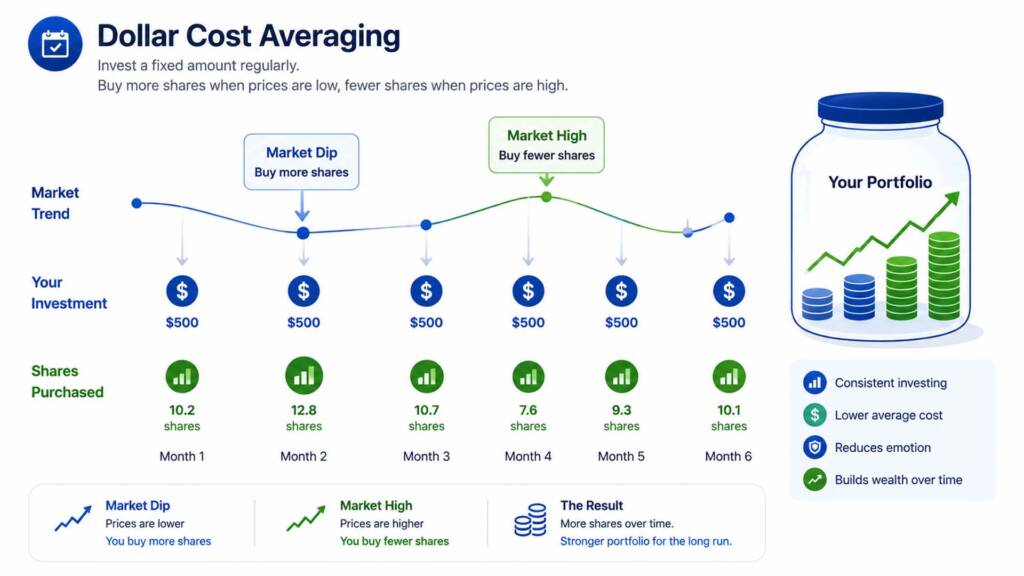

What Is Dollar-Cost Averaging and Why Does It Work?

Dollar-cost averaging (DCA) is the practice of investing a fixed dollar amount into a chosen ETF at regular intervals — weekly, bi-weekly, or monthly — regardless of the current market price.

Here’s the mechanical magic of DCA:

- When prices are high, your fixed amount buys fewer shares.

- When prices are low, your fixed amount buys more shares.

- Over time, your average cost per share decreases, even in volatile markets.

This is not just theory. When you consistently invest into a broad-market ETF like VOO through both the S&P 500’s brief -4.33% dip in early 2026 and its subsequent recovery to ~8–9% gains, you automatically buy more units at depressed prices — dramatically improving your long-run average cost basis.

You can learn more about this concept in depth in our guide on Dollar-Cost Averaging Explained.

DCA vs. Lump Sum Investing

| Factor | DCA (Automated) | Lump Sum |

|---|---|---|

| Emotional stress | Low — fully automated | High — requires timing confidence |

| Risk of buying at peak | Spread across time | High if timed poorly |

| Best for | Regular salary investors | Windfalls or large cash positions |

| Consistency | Guaranteed by automation | Relies on discipline |

| Long-term outcome | Competitive, lower volatility | Slightly higher in rising markets |

For most working investors with a regular paycheck, DCA is the statistically safer and psychologically superior choice. A study highlighted by Investopedia confirms that DCA outperforms lump-sum investing in roughly one-third of market environments — and produces near-equivalent results in many others, with far less stress.

Choosing the Right ETFs for Your Automated Portfolio

Not all ETFs are created equal for automation. For a true “Set It and Forget It” portfolio, you want ETFs that are:

- Broadly diversified — no single company concentration risk

- Low-cost — expense ratio under 0.10%

- Highly liquid — easy to buy fractional shares automatically

- Backed by a proven index — not a niche or thematic sector fund

Here are the three core ETF types for an automated strategy:

Core Growth ETF: VOO (Vanguard S&P 500 ETF)

VOO tracks the S&P 500, holding 500 of the largest US companies. As of June 15, 2026, VOO trades at approximately $682.79 per share. Its expense ratio is just 0.03% — meaning on a $10,000 portfolio, you pay just $3 per year in fees. This is your portfolio’s engine. Learn more in our detailed VOO ETF Core Portfolio guide, or see how it stacks up in our VOO vs. SPY 2026 comparison.

Diversifier ETF: VTI (Vanguard Total Stock Market ETF)

VTI extends beyond the S&P 500 to include over 3,500 US stocks — adding mid-cap and small-cap exposure. It pairs perfectly with VOO in a core-and-satellite structure. Read our full breakdown in the VTI vs VOO analysis.

Income ETF: SCHD (Schwab US Dividend Equity ETF)

Adding a dividend-focused ETF like SCHD introduces a cash flow layer to your automated portfolio. Reinvesting those dividends via DRIP automatically buys more shares — compounding your income. Explore this in our SCHD ETF Review 2026 and our piece on Dividend Growth Investing for Beginners.

Building Your Set It and Forget It Portfolio: Step-by-Step

Here is the exact four-step process to automate your investment strategy today:

Step 1: Open a Brokerage Account That Supports Automation

You need a platform that supports recurring/automatic investments and fractional shares. Top options include:

- Fidelity — Free DCA, fractional shares, zero commissions

- Charles Schwab — Automated investing, fractional shares via Schwab Stock Slices

- Interactive Brokers (IBKR) — Excellent for international investors; supports automatic recurring orders. Start here with IBKR

IBKR is particularly well-suited for investors outside the US who want access to US-listed ETFs like VOO and VTI at competitive rates.

Step 2: Choose Your ETF Allocation

A simple, beginner-proof automated portfolio could look like this:

| ETF | Allocation | Purpose |

|---|---|---|

| VOO | 70% | Core US large-cap growth |

| VTI or VXUS | 20% | Broad market / international |

| SCHD | 10% | Dividend income layer |

This is aligned with the 3-ETF portfolio approach outlined in our 3 ETF Portfolio Strategy guide. For a deeper dividend-focused build, see our Build a Dividend Portfolio 2026 article.

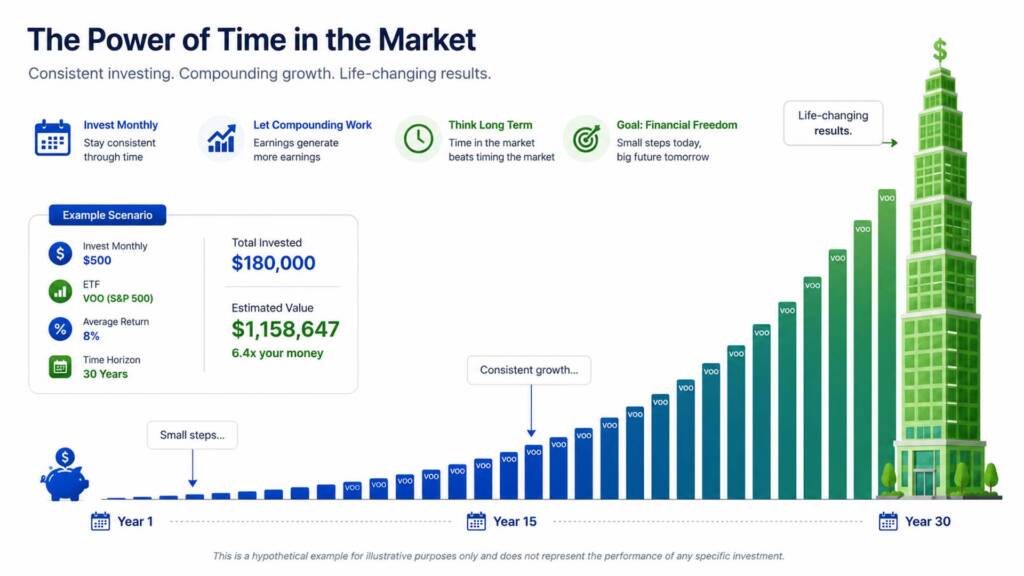

Step 3: Set a Recurring Investment Amount

Choose a fixed dollar amount you can contribute every month without fail. It doesn’t have to be large. Here’s what a consistent $200/month automated into VOO could look like, based on the S&P 500’s historical ~10% annualized return:

| Years Invested | Total Contributed | Projected Portfolio Value* |

|---|---|---|

| 5 years | $12,000 | ~$15,300 |

| 10 years | $24,000 | ~$38,200 |

| 20 years | $48,000 | ~$152,000 |

| 30 years | $72,000 | ~$452,000 |

*Projected using historical ~10% annualized return. Past performance does not guarantee future results.

Even $50 per month makes a meaningful difference over time. See the full breakdown in our article Investing $50 a Month in VOO. You can also use our FIRE Calculator to model your own personalized projection.

Step 4: Enable DRIP (Dividend Reinvestment Plan)

DRIP automatically reinvests any dividends your ETF pays back into additional shares. This is one of the most powerful wealth-building mechanics available to passive investors. Over decades, reinvested dividends can account for over 40% of total portfolio returns according to data from Vanguard. This is the concept behind the Dividend Snowball Effect — small reinvestments that compound into massive results over time.

When and How to Rebalance Your Automated Portfolio

“Set It and Forget It” does not mean “never look at it again.” Over time, market performance shifts your allocation. For example, after a strong year for VOO, your growth slice may grow from 70% to 80% of your portfolio — increasing your concentration risk beyond your original intent.

A smart rule of thumb is to rebalance once a year — or whenever any allocation drifts more than 5% from your target. This annual check-in is all the active management your automated portfolio should require. Our full guide on How Often to Rebalance Your Portfolio covers this in detail. You can also explore our Core and Satellite Portfolio framework for a structured approach to keeping your holdings balanced.

What to Do During Market Crashes

One of the hardest psychological tests of an automated strategy is a market crash. When your portfolio is down 20%, every instinct says to sell. Don’t. Your automation is buying more shares at lower prices during that exact window — which is mathematically the best possible thing that can happen to a long-term DCA investor.

The S&P 500 experienced a brief correction in early 2026, dipping approximately -4.33% before recovering to post year-to-date gains. Investors who stayed the course and kept their automation running captured every unit of that recovery. Our guide on What to Do When the Stock Market Crashes provides a practical playbook for exactly these moments.

Advanced Automation: Adding Income Layers

Once your core automated strategy is in place, you can add sophistication without adding complexity. Consider layering in income-generating ETFs that also support automatic reinvestment:

- JEPI or JEPQ — Covered call ETFs that generate monthly income. Read our JEPI vs JEPQ breakdown or the dedicated JEPQ ETF Review 2026.

- SCHD vs DGRO — For dividend growth income automation. See our SCHD vs DGRO 2026 comparison.

- Bond ETFs — Add stability by automating a small bond allocation. Our Bond ETF Guide for Beginners 2026 covers the basics.

These additions create a Passive Income ETF Portfolio — a multi-stream automated machine that grows capital, generates income, and reinvests all simultaneously. Explore the full blueprint in our Passive Income ETF Portfolio guide.

Conclusion & Call to Action

Automating your investments with an ETF strategy is the single most powerful financial habit you can build. By combining a low-cost index ETF like VOO as your core, pairing it with DCA on a fixed monthly schedule, enabling DRIP, and checking in annually to rebalance, you create a system that compounds wealth with almost zero ongoing effort.

The data backs this up: the S&P 500 has returned approximately 10% annualized historically, VOO became the world’s largest ETF in 2026, and investors who stayed automated through early 2026’s volatility captured the full recovery.

Your next step is simple: open a brokerage account, pick your ETFs, set a recurring amount, and hit go. The best day to start was yesterday — the second best is today.

👉 Have you already set up automated investing? Drop a comment below and tell us your ETF picks! Or, if you’re just getting started, read our Beginner Investor Mistakes guide before you make your first move.

FAQs

Q1: What is the best ETF to automate investments for a beginner in 2026?

A1: For most beginners, VOO (Vanguard S&P 500 ETF) is the best single ETF to start automating. It tracks the 500 largest US companies, carries an ultra-low 0.03% expense ratio, and as of June 2026 trades at approximately $682 per share with fractional share support available on most platforms. Its long-term track record of ~10% annualized historical returns makes it the benchmark for passive ETF investing. Pair it with automatic dividend reinvestment (DRIP) from day one.

Q2: How much money do I need to start an automated ETF investment strategy?

A2: You can start automating investments with as little as $1 using platforms that support fractional shares. Practically speaking, even $50 to $100 per month invested consistently into a broad-market ETF like VOO builds meaningful wealth over 10–30 years thanks to compounding. The key is not the starting amount — it’s the consistency and automation of the contribution schedule.

Q3: Does automating investments mean I never have to actively manage my portfolio?

A3: Automation handles the buying — but you should still review your portfolio allocation once a year. Over time, strong performance in one ETF can shift your portfolio away from your target allocation, increasing unintended risk. A simple annual rebalance (selling a small amount of your over-weight position and buying the under-weight one) keeps your strategy on track without requiring constant attention.

Financial Disclaimer: This article is intended for educational and informational purposes only. It does not constitute financial, investment, or tax advice. The examples, projections, and historical data cited are for illustrative purposes and do not guarantee future results. All investing involves risk, including the possible loss of principal. Always conduct your own research and consult with a licensed financial advisor before making any investment decisions.